Published Year: 2023

Space Carbon Fiber Composite Market - A Global and Regional Analysis: Focus on Application, End User

The space carbon fiber composite market was valued at $393.6 million in 2022 and is projected...

Focus on Platform, Component, Material, Manufacturing Process, Service, and Country - Analysis and Forecast, 2023-2033

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights that are gathered from primary experts.

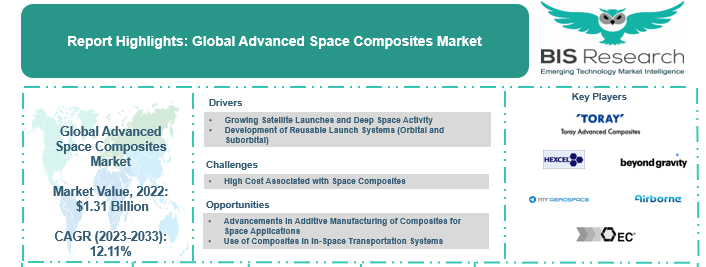

In the global advanced space composites market, established commercial players and legacy companies account for 65% of the market, and small-scale players and startups account for 35% of the market. The primordial established commercial players and legacy companies are Toray Advanced Composites, Beyond Gravity, Hexcel Corporation, Airborne, and MT Aerospace AG, among others. The primordial small-scale players and startups include Orbital Composites, ST Advanced Composites Pvt Ltd., Scorpius Space Launch Company (SSLC), and Infinite Composite Technologies, among others.

Key Companies Profiled:

• Airborne

• Beyond Gravity

• CRP Technology S.r.l

• EURO-COMPOSITES

• Hanwha Cimarron

• Hexcel Corporation

• MT Aerospace AG

• Opterus Research and Development

• Rock West Composites, Inc.

• Teijin Limited

• Toray Advanced Composites

Introduction to Advanced Space Composites

The advanced space composites market is swiftly gaining prominence as a pivotal sector within the aerospace industry, driven by the escalating demand for lightweight and high-strength materials to revolutionize space exploration and satellite technologies. Composites are materials composed of distinct elements combined to achieve superior mechanical, thermal, and structural properties, offering unprecedented opportunities to enhance the efficiency and capabilities of spaceborne systems.

Within this market, various segments stand out, each contributing to the transformation of space technologies through the innovative use of advanced composites. Satellite structures and components represent a critical sector where composites play a pivotal role in constructing lightweight yet robust frameworks that withstand the rigors of launch, vacuum conditions, and thermal extremes. These materials enable the development of larger and more complex satellites, accommodating advanced payloads and expanding communication, Earth observation, and scientific capabilities.

Composite materials find extensive application in the fabrication of rocket structures, contributing to weight reduction, enhanced fuel efficiency, and improved overall performance. This segment encompasses composite fairings, interstage, and even propellant tanks, where high-strength, low-weight materials are essential to facilitate cost-effective and reliable access to space. Advanced propulsion systems constitute a significant segment focusing on harnessing the benefits of composites to create high-performance, lightweight propulsion components. From nozzle assemblies to tanks for liquid propellants, composite materials offer the strength-to-weight ratio necessary for achieving efficient thrust and maneuverability while ensuring the structural integrity required for space missions spanning from Earth's orbit to interplanetary travel.

The realm of space habitat construction and interplanetary exploration also sees the integration of advanced composites to design and fabricate durable systems for extended missions in lunar and interplanetary scope. These materials provide protection against radiation, micrometeoroid impacts, and temperature fluctuations while allowing for modular construction and adaptability to different planetary environments.

The advanced space composites market stands as a driving force behind the transformation of space technologies, offering an array of materials and fabrication techniques that challenge traditional aerospace paradigms. As humanity ventures further into the cosmos, the integration of advanced composites is poised to redefine the limits of what can be achieved in space exploration, satellite deployment, and realization of ambitious interplanetary endeavors.

