Published Year: 2023

Data Center Liquid Cooling Market - A Global and Regional Analysis: Focus on Product, Application, a

The global data center liquid cooling market was valued at $2.79 billion in 2021, which is...

Introduction of the Global Floating Data Center Market

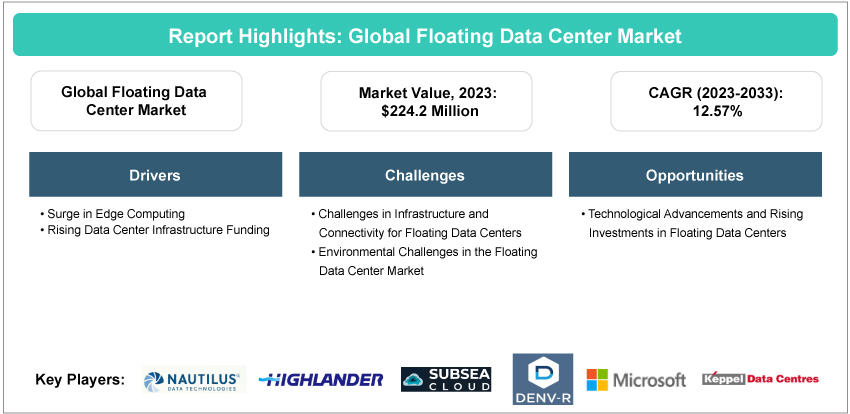

The global floating data center market, valued at $224.2 million in 2023, is expected to reach $732.60 million by 2033, exhibiting a robust CAGR of 12.57% during the forecast period 2023-2033. One of the primary drivers for the growth of the floating data center market is the increasing demand for edge computing. Edge computing involves processing data closer to where it is generated rather than relying on a centralized data-processing warehouse. This surge is particularly evident in the anticipated expansion of edge data center counts by suppliers, which is projected to grow significantly. The increase in edge computing is due to the need for faster processing and lower latency in data handling, particularly for applications such as Internet of Things (IoT) devices, smart cities, and mobile computing.

Introduction to Floating Data Center

The concept of floating data centers has gained significant attention due to its potential to address the growing demand for sustainable and efficient data processing. These innovative facilities are essentially data centers housed on floating platforms, typically located on bodies of water. The demand for floating data centers is expected to increase for several reasons.

Floating data centers present a viable remedy to land scarcity challenges in densely populated urban areas, where conventional data centers often grapple with spatial limitations.

Moreover, leveraging natural water bodies for cooling purposes contributes to heightened energy efficiency, thereby mitigating the environmental footprint associated with data center operations. With the escalating global demand for data storage and processing, the adaptability and eco-friendly characteristics of floating data centers render them an attractive and pragmatic solution for the evolving landscape of data infrastructure.

One of the key advantages of floating data centers is their ability to use the surrounding water for natural cooling, reducing the need for traditional, energy-intensive cooling methods. Their placement on the water allows these data centers to be positioned close to data-intensive operations or in regions where land-based data centers are not feasible. This mobility also aids in reducing latency and improving responsiveness for certain applications. Floating data centers can be designed to be resilient against natural disasters, a significant consideration given the increasing focus on disaster-resistant infrastructure. The integration of technologies such as edge computing in floating data centers is pivotal. This enables real-time data processing, which is essential for applications such as disaster response, environmental monitoring, and autonomous systems.

The expansion of the floating data center market is influenced by a multitude of significant factors. These include the escalating worldwide need for energy-efficient and robust data center cooling solutions, diminishing accessibility of water resources, increasing penetration of the internet, cloud computing, edge computing, and technologies such as AI, IoT, and big data, and the regulatory landscape toward environment-friendly cooling solutions. As a cumulative effect, these factors are projected to drive the increased adoption of underwater and floating data centers over the forecasted period.

