Published Year: 2023

APAC Fluids and Lubricants Market for Electric Vehicles - Regional Analysis: Focus on Application, P

The APAC fluids and lubricants market for electric vehicles is projected to reach $2,363.8...

Focus on Vehicle Type, Propulsion Type, Sales Outlet, Mode of Sales, Part, and Country-Level Analysis - Analysis and Forecast, 2023-2032

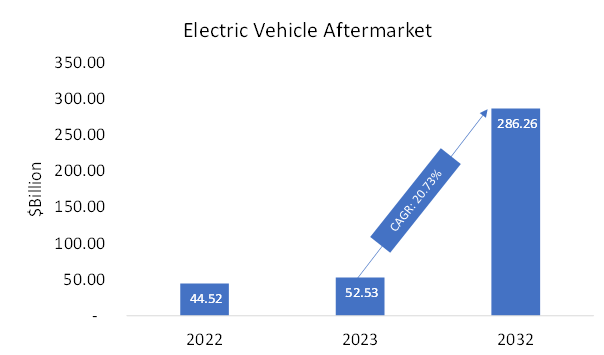

The global electric vehicle aftermarket is projected to reach $286.26 billion by 2032 from $44.52 billion in 2022, growing at a CAGR of 20.73% during the forecast period 2023-2032. The growth in the electric vehicle aftermarket is expected to be driven by the rising popularity of electric vehicles, proliferating consumer demand for electric vehicle customization, and increasing popularity of electric vehicle second-life applications.

Market Lifecycle Stage

Electric vehicles (EVs) are a pivotal technology in the pursuit of decarbonizing the road transportation sector, which contributes to approximately one-sixth of global emissions. The continued implementation of ambitious policies remains indispensable for fostering growth within the global electric vehicle markets.

Few sectors within the clean energy domain exhibit as much dynamism as the electric car industry. Recent years have witnessed remarkable growth in sales, accompanied by enhancements in driving range, broader model availability, and heightened performance standards. According to the International Energy Agency (IEA), nearly 20% of new car sales in 2023 are projected to be electric.

Should the robust growth observed over the previous two years persist, it is conceivable that by 2030, carbon dioxide emissions resulting from vehicular usage can be steered onto a trajectory that aligns with the Net Zero Emission (NZE) Scenario 2050. Nevertheless, the widespread adoption of electric vehicles remains a phenomenon yet to be fully realized on a global scale. Sales of electric vehicle aftermarket components in developing and emerging economies have encountered sluggishness, primarily due to the comparatively elevated upfront cost of electric vehicles and inadequate availability of charging infrastructure.

The electrification of lightweight vehicles presents a multifaceted challenge, given that portfolio and investment strategies have become notably intricate. Market entities operating in the aftermarket realm will be required to cater to both electric vehicles and internal combustion engine (ICE) vehicles. Additional complexities emerge as battery-electric vehicles (BEVs) exert an estimated 30% lesser demand for traditional aftermarket components compared to ICE vehicles, thereby presenting manifold challenges for the aftermarket sector.

The process of electrification ushers in an array of novel opportunities for stakeholders across the value chain. Manufacturers of automotive components can strategically transition their product portfolios to encompass BEV-specific elements and expand their operational framework to encompass remanufacturing initiatives. Collaborations with battery experts, who frequently lack post-sale capabilities, also present avenues for growth. Wholesale distributors can play a pivotal role in managing end-of-life components and may leverage their established logistics networks to engage new customer segments. Service workshops can opt for a specialized focus on BEVs or uphold a dual specialization in both ICE and BEV technologies, potentially forging partnerships with specialized service providers in the process.

Impact

The electric vehicle aftermarket is driven by several factors, such as the surge in the adoption of electric vehicles, the burgeoning consumer interest in customizing electric vehicles, and the growing trend of repurposing electric vehicles for second-life applications.

Electric vehicle aftermarket solution providers/vendors are working toward the development of advanced electric vehicle aftermarket solutions through significant investment in research and development (R&D) and partnerships with other key stakeholders in the electric vehicle ecosystem. With rapidly rising demand for electric vehicles, increasing emphasis on policies, subsidies, and investment by the governing bodies, and shifting the focus of automakers towards decarbonization, among others, the electric vehicle aftermarket solutions are likely to witness a considerable increase in their demand during the review period.

