Published Year: 2024

Middle East and Africa Commercial Vehicles Market: Focus on End Use, Vehicle Type, Propulsion Type,

The Middle East and Africa commercial vehicles market is projected to reach $93,258.3 million...

Focus on Application, Propulsion, Vehicle Type, Level of Autonomy, Sensor Type, and Region - Analysis and Forecast, 2024-2033

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

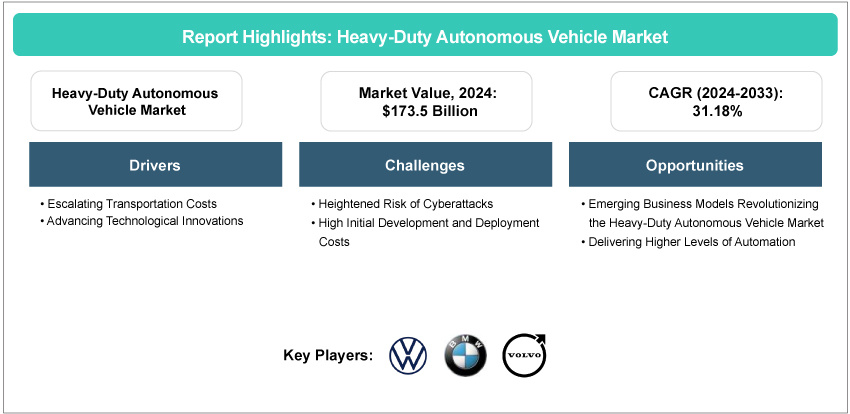

The heavy-duty autonomous vehicle (HDAV) market has been experiencing rapid growth, driven by increased automation in logistics, mining, and construction. The market size in 2024 was estimated at $173.5 billion and is projected to reach $1.99 trillion by 2033, with a CAGR of 31.18% under a realistic scenario. Key factors fueling this expansion include advancements in AI, robotics, and IoT, alongside the growing need for efficient, cost-effective, and sustainable transport solutions. Autonomous trucks are optimizing freight operations, reducing fuel consumption, and addressing driver shortages. Governments are also implementing regulatory frameworks and incentives to promote autonomous technology adoption, further accelerating the market's evolution.

Introduction of Heavy-Duty Autonomous Vehicle

The heavy-duty autonomous vehicle (HDAV) market is driven by advancements in artificial intelligence (AI), machine learning, and automation, enabling these vehicles to operate with minimal human intervention. These vehicles are integrated with sensors, IoT devices, and predictive analytics, enhancing safety, reducing operational costs, and improving efficiency across industries such as logistics, public transportation, construction, and agriculture. The market is segmented into semi-autonomous (SAE Level 1-2) and fully autonomous (SAE Level 3-5) vehicles, with growth being propelled by increasing demand for automation, environmental sustainability, and technological innovation.

Market Introduction

The heavy-duty autonomous vehicle market has been witnessing significant growth due to advancements in automation, artificial intelligence, and connectivity technologies. The market is currently driven by increasing demand for efficiency in logistics, public transportation, and industrial applications. Companies are investing heavily in R&D to enhance vehicle safety, autonomy, and operational cost efficiency. Over the forecast period (2024-2033), the market is expected to expand rapidly, propelled by regulatory support, increased adoption of electric and hybrid autonomous vehicles, and integration of advanced sensor technologies. However, challenges such as high initial investment costs and cybersecurity risks may impact growth. Despite these hurdles, the industry is set to revolutionize transportation, with autonomous trucks, buses, and industrial vehicles becoming more mainstream.

Industrial Impact

The industrial impact of heavy-duty autonomous vehicles (HDAVs) is profound, particularly in logistics, mining, and construction. These vehicles enhance operational efficiency by reducing labor dependency, mitigating driver shortages, and ensuring continuous, 24/7 operations. Autonomous mining trucks from companies such as Caterpillar and Komatsu have significantly improved safety, cost-efficiency, and productivity, with Caterpillar reporting a 30% increase in productivity. The logistics sector benefits from fuel-efficient driving algorithms, reducing operational costs by up to 5% while lowering carbon emissions. Additionally, regulatory advancements, such as Level 4 autonomy approvals in the EU and proactive testing in China, have accelerated industry adoption. However, challenges such as high initial costs, cybersecurity risks, and infrastructure limitations remain barriers to full-scale implementation.

