Published Year: 2022

Solar-Powered Microbes Market - A Global and Regional Analysis: Focus on Type, End-Use Industry, and

Microbes such as bacteria, molds, and yeasts are utilized for the food, feed, food...

Focus on Product, Application, and Competitive Landscape, 2023-2033

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Companies involved in agrivoltaics can capitalize on this trend by investing in innovative technologies, developing partnerships with farmers and solar energy providers, and leveraging government incentives and policies supporting renewable energy. Strategic investments in research and development, along with the establishment of resilient production infrastructure, will be key for companies looking to capitalize on the expanding agrivoltaics market. By embracing these strategies, companies can position themselves as leaders in sustainable energy solutions for agriculture, shaping the future of the global agrivoltaics market and meeting the evolving needs of farmers and energy consumers worldwide.

Market Introduction

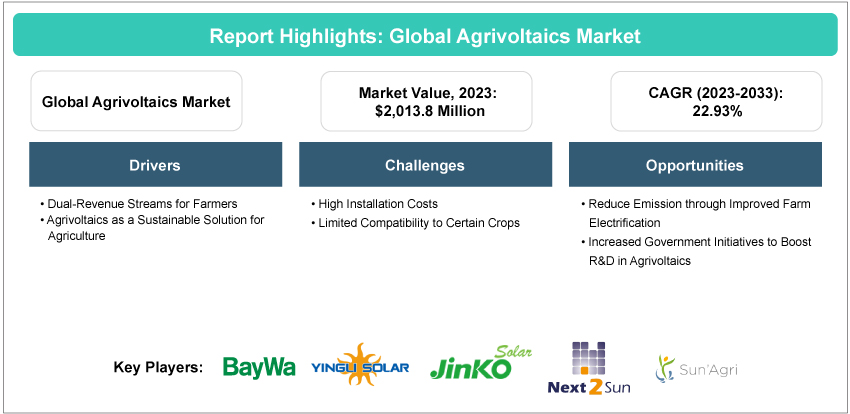

The global agrivoltaics market, which integrates solar energy production with agricultural practices, is poised for significant growth in the coming years. The market is valued at $1,768.8 million in 2022. The market is expected to expand rapidly, reaching an estimated $15,871.6 million by the end of 2033. This growth is driven by several factors, including increasing recognition of the benefits of agrivoltaics in enhancing crop yields, reducing water usage, and maximizing land efficiency. Agrivoltaics offers a sustainable and efficient solution for both energy production and agricultural land use, aligning with the global shift toward more environment-friendly practices.

Industrial Impact

The utility-scale solar farms, typically ranging from 1 MW to 2,000 MW, are known to sell their electricity to generate profits for their owners. The installation cost of solar farms usually falls between $0.89 to $1.01 per watt. On average, a 1 MW solar farm can earn around $43,500 annually by selling its electricity to utilities. Landowners who lease their land for solar farms can expect to earn between $250 to $3,000 per acre per year. These findings underscore the economic viability and potential profitability of solar farm investments.

While comparing agrivoltaics to ground-mounted PV plants, researchers have found that agrivoltaics projects tend to be more expensive. This is primarily due to higher costs incurred during the approval process and design limitations, as well as the need for specialized components such as modules, mounting systems, and trackers. For instance, the inclusion of vertical plants or elevated modules to accommodate agricultural machinery underneath can significantly raise costs. The additional expenses for these components are estimated to range from $268.68 to $303.00 per kW for modules and from $90.7 to $240.6 per kW for racks.

Market Segmentation:

Segmentation 1: by Array Configuration

• Fixed

• Single-Axis Tracking

Fixed Array to Dominate the Global Agrivoltaics Market (by Array Configuration)

The fixed array stands out as the leading segment among the various types of array configurations in the global agrivoltaics market, driven by its practicality, cost-effectiveness, and compatibility with agricultural operations. This segment represents a significant portion of agrivoltaics installations worldwide, offering a balance between solar energy generation and agricultural productivity.

