Published Year: 2022

Carbon Neutral Data Center Market - A Global and Regional Analysis: Focus on Product, Application an

The global carbon neutral data center market was valued at $5.02 billion in 2021 and is...

Focus on Application, Product, and Country - Analysis and Forecast, 2022-2027

Global Data Center Cooling Market Industry Overview

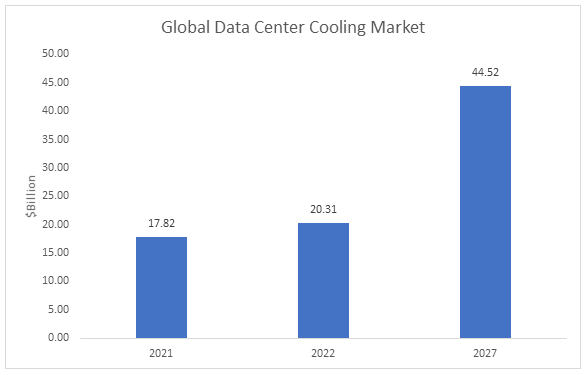

The global data center cooling market accounted for $17.82 billion in 2021 and is expected to grow at a CAGR of 16.99% and reach $44.52 billion by 2027. The growth in the global data center cooling market is expected to be driven by the increasing number of data centers and government initiatives for energy-efficient data centers. The need to address the water scarcity issue has further resulted in the adoption of data center cooling technologies.

Market Lifecycle Stage

The data center cooling market is in a growth phase. Cooling is a standard part of data center operations as servers constantly run 24/7, which increases the core temperature, which, if not controlled, can lead to a data center outage. Excess heat and humidity can damage appliances and equipment, triggering them to malfunction and stop functioning. Hence, the need of the hour is to accommodate innovative data center cooling systems in retrofits or newly built data centers. Data center cooling involves the collective equipment, tools, techniques, systems, and processes that ensure standard temperatures and humidity levels inside a data center facility. Therefore, a growing number of data centers are resulting in a boost in the utilization of data center cooling techniques.

Impact

• High-performance workloads will continue to require more power per rack, which will, in turn, require more power and cooling. However, with the right cooling technology, businesses can save space in their data centers and lower their energy costs.

• For efficient data center operations, smart technology such as artificial intelligence (AI) is used, which assists in automatic cooling control of the facility. Additionally, AI could identify issues with cooling systems before they fail and cause costly shutdowns. For instance, Google keeps its data centers cool without human intervention.

Impact of COVID-19

The lockdowns due to the pandemic affected economies around the world. Data centers were also impacted due to the COVID-19 pandemic restrictions. As a result of the pandemic, it is anticipated that the global data center cooling market is expected to grow faster in the future due to the increasing requirements to bolster IT execution, flexibility, and security across the globe. Therefore, corporations and big technology companies are adopting sustainable data center cooling technologies and systems to meet increasing data storage requirements.

Market Segmentation:

Segmentation 1: by Application

• IT and Telecom

• Banking, Financial Services, and Insurance (BFSI)

• Government and Public Sector

• Manufacturing

• Healthcare

• Retail

• Others

The IT and telecom segment is the dominating application segment. With the introduction of new technologies such as 5G, IoT, virtual and augmented reality, and artificial intelligence, the telecommunications industry is evolving to cater to huge data processing. As a result, telecom data centers are also transforming to handle high data volume and low latency needs. The banking, financial services, and insurance (BFSI) segment is expected to anticipate the highest growth rate due to being digitized, which involves utilizing the most cutting-edge technology, which will boost the data center usage, thereby augmenting the data center cooling solutions.

Segmentation 2: by Data Center Type

• Hyperscale

• Colocation

• Enterprise

• Edge Data Centers

The hyperscale segment is the dominating segment due to the demand for hyperscale data centers being driven by the need for more data and processing power.

Segmentation 3: by Solution

• Air Cooling

• Liquid Cooling

• Free Cooling

The air cooling market segment is expected to dominate the global data center cooling market because the majority of data centers are old currently and still continue to use air conditioners and other air cooling systems. Additionally, the retrofit data centers also adopt air cooling technologies. However, liquid cooling is expected to witness the highest growth rate from 2022 to 2027 as it efficiently cools the data center area, which results in less usage of fans leading to better acoustics.

Segmentation 4: by Air Cooling

• Air Conditioner

• Air Handling Unit

• Chiller

• Cooling Tower

• Economizer System

• Others

Based on air cooling, the air conditioner segment dominates the data center cooling market as it supports keeping servers cool, enhancing airflow between the aisles, treating hot air from the servers, and keeping humidity at a suitable level. Air handling units witness the second-highest growth rate after air conditioners due to their ability to maintain the mandatory environmental conditions to guarantee optimal performance and reliability of the information technology equipment (ITE) hardware.

Segmentation 5: by Liquid Cooling

• Indirect

• Direct

Based on liquid cooling, the indirect segment is expected to dominate the global data center cooling market due to the fact that it is a highly efficient way to minimize energy usage while maximizing chilling capabilities. Moreover, the direct segment witnesses a higher growth rate due to emerging cooling solutions such as direct-to-chip and immersion.

Segmentation 6: by Indirect

• In-Row

• In-Rack

Based on indirect, the in-row segment dominates the data center cooling market as it can be used for small and highly densified data centers such as edge data centers. In-row cooling units implanted between the rows are standard for removing hot air generated from the back of rows and reducing air recirculation. Furthermore, it can directly impact energy costs and power usage. However, a higher growth rate can be anticipated for the in-rack segment as in-rack is the most precise cooling technology available, which operates in a closed relationship with the air conditioner.