Market Segmentation:

Segmentation 1: by Vehicle Type

• Passenger Vehicles

• Commercial Vehicles

Among the vehicle types, the passenger vehicles segment is expected to dominate the vehicle type segment in the global electric vehicle aftermarket by 2032. This prominence can be attributed to the rising adoption of passenger electric vehicles in both developing and developed economies. The upward trajectory is underpinned by the convergence of more rigorous emission regulations and the reinforcement of governmental initiatives, including subsidies, culminating in augmented demand for passenger EVs in recent times.

Segmentation 2: by Propulsion Type

• Battery Electric Vehicles (BEVs)

• Plug-In Hybrid Electric Vehicles (PHEVs)

• Hybrid Electric Vehicles (HEVs)

Battery electric vehicles (BEVs), hybrid electric vehicles (HEVs), and plug-in hybrid electric vehicles (PHEVs) are the major propulsion types that are served by the global electric vehicle aftermarket. While BEV models have garnered significant traction in the market for a considerable period, concerns surrounding range anxiety and higher upfront costs have encouraged customers to opt for HEVs over BEVs. HEVs exhibit lower emission levels in comparison to traditional gasoline and diesel vehicles. As the prevalence of HEVs continues to grow, it becomes essential for the aftermarket participants to cater to the growing demand for spare parts for HEVs along with their parc size.

Segmentation 3: by Sales Outlet

• Authorized Service Centers

• Premium Multi-brand Service Centers

• Others

Among the various sales outlets, the authorized service centers (OEMs) segment occupied the largest market share in 2022. These centers are staffed by highly trained technicians possessing expert knowledge in electric vehicle technology.

Segmentation 4: by Mode of Sales

• Offline sales

• Online sales

Among the mode of sales, the offline sales segment is expected to dominate the market throughout the forecast period 2023-2032.

Segmentation 5: by Part

• Batteries

• Tires and Wheels

• Brakes and Suspensions

• Body Parts

• Others

The tires and wheels segment is expected to generate the majority of revenue throughout the forecast period. Vehicle electrification will positively influence the demand for tire and wheel replacements in the coming years. It can be ascribed to the increased overall weight of the vehicle, leading to a higher wear rate for this part category.

Segmentation 6: by Region

• North America

• Europe

• U.K.

• China

• Asia-Pacific and Japan

• Rest-of-the-World

Asia-Pacific and Japan dominated the electric vehicle aftermarket in 2022. It can be ascribed to the abundance of HEV parc in Japan. The region is also likely to witness substantial growth in coming years owing to the rising adoption of EVs in other Asian countries. However, it is China that is expected to register the fastest growth during the forecast period as compared to other regions covered within the scope of this report, owing to evolving consumer preferences favoring EVs, rising environmental awareness, access to essential raw materials, robust economic growth, and cost-effective labor force. These pivotal factors collectively contribute to the robust growth of its domestic electric vehicle ecosystem, thereby paving the way for a thriving aftermarket demand in the forthcoming years.

Recent Developments in the Electric Vehicle Aftermarket

• In April 2023, Robert Bosch GmbH launched the “Ultra White bulb range.” The enhanced color temperature would now be available across a range of headlight types, spanning from 4,200 to 4,800 kelvin, delivering a more vibrant and brilliant light output. These ‘Ultra White’ bulbs offer a remarkable 40 percent increase in luminosity compared to standard halogen bulbs.

• In June 2022, Schaeffler AG launched a new four-in-one electric axle for e-mobility. The product offers increased comfort and range owing to innovative thermal management and enhances performance through the interaction of an electric motor, thermal management, power electronics, and transmission in one complete system.

• In January 2022, Continental AG achieved a significant milestone by becoming the inaugural tire manufacturer to showcase its esteemed brands, namely, Continental, Uniroyal, Semperit, Barum, General Tire, Viking, Gislaved, Mabor, and Matador, within the newly introduced tire product category in the TecDoc Catalogue. This advancement allows users to conveniently explore a comprehensive range of summer, winter, and all-season tires specifically tailored to their vehicles, accessible through size specifications or by conducting a vehicle search.

