A quick peek into the report

Market Overview

Market Overview and Estimation

The advanced power solutions an emerging technology market that is high in demand for implantable and wearable medical devices, as they offer better safety and reliability. These advanced solutions technology also offers longer battery life, thus ensuring that batteries need not to be changed too frequently. Considering, it is difficult to change batteries in implantable medical devices.

Currently, the advanced power solutions technology growth is due to the their usage in most medical devices. The emergence of sedentary lifestyles, changing dietary habits, irregular sleep patterns, and professional requirements that involve prolonged working hours, poor body postures, and high levels of anxiety and stress are the leading causes of various disorders such as cardiovascular, neurological and hearing disorders. An increase in the number of such disorders is propelling the market growth of advanced power solutions.

Also, the high prevalence of road accidents leading to an increased prevalence of spinal cord injuries results in higher socioeconomic burden of cardiovascular and neurological disorders is another cause of increasing market demand for advance power solutions.

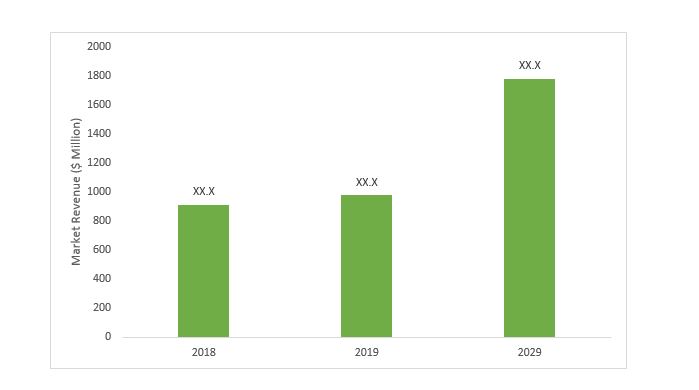

Global Advanced Power Solutions for Implantable and Wearable Medical Devices Market Report by BIS Research highlights that the market value is projected to grow at a significant CAGR of 6.26% during the forecast period, 2019-2029. The global advanced power solutions for implantable and wearable medical devices generated a market revenue of $912.73 million in 2018, in terms of value.

The continued significant investments by the healthcare and battery companies to meet the industry demand is one of the prominent factors boosting the market growth of the global advanced power solutions for implantable and wearable medical devices.

Further, the growing demand for smart wearables and increasing awareness among patients regarding implantable medical devices is also bolstering the growth of the global advanced power solutions for implantable and wearable medical devices market.

|

Growth Drivers

|

• Growing Geriatric Population Leads to Surge in Exigency of Implantable and Wearable Devices • Increasing Burden of Disease Inciting the Use of Implantable and Wearable devices |

||

|

Market Challenges

|

• Depleting Lithium Resources • Complexities in the Manufacturing Process |

||

|

Market Opportunities

|

• High Growth Opportunity in the Emerging Economies • Introduction of Nanotechnology in Lithium-ion Batteries |

||

Growth Factors

- Growing Geriatric Population Leads to Surge in Exigency of Implantable and Wearable Devices: Increased life expectancy is one of the major factors behind the high market demand for advanced power solutions. Geriatric population is growing rapidly with an upsurge in demand for primary and long-term care. Also, old age is the greatest risk factor for developing chronic diseases thus, causing a surge in demand for advanced power solutions for medical and wearable devices.

- Increasing Burden of Disease Inciting the Use of Implantable and Wearable devices: The burden of diseases is increasing leading to a surge in morbidity and mortality globally. Some of the leading causes of disability include low back pain, headache disorders (mainly migraine), depressive disorders, diabetes, age-related hearing loss, chronic obstructive pulmonary disease. However, these can be treated with the use of various implantable and wearable medical devices.

- Upsurge in Awareness Levels: The growing awareness related to diseases plays a pivotal role in their prevention and management. For instance, most of the cardiovascular diseases (CVD) related risk factors are controllable and amendable. Hence, awareness among people is of utmost importance as it stimulates a change in health behavior and potentially results in earlier medical intervention and facilitates improved patient outcomes.

