A quick peek into the report

Automotive Carbon Thermoplastic Market Overview

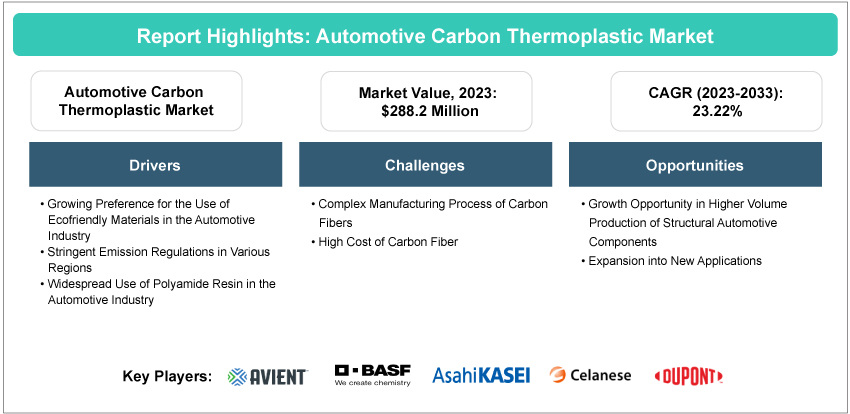

The automotive carbon thermoplastic market was valued at $288.2 million in 2023, and it is expected to grow at a CAGR of 23.22% and reach $2,325.6 million by 2033. The automotive carbon thermoplastic market thrives due to increasing demand for lightweight and durable materials in vehicle manufacturing. OEM-supplier collaborations and regulatory shifts further shape this dynamic market, focusing on reliable, efficient, and optimal performance.

Introduction of Automotive Carbon Thermoplastic Market

The automotive carbon thermoplastic market can be defined as the production, distribution, and utilization of thermoplastic composite materials reinforced with carbon fibers for automotive applications. These composite materials are created by combining a thermoplastic polymer matrix with carbon fibers, resulting in a lightweight, strong, and corrosion-resistant material with design flexibility. In the automotive industry, carbon thermoplastics are used to replace traditional materials such as metals or thermoset composites in various vehicle components. These components include interior parts, exterior body panels, structural elements, under-the-hood parts, and even battery enclosures in electric vehicles. Automotive carbon thermoplastics offer benefits such as high strength, low weight, corrosion resistance, and design versatility, making them suitable for a wide range of automotive applications.

Introduction of Automotive Carbon Thermoplastic

Automotive carbon thermoplastics, also known as carbon fiber reinforced thermoplastics (CFRTP), represent a cutting-edge advancement in automotive materials technology. These innovative materials combine the lightweight and high-strength properties of carbon fiber with the versatility and formability of thermoplastics. By integrating carbon fibers into thermoplastic matrices, automotive components can achieve remarkable strength-to-weight ratios, enhancing fuel efficiency, performance, and overall durability. CFRTPs offer superior design flexibility, allowing for complex geometries and tailored mechanical properties, making them ideal for various automotive applications, including structural components, body panels, and interior trim. As the automotive industry continues to prioritize lightweighting and sustainability, automotive carbon thermoplastics emerge as a key solution driving the evolution of next-generation vehicles.

Industrial Impact

The automotive carbon thermoplastic market's industrial impact extends across automotive manufacturing, technology development, and sustainable mobility. It contributes to energy savings and CO2 reduction in the automobile industry. This is achieved through their lightweight properties, which help improve fuel economy and reduce emissions. Carbon fiber-reinforced thermoplastic composites are highly durable, lightweight, and resistant to deformation alkaline and acid corrosion. They are designed to meet the demanding requirements of the automotive sector, providing a balance of strength, weight, and performance. Manufacturers increasingly prefer automotive carbon thermoplastics to reduce vehicle weight, enhance sustainability, and improve overall performance and efficiency.