Market Segmentation:

Segmentation 1: by Distributed Computing Model

• Cloud Computing

• Edge Computing

Segmentation 2: by Data Center Type

• Underwater Data Center

• Floating Data Center

Segmentation 3: by Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

The North American digital economy is driven by a substantial demand for data storage and processing capabilities. This demand has surged due to the increasing adoption of cloud services, IoT devices, and data-intensive technologies. As per BIS Research analysis, the region is expected to witness a remarkable growth rate, with the number of IoT devices projected to more than double from 3.22 billion in 2023 to 6.24 billion by 2030. Innovative solutions such as floating data centers are being considered to address this escalating demand. BIS Research's analysis suggests that adopting floating data centers could reduce water consumption and energy usage by up to 30%, enhancing operational efficiency and environmental responsibility in the data center industry. However, establishing such infrastructure on bodies of water poses complexities and costs. The emerging floating data center industry in the U.S. is still nascent, but it holds significant disruptive potential. Currently, only a few pilot projects exist, including Nautilus Data Technologies' Stockton1 floating data center in California. With the growing adoption of edge computing, these floating data centers are strategically positioned to support edge infrastructure, particularly in coastal areas with high population density. In 2017, Nautilus Data Technologies secured $36 million in Series C funding, reflecting industry recognition of the growth potential and significance of underwater and floating data center infrastructure. This investment underscores the industry's commitment to innovation in data center solutions.

Recent Developments in the Global Floating Data Center Market

The global data center market has been experiencing significant growth and changes. Here are some recent developments:

Market Growth: The global data center market was expected to register an impressive growth rate of 15.09% across the forecast period from 2023 to 2033.

Regional Developments: According to BIS Research Analysis, Asia-Pacific floating data center market is expected to expand by 12.25% in the forecast period. Furthermore, the surge in edge computing is catalyzing the expansion of the floating data center market, as exemplified by partnerships such as Cellnex and Bouygues Telecom's $1.1 billion investment in constructing water-based data centers to enhance connectivity and introduce 5G infrastructure by 2027.

Innovation: The rapid growth of artificial intelligence, along with other modern technologies, such as streaming, gaming, and self-driving cars, is expected to drive continued strong data center demand.

Demand – Drivers, Challenges, and Opportunities

Market Drivers: Surge in Edge Computing

The growth of the floating data center market is significantly driven by the burgeoning trend of edge computing. Edge computing involves processing data near its source, thereby reducing latency and enhancing overall system performance. Floating data centers strategically positioned near coastal areas and bodies of water emerge as ideal locations for edge computing facilities. This geographical advantage allows for faster data processing and improved responsiveness in service delivery, catering to major population centers and industrial hubs. Scalability is paramount in meeting the diverse and evolving needs of distributed computing, and floating data centers excel in this regard. Their modular and scalable designs align perfectly with the requirements of edge computing, providing adaptable infrastructure solutions. The global floating data center market is poised for substantial growth due to the escalating demand for efficient and sustainable data storage solutions. Businesses generate vast volumes of data, necessitating innovative infrastructure that can address scalability, energy efficiency, and geographical constraints. Floating data centers offer a flexible and environment-friendly approach to data storage, presenting a promising opportunity to meet these demands. Furthermore, various industries, including healthcare, manufacturing, and finance, are increasingly adopting edge computing for specific applications. Customizable floating data centers can be deployed to cater to the unique needs of these industries, further propelling market growth.

Market Challenges: Challenges in Infrastructure and Connectivity for Floating Data Centers

Connectivity challenges in floating data centers include increased latency due to the physical distance from onshore data centers, impacting real-time applications. Submarine cables, the primary means of connectivity, face vulnerabilities such as natural disasters and intentional damage. Maintenance issues involve saltwater corrosion affecting structural and electronic components, as observed in offshore structures. Additionally, extreme weather events, which are on the rise, pose threats to the operations of floating data centers.

As reported by Fox Weather and the National Institutes of Health, extreme weather events in the Gulf of Mexico disrupted the operations of a floating data center, causing downtime and highlighting the importance of designing resilient infrastructure for such conditions. This incident underscores the need for proactive maintenance and connectivity solutions to address the challenges faced by floating data centers.