Market Introduction

Advanced composites offer cost-effectiveness, ease of processability, high strength-to-weight ratio, multifunctionality, and diverse properties in terms of thermal insulation and ablation. High-modulus carbon fiber reinforced laminates are one of the major uses for many composite spacecraft applications. In human crew capsules, composite panels are used to provide the thermal protection system (TPS) required for vehicle re-entry. The temperature capability and low thermal expansion offer additional benefits by reducing the amount of TPS material required, which reduces the weight of the vehicle. Carbon fiber laminates are widely used on satellites and payload support structures. For instance, satellite bus structures are made using aluminum honeycomb sandwich panels with either carbon fiber or aluminum face sheets. Also, high-modulus, high thermal conductivity carbon fiber laminates with low moisture absorption resins, typically cyanate ester, are always used for manufacturing optical benches and other spacecraft structures, which must sustain dimensional stability for accuracy. These advanced composites help in maintaining extreme dimensional stability over extreme temperatures when the spacecraft is in space. Apart from this, radio frequency (RF) reflectors and solar array substrates also use high-modulus carbon fiber laminates in order to achieve stiffness and dimensional stability.

There are several factors that contribute to the growth of the advanced space composites market. Technologies such as reusable launch vehicle systems, on-orbit manufacturing technologies, and upcoming space stations and habitats have the potential to further the use of advanced composites for space applications. The companies operating in the advanced space composites market are highly engaged in research and development initiatives and have been investing in developing new innovative technologies that would enhance space systems. The convergence of visionary space agencies, pioneering private enterprises, and international partnerships underscores the momentum propelling the growth of the advanced space composites market. Advancements in materials science, coupled with enhanced launch vehicle performance and reduced mission costs, have fuelled the market's expansion, with emphasis placed on solving challenges pertaining to structural integration and lifecycle sustainability. The market's trajectory hinges on the resolution of these factors as the space industry increasingly seeks to capitalize on the transformative potential of advanced composites.

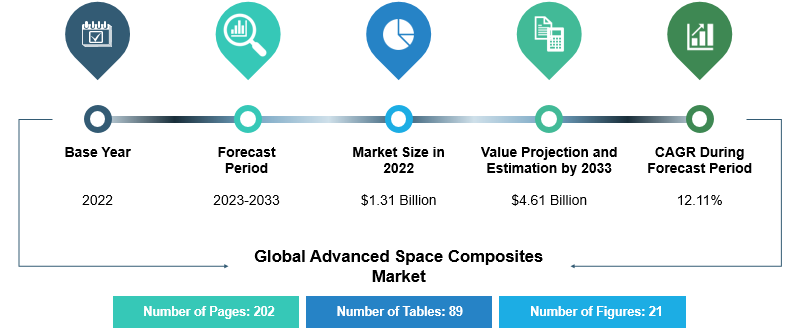

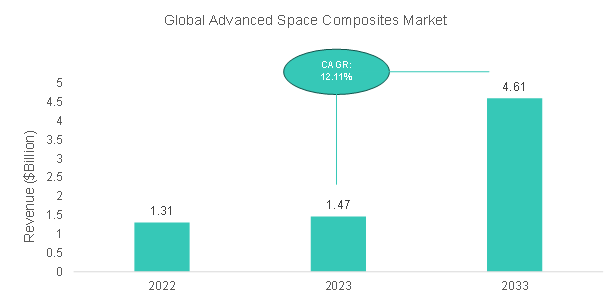

Figure: Global Advanced Space Composites Market Snapshot, $Billion, 2022-2033

Market Segmentation:

Segmentation 1: by Platform

• Satellites

• Launch Vehicles

• Deep Space Probes and Rovers

Launch Vehicles to Dominate as the Leading Platform Segment

The advanced space composites market’s platform segment is led by the launch segment, with a 40.25% share in 2023. The application of advanced composite materials in launch vehicles has brought significant advancements, offering numerous benefits, including weight reduction, increased payload capacity, improved structural integrity, enhanced fuel efficiency, and enhanced performance. Launch vehicle manufacturers are now focusing on designing and developing smaller, less complex, reusable, and cost-efficient launch vehicles, which are facilitated by the growth of small satellites. However, with the rise in satellite launches in the past few years and the expected small satellite mega constellation in the next decade, it is anticipated that the satellites segment will register the highest growth during the forecast period 2023-2033. The satellites segment is expected to grow at the highest CAGR of 12.24% during the forecast period.