The key players operating in the automotive carbon thermoplastic market include Avient Corporation, Asahi Kasei Corporation, BASF SE, Celanese Corporation, COMPLAM Material Co., Ltd., Solvay, DuPont, Mitsubishi Chemical Group Corporation, SABIC, SGL Carbon, TEIJIN LIMITED, DowAksa, Hexcel Corporation, Covestro AG, and Toray Industries Inc., among others. These companies are focusing on strategic partnerships, collaborations, and acquisitions to enhance their product offerings and expand their market presence.

Market Segmentation:

Segmentation 1: by Application

• Exterior

• Interior

• Chassis

• Powertrain and Under the Hood

• Others

Exterior Application to Dominate the Automotive Carbon Thermoplastic Market (by Application)

The exterior application of automotive carbon thermoplastics is poised to lead the market due to several key factors. As automakers strive to improve fuel efficiency, reduce emissions, and enhance vehicle performance, lightweight materials such as carbon thermoplastics offer a compelling solution for exterior components.

In the exterior application segment, carbon thermoplastics are commonly used for body panels, hoods, roofs, fenders, and other exterior body parts. These components benefit from the material's high strength-to-weight ratio, which allows for weight reduction without compromising structural integrity. Additionally, carbon thermoplastics offer excellent resistance to corrosion and impact, making them well-suited for exterior applications where durability is crucial.

Furthermore, carbon thermoplastics provide automotive designers with greater flexibility in styling and aerodynamics, allowing for the creation of sleeker and more aerodynamic vehicle designs. This design freedom enables automakers to differentiate their vehicles in a competitive market while meeting stringent regulatory standards for fuel efficiency and emissions.

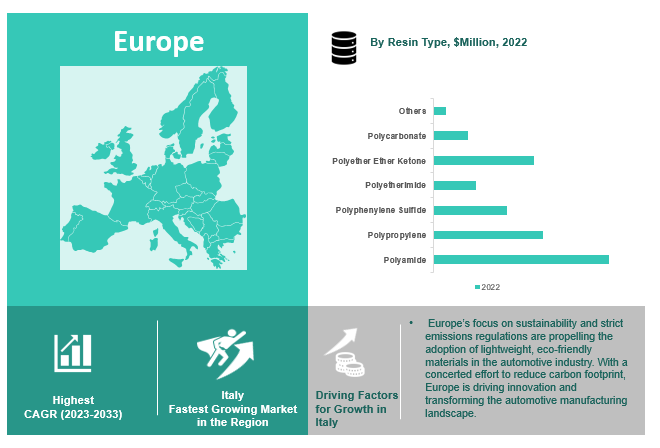

Segmentation 2: by Resin Type

• Polyamide

• Polypropylene

• Polyphenylene Sulfide

• Polyetherimide

• Polyether Ether Ketone

• Polycarbonate

• Others

Polyamide Resin to be Dominant in the Automotive Carbon Thermoplastic Market (by Resin Type)

The polyamide resin type is anticipated to lead the automotive carbon thermoplastic market owing to its unique combination of properties that make it well-suited for automotive applications. Polyamide resins, commonly known as nylon, offer a balance of strength, stiffness, toughness, and chemical resistance, making them ideal for use in various automotive components. In automotive applications, polyamide resins are commonly used for interior and exterior parts such as door panels, instrument panels, bumpers, and under-the-hood components. Their excellent impact resistance and dimensional stability make them suitable for parts requiring durability and precision. Moreover, polyamide resins exhibit good resistance to heat and chemicals, ensuring performance in harsh operating conditions.

Furthermore, polyamide resins can be reinforced with carbon fibers to enhance their mechanical properties, including strength and stiffness, without significantly increasing weight. This makes them particularly attractive for lightweighting initiatives aimed at improving fuel efficiency and reducing emissions in vehicles. While other resin types such as polypropylene, polyphenylene sulfide, and polycarbonate also offer advantages in specific applications, the versatility and overall performance of polyamide resins position them as a leading choice for automotive carbon thermoplastic solutions. As automotive manufacturers continue to prioritize lightweight materials and innovative design, the demand for polyamide-based carbon thermoplastics is expected to grow, driving their dominance in the market.

