A quick peek into the report

Global Carbon Capture Utilization and Storage Industry Overview

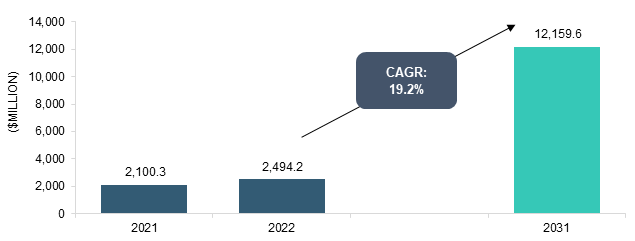

The global carbon capture utilization and storage (CCUS) market was valued at $2,100.0 million in 2021 and is expected to reach $12,159.6 million by 2031, growing at a CAGR of 19.2% between 2022 and 2031. The growth in the global carbon capture utilization and storage market is expected to be driven by an increasing focus on reducing carbon emissions and the growing demand for enhanced oil recovery (EOR). Lack of storage facilities and leakage of CO2 from underground storage are some key restraining factors of the industry.

Market Lifecycle Stage

The global carbon capture utilization and storage market is still in a nascent phase. New capturing technologies such as bio-based capturing and membrane capturing are expected to reduce the carbon capture process cost.

Figure: Global Carbon Capture Utilization and Storage Market Snapshot, $Million, 2021, 2022, and 2031

Industrial Impact

With an increased worldwide focus on achieving net-zero emissions, the shift to eco-friendly industrial practices increases financing opportunities. The shift is more prominent in the oil and gas industry in regions such as North America and the Middle East. The U.S. has the largest carbon capture utilization and storage industry as oil and gas companies use captured carbon for enhanced oil recovery.

Impact of COVID-19

The impact of COVID-19 on carbon capture utilization and storage (CCUS) was limited as it has still not been commercialized. Also, most investments toward CCUS plants were announced prior to the pandemic and are currently in the construction phase.

The new plants, such as the iCORD project in Croatia and Dry Fork Power Plant in the U.S., will start operation in 2025. Therefore, due to the delayed nature of the industry, it did not suffer any significant impact.

Market Segmentation

Segmentation 1: by Application

o Oil and Gas Industry

o Power Industry

o Others (Cement Industry and Chemical Industry)

The oil and gas industry accounts for a 61.7% share of the global CCUS market. Enhanced-oil recovery is the key industrial use of CO2, wherein pressurized CO2 is injected into oil and gas reservoirs to extract more hydrocarbons.

Segmentation 2: by Capture Technology

o Pre-Combustion Carbon Capture

o Post-Combustion Carbon Capture

o Oxy-Fuel Combustion Carbon Capture

The post-combustion carbon capture technology accounts for 95% of the global CCUS market; since it is commercially viable compared to other technologies.

Segmentation 3: by Region

o North America - U.S. and Canada

o Europe - Belgium, Norway, Croatia, Iceland, and Rest-of-Europe

o Asia-Pacific - China and Australia

o Middle East– U.A.E., Qatar, and Saudi Arabia

o Rest-of-the-World - South America and Africa

North America accounts for a 68% share of the global CCUS market, owing to the presence of operational CCUS plants in the U.S. (Texas, Wyoming) and Canada (Saskatchewan, Alberta).

Recent Developments in Global Carbon Capture Utilization and Storage Market

• In March 2022, ExxonMobil Corporation announced hydrogen production facility, carbon capture, and storage projects at its integrated refining and petrochemical site in Baytown, Texas, U.S. This would support companies in reducing emissions from local industries and company operations.

• In November 2021, ExxonMobil Corporation and Petronas signed a Memorandum of Understanding (MoU) to collaborate and jointly explore potential carbon capture and storage projects in Malaysia. This MoU would strengthen a decades-long strategic partnership between ExxonMobil and Petronas and has the objective of helping Malaysia reduce emissions and achieve its net-zero ambitions.

• In May 2021, Linde plc was selected by the U.S. Department of Energy’s National Energy Technology Laboratory (NETL) to install and test a 200 tons/day CO2 capture large pilot plant at the City Water, Light & Power (CWLP) power plant in Springfield, IL. The project would be executed in collaboration with the BASF, the University of Illinois at Urbana Champaign, ACS, and CWLP. The operation of this facility provides an opportunity to demonstrate economically attractive and innovative capture techniques.

• In May 2021, Linde plc was selected by the U.S. Department of Energy’s National Energy Technology Laboratory (NETL) to install and test a 200 tons/day CO2 capture large pilot plant at the City Water, Light & Power (CWLP) power plant in Springfield, IL. The project will be executed in collaboration with the BASF, the University of Illinois at Urbana Champaign, ACS, and CWLP.

Demand – Drivers and Limitations

Following are the demand drivers for the global carbon capture utilization and storage market:

• Favorable Government Policies Driving the Deployment of CCUS Technology

• Increasing Demand for CO2 for Enhanced Oil Recovery (EOR)

• Rise in Adoption of Net-Zero Emissions Targets

The market is expected to face some limitations too due to the following challenges:

• High Initial Cost of Carbon Capture Utilization and Storage Process

• CO2 Leakage from the Underground Storage Reservoirs

Analyst Thoughts

According to Pooja Tanna, Lead Analyst, BIS Research, "The carbon capture utilization and storage is expected to be the best option for reducing carbon footprints. With the increasing investments globally and the rising government support through incentives, the growth of the CCUS industry is expected to be exponential.”

Carbon Capture Utilization and Storage Market - A Global and Regional Analysis

Focus on Application, Type, and Region - Analysis and Forecast, 2022-2031

Frequently Asked Questions

According to International Energy Agency (IEA), carbon capture, utilization, and storage, or CCUS, is an important emissions reduction technology applied across the energy system. CCUS technologies involve the capture of carbon dioxide (CO2) from fuel combustion or industrial processes, the transport of CO2 via ship or pipeline, and its use as a resource to create valuable products or services or its permanent storage deep underground in geological formations. CCUS technologies also provide the foundation for carbon removal or "negative emissions" when the CO2 comes from bio-based processes or directly from the atmosphere.

The key trends in the carbon capture utilization and storage market include implementing CCUS technology in various industrial plants, such as power and chemical, and introducing new and cost-effective capturing technology.

The carbon capture utilization and storage market has seen major development by key players operating in the market, such as business expansion, partnership, collaboration, and joint venture. According to BIS Research analysis, the majority of the companies have adopted partnership and collaboration strategies.

A new entrant can focus on developing and providing new carbon capture technology that is cost-effective and fulfills the climate goals set by the government and companies.

• Market ranking analysis based on product portfolio, recent developments, and regional spread

• Investment landscape including product adoption scenario, funding, and patent analysis

The report is suitable for carbon capture technology providers and companies involved in capturing and storing CO2.