Segmentation 2: by Component

• Payloads

• Structures

• Antenna

• Solar Array Panels

• Propellent Tanks

• Spacecraft Module

• Sunshade Door

• Thrusters

• Thermal Protection

Structures Segment to Dominate the Global Advanced Space Composites Market (by Component)

The structures segment is expected to dominate the market during the forecast period from 2023 to 2033. The factor contributing to this growth is the increased focus of space companies to develop reusable launch vehicles as well as small launch vehicles (SLVs).

Segmentation 3: by Material

• Carbon Fiber

• Glass Fiber

• Thermoset

• Thermoplastic

• Nanomaterials

• Ceramic Matrix Composites (CMC) and Metal Matrix Composites (MMC)

• Others

Carbon Fiber Segment to Lead the Global Advanced Space Composites Market (by Material)

The advanced space composites market’s material segment is led by carbon fiber, with a 31.1% share in 2023. Carbon fiber composites have been used by the space industry for several decades and are continuously being used for several space applications, including launch vehicles, satellites, experimental systems, suborbital vehicles, and deep space probes. Recent advancements in carbon fiber manufacturing techniques have enhanced its flexibility, resulting in the introduction of novel carbon fiber types with improved modulus and strength tailored for space system applications.

Segmentation 4: by Manufacturing Process

• Automated Fiber Placement (ATL/AFP)

• Compression Molding

• Additive Manufacturing

• Others

Segmentation 5: by Service

• Repair and Maintenance

• Manufacturing

• Design and Modeling

Segmentation 6: by Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

Europe is the highest-growing market among all the regions, registering a CAGR of 13.09%. European countries are known for their expertise in space research and development, with multiple renowned space agencies, primordially the European Space Agency (ESA), playing a pivotal role in space exploration and technology development. These agencies collaborate with industry-leading companies, research institutions, and universities to drive innovation and push the boundaries of advanced space composites’ performance. The European Space Agency (ESA) introduced the SpaceCarbon project under the Horizon 2020 Programme. This project’s objective is to develop Europe-based carbon fibers (CF) and pre-impregnated materials for launchers and satellite applications.

Recent Developments in the Global Advanced Space Composites Market

• In July 2023, Orbital Composites won a $1.7 million contract from the U.S. Space Force to develop its technological capabilities to facilitate in-orbit manufacturing of satellite antennas.

• In June 2023, Beyond Gravity won a contract from ESA to develop the payload fairing for the Ariane 6 launch vehicle. The payload fairing is 14 meters and 20 meters tall for the respective variants of the launch vehicle and will have a standard diameter of 5.4 meters.

• In November 2022, MT Aerospace AG won a $33.5 million contract from ESA for developing demonstrator systems made of carbon fiber-reinforced polymer (CFRP) for the Prototype for a Highly OptimizEd Black Upper Stage (PHOEBUS) project, which would be incorporated in the Innovative Carbon Ariane Upper Stage (ICARUS) of the Ariane 6 family of launch vehicles.

• In October 2022, Beyond Gravity won a contract to supply 38 payload fairings for ULA’s Vulcan rockets, which would be used to launch the satellites of Amazon’s project Kuiper.

• In March 2022, Beyond Gravity and Amazon announced a partnership to develop and manufacture customized composite satellite dispenser systems for Project Kuiper. The project aims to establish a low Earth orbit (LEO) constellation comprising 3,236 satellites.

Demand – Drivers, Challenges, and Opportunities

Market Demand Drivers:

The surging number of satellite launches and the increasing scope of deep space activities is driving the requirements for advanced space composites. The advanced space composites industry stands poised for significant expansion. Companies specializing in advanced composites, equipped with deep expertise in composite manufacturing processes, material development, and structural design, are strategically positioned to capture the array of opportunities that this burgeoning market segment has. By delivering cutting-edge composite solutions tailored to the specific needs of space missions, these companies can propel technological advancements, elevate mission capabilities, and actively contribute to the advancement of space exploration.