Segmentation 3: by Region

• North America: U.S., Canada, and Mexico

• Europe: Germany, France, Italy, Spain, U.K., and Rest-of-Europe

• Asia-Pacific: China, Japan, South Korea, India, and Rest-of-Asia-Pacific

• Rest-of-the-World: Middle East and Africa and South America

Europe is expected to dominate the automotive carbon thermoplastic market due to stringent emission regulations and a strong emphasis on lightweight components in the automotive industry. Countries such as Germany, France, and the U.K. have significant automotive manufacturing capabilities and are at the forefront of adopting advanced materials such as carbon thermoplastics. The region benefits from a robust infrastructure for research and development, enabling continuous innovation in carbon fiber production and composite manufacturing technologies. Additionally, government initiatives and incentives aimed at promoting sustainable mobility further drive the demand for lightweight materials.

European automotive OEMs are increasingly integrating carbon thermoplastics into their vehicle designs to improve fuel efficiency, reduce emissions, and enhance overall performance. Moreover, partnerships between material suppliers, composite manufacturers, and automotive companies facilitate the development and commercialization of carbon thermoplastic solutions tailored to the region's specific market needs.

Recent Developments in the Automotive Carbon Thermoplastic Market

• In October 2023, Celanese Corporation introduced new sustainable engineering thermoplastic solutions, which are aimed at supporting manufacturers in their transition to a circular economy. These innovative materials, known as ECO-R, offer outstanding mechanical properties and other benefits while incorporating recycled content.

• In December 2022, Asahi Kasei Corporation collaborated with the National Institute of Technology, Kitakyushu College, and Tokyo University of Science to develop fundamental technology for recycling continuous carbon fiber.

• In October 2022, Avient Corporation introduced reSound Ultra-Low Carbon Footprint TPEs, which offered an industry-first cradle-to-gate product carbon footprint (PCF) range between -0.46 and -0.02 in kg CO2 equivalent kg/ product.

• In September 2021, Solvay announced the completion of its new thermoplastic composites (TPC) manufacturing plant located at its Greenville, South Carolina site, with a full production capacity of 27,000 square feet.

• In Feb 2021, BASF SE expanded its polyphthalamide (PPA) portfolio of Ultramid advanced with carbon-fiber reinforced grades with fillings of 20, 30, and 40 percent. The new carbon-fiber (CF) reinforced grades can be used to manufacture automotive structural parts for the body, chassis and powertrain, pumps, fans, gears, and compressors in industrial applications, as well as for stable and ultra-lightweight components in consumer electronics.

Demand - Drivers, Limitations, and Opportunities

Market Demand Driver: Growing Preference for the Use of Ecofriendly Materials in the Automotive Industry

The automotive industry is undergoing a significant transformation toward sustainability, with manufacturers increasingly adopting eco-friendly materials in their production processes. Initiatives such as using recycled materials, bio-based thermoplastics, and plastic alternatives are gaining attention, driven by the industry's commitment to sustainability.

For instance, in January 2022, UBQ Materials, a company known for its innovative thermoplastic derived entirely from landfill-bound waste, announced a collaboration with Mercedes-Benz. The all-electric Mercedes-Benz VISION EQXX features UBQ bio-based thermoplastic in various components, including the vehicle's body shell and interior structures, such as headrests. Unlike conventional automobiles that rely on petroleum-based plastics, Mercedes-Benz opted for UBQ Materials' sustainable alternative to enhance the sustainability profile of the VISION EQXX. Additionally, UBQ was utilized in the bionic structure of the car's body shell and interior elements.

Market Challenge: Complex Manufacturing Process of Carbon Fibers

The challenge faced in machining carbon fiber is its complex manufacturing process. Carbon fiber is known for being an abrasive material, which increases tool wear and poses difficulties in managing waste, dust, and tools during machining. The material's low thermal conductivity further complicates machining, as it leads to heat buildup and risks delamination of the material's layers. Additionally, the process of carbon fibers demands precise supervision at each stage. The enhancement of the carbon fiber microstructure commences during the polymerization phase and continues throughout the entirety of production. Any error at any stage can impact the characteristics of the product.