One key advantage of fixed arrays is their simplicity and ease of installation, making them a preferred choice for many farmers and solar developers. Unlike tracking systems, fixed arrays do not require complex mechanisms for adjusting the angle of solar panels, reducing maintenance costs and potential points of failure. Furthermore, fixed arrays are well-suited for a variety of agricultural settings, including grassland farming, horticulture, and arable farming, providing flexibility in deployment. Their stationary nature ensures minimal disruption to farming activities, allowing crops to thrive without compromising solar energy generation.

Segmentation 2: by Photovoltaic Technology

• Monofacial Solar Panels

• Bifacial Solar Panels

• Translucent Photovoltaic Technology

• Others

Monofacial Solar Panels Segment to Dominate the Global Agrivoltaics Market (by Photovoltaic Technology)

Monofacial solar panels have emerged as the leadingly adopted photovoltaic technology in the global agrivoltaics market. This trend is driven by several factors, including cost-effectiveness, efficiency, and compatibility with agricultural activities. Monofacial panels are traditional solar panels that absorb sunlight from one side, making them ideal for installations where space is not a constraint.

One recent example highlighting the dominance of monofacial solar panels in agrivoltaics installations is the AgriPV project in the Netherlands, initiated in April 2021. This project involves the installation of monofacial solar panels on a greenhouse to generate solar power while allowing for crop cultivation underneath. The project showcases the efficiency and compatibility of monofacial panels with agricultural settings, as well as their ability to enhance land use efficiency.

Segmentation 3: by Site of Installation

• Grassland Farming

• Horticulture and Arable Farming

• Indoor Farming

• Pollinator Habitat

Pollinator Habitant Segment to Dominate the Global Agrivoltaics Market (by Site of Installation)

Pollinator habitat emerges as the leading application segment in the global agrivoltaics market, showcasing a pivotal shift toward sustainable agricultural practices and renewable energy generation. This segment not only promotes biodiversity but also enhances the ecosystem services provided by agrivoltaics systems.

A notable example is Jack’s Solar Garden, launched in June 2021, which stands as the largest agrivoltaics research project in the U.S. Located in Boulder County, Colorado, this 1.2-MW solar farm integrates all four types of vegetation, including pollinator habitats. The site features over 3,000 trees, shrubs, and other pollinator-friendly plants, demonstrating a successful blend of solar energy production and environmental conservation.

Segmentation 4: by Region

• North America: U.S. and Canada

• Europe: France, Germany, Italy, Spain, U.K., and Rest-of-Europe

• Asia-Pacific: China, Japan, India, South Korea, and Rest-of-Asia-Pacific

• Rest-of-the-World: Brazil, South Africa, and Other

North America, especially the U.S., plays a pivotal role in shaping the global agrivoltaics market, being a major contributor due to its increasing energy demands and the rising prominence of agrivoltaics as a sustainable energy source. The growth of the agrivoltaics market in the U.S. is expected to accelerate in the coming years, driven by factors such as government support, rising demand for renewable energy, and the benefits it offers to farmers.

A significant milestone in the U.S. agrivoltaics landscape was the launch of the U.S. Department of Energy's Agrivoltaics Partnership in 2020, aiming to accelerate the development and deployment of agrivoltaics technologies. In December 2022, the U.S. Department of Energy announced the Foundational Agrivoltaics Research for Megawatt Scale (FARMS) funding, allocating $8 million for six solar energy research projects across six states and the District of Columbia. This funding initiative demonstrates the government’s commitment to supporting the growth and development of the agrivoltaics market.

Recent Developments in the Global Agrivoltaics Market

• In October 2023, the National Solar Energy Federation of India (NSEFI) inaugurated the Agrivoltaics Alliance in Delhi, India. The primary aim of this initiative is to facilitate easier crop production. By achieving incremental improvements, lowering production expenses, and maximizing the utilization of natural sunlight, the country aims to mitigate the presence of adulterated vegetables in the market.

• In December 2022, the U.S. Department of Energy announced the Foundational Agrivoltaics Research for Megawatt Scale (FARMS) funding, allocating $8 million for six solar energy research projects across six states and the District of Columbia.