Market Challenges:

The high cost associated with space composites poses a significant business challenge for the advanced space composites industry. While these materials offer exceptional performance and unique properties necessary for space applications, their production, development, and implementation can be prohibitively expensive. One of the primary contributors to the high cost of space composites is the intricate manufacturing process. Advanced space composites often require specialized manufacturing techniques, such as filament winding, autoclave curing, or additive manufacturing with high-performance polymers or carbon fibers. These techniques involve complex machinery, precise control of environmental conditions, and skilled labor, all of which contribute to elevated production costs. Additionally, the stringent quality control and testing requirements for space-grade composites further increase expenses. These factors also add inflexibility for rapid component development in hardware-rich approaches.

Market Opportunities:

Manufacturing complex composite structures using conventional methods presents significant challenges in terms of difficulty and time consumption. However, additive manufacturing offers a solution by enabling precise layer-by-layer deposition of composite materials, allowing for the creation of geometrically complex and specialized structures. This innovative technology enables the fabrication of internal features and graded material compositions that are otherwise difficult or impossible to achieve using traditional subtractive manufacturing techniques. The field of additive manufacturing for composites has seen notable advancements, including the utilization of novel feedstock materials such as continuous fibers, nanoparticles, and functional fillers, which enhance the mechanical, thermal, and electrical properties of printed composites. Furthermore, the development of hetero-material and differential method printing capabilities has expanded the design possibilities and performance of composite materials for space applications.

Analyst’s Thoughts

Nilopal Ojha, Principal Analyst, BIS Research, states, “The growing number of space assets, particularly launching small satellites for satellite constellations and increasing use of reusable launch vehicles, has increased the demand for space composites. The need for composites for manufacturing lightweight and durable satellite and launch vehicle components is expected to propel the advanced space composites market during the forecast period.”

Focus on Platform, Component, Material, Manufacturing Process, Service, and Country - Analysis and Forecast, 2023-2033

The key trends in the global advanced space composites market are:

• Additive manufacturing of advanced composites has significant potential for enhancing the production capability of specialized space components with complex geometrical profiles. Additive manufacturing of advanced composites also holds great potential for in-space manufacturing solutions. Made In Space and Orbital Composites are the key players with developments in composite additive manufacturing for in-space manufacturing solutions.

• The developments in in-space transportation systems have significant implications for the advanced space composites market. As these transportation systems become more efficient, reliable, and versatile, they enable a wide range of space missions, including satellite deployments, servicing, and interplanetary exploration, increasing the demand for advanced space composites.

The global advanced space composites market is witnessing the developments of major key players such as Toray Advanced Composites, Hexcel Corporation, Beyond Gravity, Rock West Composites, Inc., and MT Aerospace AG, which are capable of providing various advanced materials for the requirements of the space agencies and NewSpace ecosystem. Key players are targeting the diverse market via contracts, agreements, and partnerships for facilitating the development and deployment of these advanced materials in space systems. Startups are primarily targeting specialized advanced materials that have very specific applications as the markup factor for their offering’s differentiation.

The following can be seen as some of the USPs of the report:

• A dedicated section on growth opportunities and recommendations

• A qualitative and quantitative analysis of the advanced space composites market based on programs and systems

• Quantitative analysis of the product sub-segment, which includes:

• By Material

o Carbon Fiber

o Glass Fiber

o Thermoset

o Thermoplastic

o Nanomaterials

o Ceramic Matrix Composites (CMC) and Metal Matrix Composites (MMC)

o Others

• By Manufacturing Process

o Automated Fiber Placement (ATL/AFP)

o Compression Molding

o Additive Manufacturing

o Others

• By Service

o Repair and Maintenance

o Manufacturing

o Design and Modeling

• A detailed company profile comprising established players and growing startups

Companies facilitating the development of the space economy, which includes advanced materials manufacturers, launch vehicle developers, space systems developers, and NewSpace startups, are the primary target audience. Additionally, investors and venture capitalists potentially pursuing the space sector as a part of their investment thesis should also buy this report to get insights about the emerging advanced space composites demand and how they could benefit from it.

The space carbon fiber composite market was valued at $393.6 million in 2022 and is projected...

The global SiC fibers market is expected to reach $2,519.2 million by 2031, with a CAGR of...