Report Description

|

|

|||

|

|

2018 |

|

$912.7 million |

|

|

2019-2029 |

|

$ 1.78 billion |

|

|

6.26% |

|

|

|

|

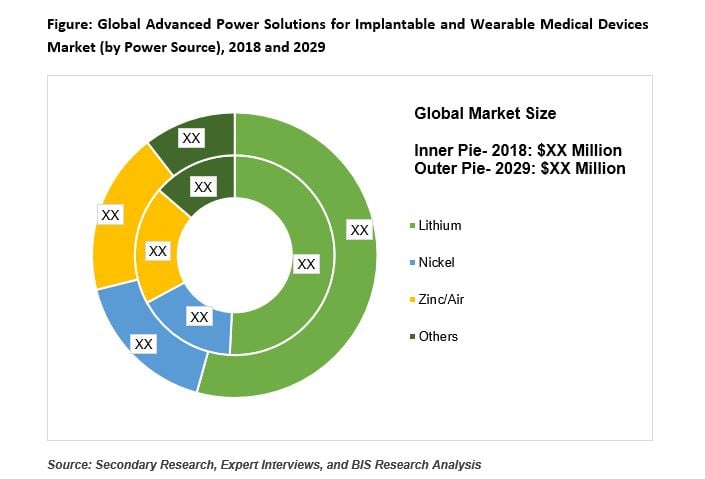

• Power Source - Lithium Batteries, Nickel Batteries, Zinc/Air Batteries, Futuristic Power Solutions, and Others • Applications - Implantable Devices and Wearable Devices • Battery Type - Primary Batteries and Secondary Batteries |

||

|

|

• North America • Europe • Asia-Pacific • Rest-of-the-World |

||

|

|

The key manufacturers include Abbott Laboratories, Boston Scientific Corporation, EaglePicher Technologies, EnerSys, General Electric Company, Ilika Plc, Integer holdings corporation, Medtronic Plc, Murata Manufacturing Co. Ltd., Panasonic Corporation, Saft Batteries, Samsung SDI Co., Ltd., Siemens Healthineers AG, Tianjin Lishen Battery, and Ultralife Corporation, among others. |

||

Market Segmentation

Market Outlook by Power Source

The global advanced power solutions for implantable and wearable medical devices market segmentation based on power source is further categorized into lithium batteries, nickel batteries, zinc/air batteries, and others. The market share of lithium batteries to power implantable and wearable medical devices is the leading contributor to the global advanced power solutions for implantable and wearable medical devices market revenue. Due to the high energy density and low energy discharge on storage for lithium-based batteries they are favoured more over other type of batteries.

By Application

The global advanced power solutions for implantable and wearable medical devices market segmentation based on application is further categorized into implantable and wearable devices. The implantable devices are further sub-segmented into pacemakers, ICDs, spinal cord stimulation devices, deep brain stimulation devices, vagus nerve stimulation devices, cochlear implants, and others. The wearable devices are further sub-segmented into smart wearables and hearing aids. In terms of market size wearable devices contributed the maximum share to the revenue of the segment in 2018.

By Battery Type

The global advanced power solutions for implantable and wearable medical devices market size segmentation based on battery type is further classified into primary batteries and secondary batteries. In terms of market size primary batteries contributed the maximum share to the revenue of the segment in 2018.

By Region

North America, Europe, Asia-Pacific and Rest-of-the-World are the four regional segments of the advanced power solutions for implantable and wearable medical devices market. Wherein, North America contributed the maximum market revenue in 2018. It is also expected that in terms of market size North America will maintain its dominant position.

Global Advanced Power Solutions for Implantable and Wearable Medical Devices Market

Focus on Power Source, Application, Battery Type, Regional Analysis, Data – Analysis and Forecast, 2019-2029