• In December 2023, Turkey initiated the Agrivoltaics research project, enabling researchers to evaluate both products and the production process. To facilitate this endeavor, researchers introduced tracker systems tailored for crops cultivated through Agrivoltaics methods.

Demand - Driver, Challenge, and Opportunity

Market Driver: Dual-Revenue Streams for Farmers

• Agrivoltaics systems offer farmers the opportunity to utilize the land beneath the solar panels for either livestock grazing or cultivating various crops while simultaneously generating electricity. This arrangement creates a dual-revenue stream for farmers. Agrivoltaics have been successfully implemented for berries, grapes, and orchard crops such as apples, and they are particularly suitable for shade-tolerant crops such as cauliflower or cabbage. Researchers from the University of Arizona found that growing crops in the shade from solar panels can yield two or three times more fruit and vegetables compared to conventional agricultural setups.

Market Challenge: High Installation Costs

• High installation costs have presented a significant obstacle to the widespread adoption of agrivoltaics. A primary contributing factor to these costs is the expense of photovoltaic panels. Moreover, the installation of agrivoltaic systems can be intricate, necessitating specialized expertise and equipment, further escalating expenses. The total cost of installing agrivoltaic systems can vary based on factors such as system size, complexity, location, and specific components used.

• According to a report by the National Renewable Energy Laboratory (NREL) in the U.S., the installed cost of an agrivoltaic system typically ranges from $2.60 to $4.50 per watt. In comparison, traditional ground-mounted solar systems typically cost between $1.50 to $3.00 per watt. This significant disparity in costs is likely to impede the growth of the Agrivoltaics market during the forecast period.

Market Opportunity: Reduce Emission through Improved Farm Electrification

• Agrovoltaics presents opportunities for carbon sequestration by incorporating vegetation between and around solar panels. This vegetation serves as a carbon sinks, absorbing carbon dioxide from the atmosphere and storing it in the plant biomass and soil. Through this integration of solar panels with vegetation, agrovoltaics can effectively mitigate greenhouse gas emissions and contribute to reducing the farm's overall carbon footprint.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “By harmonizing solar energy production with agricultural cultivation, agrivoltaics epitomizes innovation at the intersection of sustainability and efficiency. This synergy holds the promise of transforming traditional farming landscapes into vibrant hubs of renewable energy generation, showcasing the power of interdisciplinary solutions to address pressing global challenges.”

Focus on Product, Application, and Competitive Landscape, 2023-2033

The global agrivoltaics market refers to the integration of agriculture and photovoltaic power generation systems, allowing for dual land use. It offers benefits such as increased land productivity, water conservation, and renewable energy generation. With growing interest in sustainable practices, the agrivoltaics market is expected to expand significantly in the coming years.

Key business opportunities in the global agrivoltaics market include developing innovative technology for efficient integration of solar panels and agricultural activities, providing consulting services for optimal system design and implementation, and offering financing solutions for farmers and landowners to adopt agrivoltaic systems. Additionally, there is potential for creating partnerships between solar energy companies and agricultural stakeholders to maximize land use efficiency and sustainability.

Existing market players in the agrivoltaics industry are adopting strategies such as diversifying product portfolios to offer integrated agrivoltaic solutions, investing in research and development for improved efficiency and cost-effectiveness, and forging strategic partnerships with agricultural stakeholders and renewable energy firms to expand market reach and enhance technological capabilities.

A new company entering the global agrivoltaics market could focus on developing cutting-edge agrivoltaic technology with enhanced efficiency and adaptability to various agricultural settings. Additionally, differentiation through sustainable and environment-friendly practices, such as utilizing recycled materials or offering carbon-neutral solutions, could help establish a competitive edge. Strategic partnerships with research institutions or agricultural organizations for data-driven optimization and tailored solutions could also be pivotal for staying ahead.

The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the global agrivoltaics market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the global agrivoltaics market

• Qualitative and quantitative analysis of the global agrivoltaics market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Renewable energy companies, agricultural technology firms, investors and venture capitalists, government agencies, policymakers, and research institutions can buy this report.

Microbes such as bacteria, molds, and yeasts are utilized for the food, feed, food...