Market Opportunities: Technological Advancements and Rising Investments in Floating Data Centers

In recent years, companies have recognized the transformative potential of floating data centers as a sustainable and efficient solution for data infrastructure. Notable players such as Nautilus Data Technologies, Inc. made substantial investments, with a $110 million commitment in 2020, demonstrating its confidence in this innovative approach. This trend not only addresses environmental concerns but also positions these companies as leaders in a growing market. With global data demands on the rise, investing in floating data centers is both a technological innovation and a lucrative business opportunity, combining profitability with environmental responsibility. Furthermore, sustainability is increasingly prioritized in corporate operations, aligning with corporate social responsibility goals. Floating data centers, with their renewable energy integration and reduced environmental impact, resonate with environmentally conscious clients, enhancing brand image. Their energy efficiency, driven by advanced cooling technologies, offers long-term cost savings. Additionally, geographic flexibility and disaster resilience give companies a competitive edge, effectively addressing regional data needs while mitigating risks associated with natural disasters.

Analyst’s Thoughts

According to Debraj Chakraborty, Principal Analyst at BIS Research,” The market exhibits promising growth, driven by rising demand for sustainable and scalable data infrastructure. Notable investments by companies such as Nautilus Data Technologies reflect confidence in this innovative approach. Edge computing integration enhances real-time processing for critical applications, such as disaster response, and presents a unique blend of profitability and environmental responsibility, appealing to sustainability-focused businesses.”

A floating data center is a specialized type of data center that is designed to operate on water, typically on the surface of oceans, lakes, or other bodies of water. These data centers are housed within modular, water-tight structures that can be deployed and anchored in water bodies. They utilize water for cooling systems and may integrate renewable energy sources such as tidal or wave power. Floating data centers are known for their mobility and adaptability, enabling them to be strategically positioned near coastal areas to reduce data transmission latency and serve as ideal locations for edge computing facilities. They offer unique advantages such as environmental sustainability, disaster resilience, and scalability.

The report has considered several drivers for the growth of floating and underwater data centers, such as:

1. Surge in Edge Computing

2. Rising Data Center Infrastructure Funding

New companies entering the floating data center market can gain a competitive edge by focusing on several key areas:

• Environmental Sustainability: Prioritize eco-friendly designs and renewable energy sources to align with the growing demand for sustainable data solutions.

• Edge Computing Integration: Emphasize real-time data processing capabilities, catering to applications requiring low latency and rapid decision-making.

• Resilience and Disaster Preparedness: Develop robust infrastructure to withstand extreme weather events and natural disasters, ensuring uninterrupted operations.

• Modularity and Scalability: Design floating data centers with modular components, enabling easy scalability to meet evolving data demands.

• Security and Compliance: Implement stringent security measures and comply with data privacy regulations to instill trust in clients.

• Cost-Efficiency: Leverage advanced cooling technologies for energy efficiency, resulting in long-term operational cost savings.

• Global Market Expansion: Explore strategic positioning to serve diverse markets, addressing regional data needs effectively.

• Partnerships and Alliances: Collaborate with industry partners to enhance connectivity, network reliability, and service offerings.

The USP of the floating data center market report lies in its comprehensive coverage of drivers, restraints, and challenges, industry trends, case studies, key start-ups, funding analysis, product and application segmentation, patent insights, architectural/technical comparison of key products, and country-specific market statistics with forecasts until 2033. This data and insights enable stakeholders to make informed decisions, identify emerging trends, and strategize effectively for market growth and competitive advantage.

1. Floating Barge Manufacturers

2. Investors and Venture Capitalists

3. HVAC Contractors and Service Providers

4. Government and Regulatory Bodies

5. Research Institutions

6. Data Center Cooling Systems Providers

7. Data Center Operators

8. Consulting and Market Research Firms

Some of the market challenges include:

1. Challenges in Infrastructure and Connectivity for Floating Data Centers

2. Environmental Challenges in the Floating Data Center Market

Some of the business opportunities within the market include:

1. Technological Advancements and Rising Investments in Floating Data Centers

The global floating data center market was valued at $29.56 million in 2022 and is projected to grow at a CAGR of about 12.57% to reach $732.60 million by 2033.

North America and Europe are expected to lead the global floating data center market during the forecast period. Their strong technological infrastructure is expected to drive innovation and adoption, cementing their dominant positions in the industry.

The global data center liquid cooling market was valued at $2.79 billion in 2021, which is...

The global data center cooling market accounted for $17.82 billion in 2021 and is expected to...