• In September 2021, ZF Friedrichshafen AG unveiled the TRW Electric Brake Booster, a cutting-edge brake technology specifically engineered for electric vehicles. This innovative system utilizes advanced electronic components to enhance brake actuation, offering superior performance and responsiveness. The introduction of the TRW Electric Brake Booster underscores ZF's commitment to delivering tailored solutions that cater to the unique requirements of electric vehicles, further solidifying its position as a leader in the aftermarket industry.

• In April 2021, Michelin launched the new " MICHELIN X Incity EV Z" tires. It’s the first range of tires offered by the company for electric buses, which can also be used for traditional suburban and urban vehicles.

Demand - Drivers and Limitations

Following are the demand drivers for the electric vehicle aftermarket:

• Rising Popularity of Electric Vehicles

• Proliferating Consumer Demand for Electric Vehicle Customization

• Increasing Popularity of Electric Vehicle Second-Life Applications

Following are the limitations of the electric vehicle aftermarket:

• Lack of Electric Vehicle Aftermarket Infrastructure and Awareness

• Cost and Availability Issues of Electric Vehicle Spare Parts

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst, BIS Research, “The electric vehicle aftermarket is growing considerably and is expected to grow relatively faster over the coming years during the forecast period. Electric vehicle aftermarket solution providers are investing heavily in R&D to develop advanced electric vehicle aftermarket solutions capable of meeting the growing user demands for augmenting the EV’s life and performance. Moreover, these electric vehicle aftermarket solution providers are also focusing on partnerships and collaborations with EV manufacturers in order to enhance their competitive advantage in the market. With the growing adoption of electric vehicles in both developed and developing economies, electric vehicle aftermarket solutions will likely witness a surge in demand over the coming years during the forecast period.”

Focus on Vehicle Type, Propulsion Type, Sales Outlet, Mode of Sales, Part, and Country-Level Analysis - Analysis and Forecast, 2023-2032

The aftermarket industry constitutes the secondary components market within the automotive sector, encompassing activities such as the production, remanufacturing, distribution, retail, and installation of diverse vehicle parts, chemicals, equipment, and accessories subsequent to the initial sale of the automobile by the original equipment manufacturer (OEM) to the end consumer. The scope of electric vehicle aftermarket is confined to replacement parts and accessories. It does not include any replacement on the charging infrastructure end, training, or additional services.

The key business opportunities in the electric vehicle aftermarket include electric vehicle battery repair and replacement, EV component recycling and disposal, training and education on electric vehicle aftermarket, and shifting trends toward e-commerce.

The players in the electric vehicle aftermarket adopt the strategies of product development through research-and-development-related investments and partnerships, and collaborations to maintain and strengthen their market position, helping them retain their present customers while also attracting new ones.

A new entrant can focus on catering to the regional demand for spare parts of EVs. To further increase their influence in the market, the new entrants might look toward partnering with the companies operating in the EV ecosystem in order to understand the market dynamics and cater to the demand of customers in the electric vehicle aftermarket. In addition, emerging companies can focus on investment toward research and development-related activities and product development while also focusing on their sales and distribution networks.

The following are some of the USPs of the report:

• Extensive coverage of the 18 electric vehicle aftermarket solution providers to offer a holistic view of the electric vehicle aftermarket landscape

• Qualitative analysis of changing dynamics of the automotive aftermarket owing to the rising adoption of EVs

• Qualitative and quantitative analysis of electric vehicle aftermarket based on vehicle types, propulsion types, sales outlets, mode of sales, and parts

• Qualitative and quantitative analysis of online sales in the electric vehicle aftermarket

• Competitive benchmarking for different industry participants profiled in the Company Profiles section

• Market ranking for different parts

Electric vehicle aftermarket solution providers, EV part manufacturers, and EV ecosystem stakeholders should buy this report.

The APAC fluids and lubricants market for electric vehicles is projected to reach $2,363.8...

The global electric vehicle bearings market is projected to reach $41,127.0 million by 2031...

Fluids and Lubricants Market for Electric Vehicles accounted for $1,387.7 million in 2021 and...

The global electric vehicle brake pads market is expected to reach $289.2 million by 2026,...