A quick peek into the report

Introduction to the Agriculture Imaging Sensor Market

The global agriculture imaging sensor market has experienced remarkable growth, with North America taking the lead in adopting and advancing this technology. A pivotal report from the United States Department of Agriculture (USDA) in February 2023 shed light on the notable adoption of digital agriculture technologies within the U.S. farm sector from 1996 to 2019. The report emphasized the substantial integration of yield maps, soil maps, and variable rate technologies (VRT) on corn and soybean acreage, indicating a long-standing commitment to technological advancements. The prevalent use of imaging sensors for digital mapping activities suggests a rising demand for these sensors in the U.S. throughout the forecast period.

The global agriculture imaging sensor market is witnessing a transformative shift, with multispectral sensors emerging as a dominating product segment. Multispectral sensors offer the capability to capture data across various wavelengths, providing farmers with crucial insights into crop health, nutrient levels, and pest infestations. This advanced technology enables precise decision-making, optimizing agricultural practices for increased yields and resource efficiency.

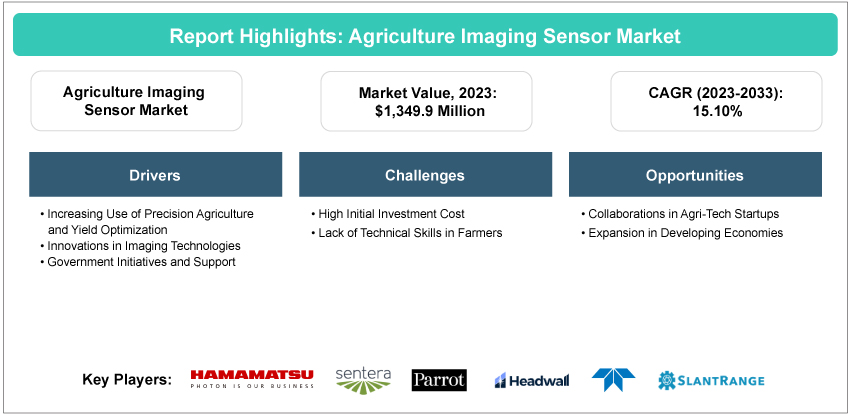

The global agriculture imaging sensor market was valued at $1,349.9 million in 2023 and is expected to reach $5,509.7 million by 2033, following a CAGR of 15.10% during 2023-2033.

Factors Influencing Market Expansion:

• Increasing adoption of precision agriculture practices

• Growing demand for drone-based agriculture solutions incorporating imaging sensors for real-time monitoring.

Industrial Impact

The agriculture imaging sensor market is marked by a competitive landscape, with key players such as Teledyne Technologies Incorporated, Fototerra, Sony Semiconductor Solutions Corporation, Omnivision Technologies, Inc., Hamamatsu Photonics K.K, and Parrot Drone SAS leading the industry. In 2022, these companies collectively held approximately 34% of the market share. The market exhibits both competitive and fragmented characteristics, as several players contribute to the diverse ecosystem of agricultural imaging solutions. Teledyne Technologies, with its advanced imaging technologies, and Micasense, specializing in multispectral sensors, are prominent players, along with Sony Semiconductor Corporation, Omnivision, Hamamatsu Photonics K.K, and Parrot Drone SAS, collectively shaping the evolving landscape of agricultural imaging sensor technologies. Teledyne Technologies, known for its advanced imaging technologies, has been at the forefront with innovations such as its state-of-the-art multispectral sensors catering to the precision agriculture sector.

Market Segmentation:

Segmentation 1: by End User

• Agriculture Robot Manufacturer

• Agriculture Drone Manufacturer

• Livestock Monitoring Equipment Manufacturer

• Others

Agriculture Drone Manufacturer to Dominate the Agriculture Imaging Sensor Market (by End User)

The agriculture drone manufacturing segment is poised to become a dominant force in the global agriculture imaging sensor market, indicating a pivotal shift toward precision agriculture. Companies operating in this space increasingly focus on developing and integrating advanced imaging sensors into their drone technologies to enhance crop monitoring and management capabilities. As an example, DJI unveiled the Mavic 3 Multispectral drone in November 2022, which is specifically crafted for precision agriculture and environmental monitoring. This drone is outfitted with an advanced multispectral imaging system, swiftly capturing crucial crop growth data to enhance overall crop production effectiveness.

As agriculture drone adoption continues to rise globally, propelled by the demand for efficient and data-driven farming practices, the role of imaging sensors in this sector is expected to grow significantly.

Segmentation 2: by Product

• RGB Sensor

• Hyperspectral Sensor

• Multispectral Sensor

• Others

Multispectral Sensor to Dominate the Agriculture Imaging Sensor Market (by Product)

The global agriculture imaging sensor market is witnessing a transformative shift, with multispectral sensors emerging as a dominating product segment. Multispectral sensors offer the capability to capture data across various wavelengths, providing farmers with crucial insights into crop health, nutrient levels, and pest infestations. This advanced technology enables precise decision-making, optimizing agricultural practices for increased yields and resource efficiency.