Segmentation 7: by Direct

• Direct-to-Chip

• Immersion

In direct-to-chip cooling, the liquid coolant absorbs heat, evaporates into a vapor, and carries heat out of the IT equipment. Therefore, this is one of the most effective and efficient forms of heat removal from the data center components, as this system cools processors directly. Thus, the direct-to-chip segment captures a significant market share as compared to the immersion cooling segment, as the latter is an emerging technology that is expected to witness a considerable growth rate in the future. This is due to immersion cooling helping to reduce electricity consumption at a much larger scale than direct-to-chip cooling and giving a greater return on investment.

Segmentation 8: by Rack Density

• Low Rack Density

• Medium Rack Density

• High Rack Density

The medium rack density (5-9 kW) captures the significant market size of the global data center cooling market. This is because around 46% of the data centers have adopted medium rack density. However, the high rack density segment is booming as it achieves better space utilization, and the response time of system failure is reduced significantly. A high rack-density data center usually consumes more than 9 kW of power; hence, it needs better airflow management to ensure efficient cooling, driving the overall data center cooling market.

Segmentation 9: by Region

• North America - U.S., Canada, and Mexico

• Europe - Germany, France, Spain, Netherlands, Italy, and Rest-of-Europe

• China

• U.K.

• Asia-Pacific - India, Japan, Australia, Singapore, and Rest-of-Asia-Pacific

• Rest-of-the-World - Middle East and Africa, and South America

North America is expected to have a massive demand for data center cooling technologies due to numerous data centers and the growing demand for innovative technologies and spending in the region.

Recent Developments in Global Data Center Cooling Market

• In September 2022, one of the most research-intensive universities in Europe, University College Dublin, received data center cooling infrastructure from Schneider Electric. The IT infrastructure at universities can benefit from the scalable, effective, and resilient cooling provided by Schneider Electric's Uniflair In-Row Direct Expansion (DX) cooling solution.

• In May 2022, the first commercial colocation provider in Asia, Digital Edge (Singapore) Holdings Pte Ltd., utilized StatePoint liquid cooling technology from Nortek Air Solutions, LLC, in its brand-new data center, NARRA1. To create the most energy and water-efficient data center in the nation, Digital Edge will utilize the sustainable cooling solution from Nortek Air Solutions, LLC

• In April 2022, as part of a restructuring program to realign its manufacturing operations, increase profitability, and boost global competitiveness, MODINE MANUFACTURING COMPANY announced the intended closure of three North American plants producing cooling packages, charge-air coolers, and oil coolers.

• In January 2022, Munters acquired EDPAC, an Irish company that makes air handling and cooling systems for data centers. Through the acquisition, Munters, a pioneer in energy-efficient data center cooling solutions in North America, expanded into Europe.

Demand – Drivers and Limitations

Following are the demand drivers for the data center cooling market:

• High-Efficient Cooling Systems

• Increasing Number of Data Centers and Spendings

• Thermal Energy Recovery Conversion from Data Centers

• Water Usage Effectiveness Driving Adoption of Alternate Cooling Solutions

• Retrofitting to a Free Cooling Data Center

The market is expected to face some limitations, too, due to the following challenges:

• High Investment Costs for Non-Conventional Cooling Systems

• Air and Free Cooling Systems Adaption Complexities

• Reliability Limitations with Immersion Liquid Cooling

• Lack of Synergy between Hardware and Cooling Vendors

• Infrastructure Development Gap between End Users and Data Centers

Analyst Thoughts

According to Debraj Chakraborty, Principal Analyst, BIS Research, “With the emerging data center cooling technologies, there are opportunities to emphasize retrofitting data centers. Data center infrastructure management (DCIM) can be facilitated with the help of better and more efficient cooling techniques. Moreover, innovative data center cooling systems will augment the number of edge data centers.”

Focus on Application, Product, and Country - Analysis and Forecast, 2022-2027

Data center cooling means the collective equipment, tools, techniques, systems, and processes that ensure standard temperatures and humidity levels inside a data center facility. Data centers use a lot of energy, which transforms into heat. The more components and servers are packed into a facility, the greater the heat generated. Appropriate data center cooling guarantees that an entire facility is supplied with sufficient ventilation, cooling, and humidity control to keep all servers within desired temperature ranges.

A few trends have resulted in augmenting the data center cooling solutions, which include increasing data requirements, increasing rack density, and 5G service leading an exponential growth of the data center cooling market. The factors driving the data center cooling market include emerging technologies, AI-assisted automatic cooling control, increasing data centers and spending, and water usage effectiveness (WUE), causing the adoption of alternate cooling solutions.

The global data center cooling market has witnessed several strategic and technological developments in the past few years undertaken by the different market players to attain their respective market shares in this emerging domain. These strategies are product development and innovation, partnerships and collaborations, business expansions, product launches and investments, and awards and recognition. The preferred strategy for the companies has been business expansion, partnership, joint venture, and collaboration to strengthen their position in the global data center cooling market.

A new entrant can focus on the liquid cooling market due to the higher growth rate in the forecast period 2022 to 2027.

• Extensive case study of the top 18 players to offer a holistic view of the global data center cooling market landscape.

• Market share analysis based on product portfolio, recent developments, and regional spread

• Patent analysis

The companies which are manufacturing and commercializing data center cooling products and services, research institutions, and regulatory bodies should buy this report.

The global carbon neutral data center market was valued at $5.02 billion in 2021 and is...

The global immersion cooling market accounted for $251.0 million in 2021 and is expected to...

The global data center liquid cooling market is expected to reach $7,723.6 million by 2026,...