Moreover, the production of carbon fiber dust poses health hazards and creates a hazardous working environment. The production process involves subjecting it to high-temperature heat treatment, which consumes a significant amount of energy and results in the emission of substantial quantities of carbon dioxide.

Despite these challenges, the industry is making remarkable progress in overcoming them. Efforts are underway to minimize defects, optimize manufacturing processes, explore alternative precursors, innovate in the development of advanced carbon fibers, and positively impact the automotive carbon thermoplastic market by enhancing the performance and sustainability of automotive components, thereby driving further adoption of carbon fiber-based materials in the industry.

Market Opportunity: Growth Opportunity in Higher Volume Production of Structural Automotive Components

Composites are emerging as a fundamental material of choice for automotive OEMs, serving both structural (such as hoods, roofs, doors, fenders, deck lids, front ends, seats, and powertrains) and non-structural (including dashboards and under-the-hood components) applications. Despite their potential, widespread adoption has been constrained by factors such as high material costs, extended production cycles, and limited automation. However, the landscape is poised for transformation in the coming years, driven by anticipated reductions in the cost of carbon fiber and the implementation of automated processes with shorter cycle times, enabling large-scale production of automotive components.

Additionally, the automotive industry's shift toward electric and hybrid vehicles further amplifies the demand for lightweight materials such as carbon thermoplastics. As automakers strive to maximize driving range and battery efficiency, the adoption of carbon thermoplastics in vehicle construction becomes imperative.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The automotive carbon thermoplastic market is likely to grow multi-fold in the coming years, owing to the rapidly growing demand for light-weighted vehicles. Moreover, huge investments in the form of subsidies and infrastructure development by government and federal agencies to promote the cut down of carbon dioxide emissions are expected to further fuel the growth of automotive carbon thermoplastic. The market is expected to witness significant growth in the coming years, and the key players in the market are focused on strategic partnerships, collaborations, mergers, and acquisitions to expand their market presence and enhance their product offerings.”

Automotive Carbon Thermoplastic Market

A Global and Regional Analysis, 2023-2033

Frequently Asked Questions

Ans: The market study conducted by BIS Research considered the definition of automotive carbon thermoplastic as the production, distribution, and utilization of thermoplastic composite materials reinforced with carbon fibers for automotive applications. These composite materials are created by combining a thermoplastic polymer matrix with carbon fibers, resulting in a lightweight, strong, and corrosion-resistant material with design flexibility. In the automotive industry, carbon thermoplastics are used to replace traditional materials such as metals or thermoset composites in various vehicle components. These components include interior parts, exterior body panels, structural elements, under-the-hood parts, and even battery enclosures in electric vehicles. Automotive carbon thermoplastics offer benefits such as high strength, low weight, corrosion resistance, and design versatility, making them suitable for a wide range of automotive applications.

Ans: The key business opportunities in the automotive carbon thermoplastic market are stringent regulations by government bodies and gaining a competitive edge through innovation.

Ans: The automotive carbon thermoplastic market is poised to grow over time, compelling companies to come up with collaborative strategies to sustain themselves in the intensely competitive market. Companies with an identical product portfolio and a need for additional resources often partner and come together for joint venture programs, which help the companies gain access to one another’s resources and facilitate them to achieve their objectives faster.

Ans: A new entrant can focus on partnering with existing automotive carbon thermoplastic manufacturers. Also, start-ups can focus on funding, launching new innovative products, and expanding their sales and distribution networks.

Ans: The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the automotive carbon thermoplastic market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the automotive carbon thermoplastic market landscape

• Qualitative and quantitative analysis of the automotive carbon thermoplastic market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Ans: Automotive carbon thermoplastic manufacturers, raw material suppliers, component manufacturers, and OEMs can buy this report.