Key industry players recognize the potential of multispectral sensors and actively contribute to their dominance in the market. MicaSense is a leading player in multispectral sensor development, with its RedEdge-MX camera designed for unmanned aerial systems showcasing its capabilities in accurate multiband data collection for agricultural remote sensing. The integration of such technology is presented as a game-changer for farmers, enabling informed decision-making and maximizing yield potential while reducing labor costs.

Segmentation 3: by Region

• North America - U.S., Canada

• Europe - Germany, France, U.K., Belgium, Spain, Italy, Ukraine, and Rest-of-Europe

• Asia-Pacific - Japan, China, Australia, and Rest-of-Asia-Pacific

• Latin America - Brazil, Mexico

• Middle East and Africa - South Africa, Turkey, and Rest-of-Middle East and Africa

The North America agriculture imaging sensor market has been experiencing substantial growth and presents numerous opportunities. The North America agriculture imaging sensor market is experiencing a significant growth rate, characterized by a competitive environment with several key players. Companies such as Teledyne DALSA, Phototerra, and Surface Optics Corporation are major contributors to the market. The market is highly fragmented, with intense competition among major players such as Canon Inc., Samsung, Sony, and others. While fostering innovation, this competitive environment also puts pressure on pricing and market share, making it challenging for new entrants and smaller companies to establish a foothold.

Recent Developments in the Agriculture Imaging Sensor Market

• In October 2023, Hamamatsu Photonics achieved a significant milestone by creating an innovative near-infrared area image sensor. This sensor boasted remarkable features, including enhanced speed and an impressive dynamic range that has doubled in comparison to existing hyperspectral camera products. Referred to as the G16564-0808T, this sensor is constructed using a combination of indium, gallium, and arsenic materials.

• In January 2023, OMNIVISION Technologies, Inc. introduced its latest innovation, the OV50H, a high-resolution 50-megapixel (MP) image sensor equipped with dual conversion gain (DCG) technology and 1.2-micron (µm) pixels. This sensor was designed to cater to the needs of high-end smartphone rear-facing cameras, boasting flagship-level performance and autofocus capabilities in low-light conditions. It supports impressive specifications, including 12.5MP at 120 frames per second (fps) and high dynamic range (HDR) at 60 fps. Notably, the OV50H also marks a milestone as OMNIVISION Technologies, Inc.'s first sensor to incorporate horizontal/vertical (H/V) quad-phase detection (QPD) technology.

• In April 2023, Teledyne Technologies Incorporated successfully provided the CIS115 CMOS sensor for integration into JUICE's optical camera, known as JANUS. This sensor boasts a 3-megapixel capacity and a pixel pitch of 7µm. Once deployed, the JANUS camera equipped with this sensor will deliver remarkable imaging capabilities, offering a stunning resolution of up to 2.4 meters when observing Ganymede and providing clear imagery at distances of approximately 10 kilometers.

• In June 2020, OMNIVISION Technologies, Inc. introduced an automotive image sensor, the OX03C10 ASIL-C. This sensor is a pioneering solution designed for viewing applications in the automotive sector, setting new standards in image quality. The sensor combines a generous 3.0-micron pixel size with an impressive high dynamic range of 140 dB.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Increasing Use of Precision Agriculture and Yield Optimization

Precision agriculture relies heavily on detailed, real-time crop data. Image sensors, particularly drones and satellites, enable detailed monitoring of crop health, identifying issues such as disease, nutrient deficiencies, and water stress. This information helps in making timely interventions to improve crop yields. For instance, companies such as AgEagle Aerial Systems provide drone-based imaging solutions that have been instrumental in enhancing crop monitoring efficiency. The integration of image sensors with IoT and AI technologies is enhancing the capabilities of precision agriculture. These integrations allow for more sophisticated data analysis and decision-making processes, leading to smarter farming practices. An example is the collaboration between sensor manufacturers and AI companies to develop predictive analytics for crop management.

The adoption and growth of precision agriculture vary significantly by region. North America is currently the largest market, while Asia-Pacific is anticipated to witness significant growth, driven by government initiatives and the adoption of modern farming technologies. This regional growth is crucial for understanding the global spread and acceptance of precision agriculture. Image sensors facilitate the precise application of resources such as water, fertilizers, and pesticides. This targeted approach, supported by data from sensors, optimizes resource usage and reduces wastage. For instance, the use of multispectral imaging sensors in precision irrigation systems has improved water usage efficiency in agriculture.

Market Challenges: High Initial Investment Cost

The cost of advanced imaging sensors and related technology, which includes drones, satellite imaging, and IoT-enabled devices, can be prohibitively expensive for many farmers. The integration of these technologies into regular farming operations often requires a substantial upfront investment. High-end drones equipped with sophisticated imaging sensors, for example, come with a steep price tag. Additionally, these systems usually necessitate complementary investments in software and data analytics tools, adding to the overall expense.

The implementation of imaging sensor technology in agriculture is not just about purchasing equipment; it also involves the cost of training personnel and adapting existing farm management practices. Farmers must invest time and resources to learn how to effectively utilize these technologies and integrate the data into their decision-making processes. This learning curve can be steep and time-consuming, requiring ongoing training and support. The adoption of imaging sensor technology also carries an element of financial risk. Agriculture is inherently influenced by external factors such as weather, market fluctuations, and policy changes. Investing a significant amount of capital into a technology-dependent farming approach can be risky, especially for smaller operations that may not have the financial resilience to absorb potential losses.

Market Opportunities: Collaborations in Agri-Tech Startups

Collaborations and partnerships in the agriculture imaging sensor market represent significant opportunities, fostering innovation, market expansion, and technological advancements. These alliances are crucial in overcoming challenges such as high costs, technical complexities, and market penetration barriers. The increasing number of partnerships between Agri-Tech companies is a key factor for the growing opportunities in the agriculture imaging sensor market. For instance, in 2023, FRAMOS' collaborated with NXP Semiconductors, which enhanced its capabilities in mastering the unique aspects of image sensor technology. This partnership granted FRAMOS access to specialized technical support, allowing its engineers and developers to utilize innovative sensor features that go beyond standard implementations. This collaboration empowers FRAMOS to extract optimal image quality from image signal processors. FRAMOS offers a range of services, including RAW IQ characterization, system-level processed IQ characterization, IQ optimization, and the development of custom IQ tests, reports, and tuning. Collaborations between tech companies and academic institutions or research organizations are instrumental in driving innovation. For example, a tech firm partnering with a university's agricultural department can lead to the development of new, more efficient sensor technologies.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The agriculture imaging sensor market is likely to grow multi-fold in the coming years, owing to the rapidly growing demand for sustainable and ethical alternatives to conventional agriculture products. This increased interest aligns with increasing environmental awareness, shifting consumer preferences, and advancements in biotechnology, creating a favorable landscape for the widespread acceptance and expansion of the agriculture imaging sensor industry. Moreover, substantial investments in the agriculture imaging sensor market further reinforce its growth potential. As investors recognize the economic and environmental benefits of imaging sensors, increased funding is facilitating research, development, and scaling of production processes. The market is expected to witness significant growth in the coming years, and the key players in the market are focused on strategic partnerships, collaborations, mergers, and acquisitions to expand their market presence and enhance their product offerings.”

Agriculture Imaging Sensor Market - A Global and Regional Analysis

Focus on Application, Product, and Region - Analysis and Forecast, 2023-2033

Frequently Asked Questions

Ans: The agriculture imaging sensor market was valued at $1.23 billion in 2022, which is expected to grow at a CAGR of 15.10% and reach a value of $5.5 billion over the forecast period 2023-2033.

Ans: Agriculture imaging sensors, also known as agricultural imaging systems, are specialized sensors and cameras designed for capturing images and data related to agricultural environments and activities. These sensors play a crucial role in modern agriculture by providing valuable information to farmers, researchers, and agricultural professionals. These can be included in autonomous tractors, robotic harvesters, and other automated tools guided by technologies such as GPS and sensors. Their use enhances efficiency, reduces labor dependence, and optimizes agricultural processes.

Ans: Prominent players in the autonomous farm equipment market include industry leaders such as Hamamatsu Photonics K.K., OMNIVISION Technologies, Inc., and Teledyne Technologies Incorporated. These companies are at the forefront of developing and implementing cutting-edge technologies such as imaging sensors, agriculture sensor solutions, and driverless agricultural equipment. Their strategic initiatives contribute significantly to the ongoing evolution of the autonomous farm equipment landscape, shaping the future of precision agriculture with innovations that enhance efficiency and sustainability in farming practices. Some other players, such as Parrot Drone SAS, are manufacturing autonomous drones that simplify operations such as field surveillance and spraying seamlessly.

Ans: Imaging sensors are extensively used in agriculture for a wide range of applications due to their ability to capture visual and non-visible information about crops, soil, and environmental conditions. Imaging sensors, often integrated with drones or ground-based platforms, capture high-resolution images of crops. These images help monitor crop health, growth stages, and potential issues such as pests and diseases. Farmers can identify areas that need attention and take corrective measures.

Ans: High-quality agriculture imaging sensors can be expensive to purchase and maintain. This cost can be a barrier for small-scale farmers or agricultural operations with limited budgets. Interpreting the data captured by imaging sensors often requires specialized knowledge and software. Farmers may need training to analyze the data effectively and make informed decisions. High-resolution images and multispectral data can generate large amounts of data that need to be stored and processed. Managing and analyzing this data can be resource-intensive.