Market Segmentation

Segmentation 1: by Application

• Logistics

• Public Transportation

• Construction and Mining

• Others

Logistics Segment to Dominate the Heavy-Duty Autonomous Vehicle Market (by Application)

The logistics sector is the dominant application for heavy-duty autonomous vehicles. The rising demand for efficiency, cost reduction, and 24/7 operations in supply chains has accelerated the adoption of autonomous trucks. These vehicles significantly lower freight costs, enhance route planning and improve overall delivery times. Additionally, the growth of e-commerce has fueled the need for scalable and cost-effective transportation solutions.

Segmentation 2: Global Conventional Heavy-Duty Vehicle Market (by Application)

• Construction and Mining

• Public Transport

• Agriculture

• Freight And Logistics

• Others

Segmentation 3: by Propulsion Type

• Internal Combustion Engine (ICE) Vehicles

• Electric Vehicles (EVs)

o Battery Electric Vehicle (BEV)

o Plug-in Hybrid Electric Vehicle (PHEV)

o Hybrid Electric Vehicle (HEV)

Internal Combustion Engine (ICE) Vehicles to Dominate the Heavy-Duty Autonomous Vehicle Market (by Propulsion Type)

Despite the global shift toward electrification, internal combustion engine (ICE) vehicles remain the dominant propulsion type in the heavy-duty autonomous vehicle market. The well-established refueling infrastructure, superior range, and high payload capacity make ICE-powered autonomous trucks the preferred choice for long-haul transportation and industries such as mining and construction. However, manufacturers are introducing hybrid models and fuel-efficient technologies to comply with strict emission regulations.

Segmentation 4: by Vehicle Type

• Heavy Trucks

• Heavy Buses

• Robo Shuttles

Heavy Trucks to Dominate the Heavy-Duty Autonomous Vehicle Market (by Vehicle Type)

Among vehicle types, heavy trucks lead the market due to their widespread use in logistics, mining, and industrial applications. The shift toward automation in trucking addresses challenges such as labor shortages, high operational costs, and safety concerns. Autonomous heavy trucks operate continuously without breaks, reducing fuel consumption and increasing delivery efficiency. Companies such as Waymo, TuSimple, and Daimler Truck AG are at the forefront of autonomous heavy truck deployment.

Segmentation 5: by Level of Autonomy

• Semi-Autonomous Vehicles

• Autonomous Vehicles

Semi-Autonomous Vehicles to Dominate the Heavy-Duty Autonomous Vehicle Market (by Level of Autonomy)

Semi-autonomous heavy-duty vehicles (SAE Level 1 and 2) are currently leading the market. To enhance safety and efficiency, these vehicles integrate advanced driver assistance systems (ADAS), including lane-keeping, adaptive cruise control, and emergency braking. The gradual transition to full autonomy is driven by regulatory challenges, infrastructure limitations, and public trust concerns. However, semi-autonomous trucks serve as a bridge to fully autonomous fleets, improving productivity while maintaining human oversight.

Segmentation 6: by Sensor Type

• LiDAR

• RADAR

• Camera

• Others

LiDAR to Dominate the Heavy-Duty Autonomous Vehicle Market (by Sensor Type)

Light detection and ranging (LiDAR) technology is the leading sensor type in autonomous heavy-duty vehicles. Its high accuracy in depth perception, object detection, and environmental mapping makes it critical for safe autonomous operation. LiDAR sensors enable vehicles to navigate complex traffic conditions, detect obstacles in real-time, and operate in low-visibility environments. Major industry players, including Mobileye and Waymo, are investing heavily in LiDAR-based perception systems.

Segmentation 7: Global Conventional Heavy-Duty Vehicle Market (by Vehicle Type)

• Heavy Trucks

• Heavy Buses

Segmentation 8: by Region

• North America (U.S., Canada, Mexico)

• Europe (Germany, France, U.K., Italy, Rest-of-Europe)

• Asia-Pacific (China, Japan, India, South Korea, Rest-of-Asia-Pacific)

• Rest-of-the-World (RoW)

North America to Dominate the Heavy-Duty Autonomous Vehicle Market (by Region)

North America is the leading region in the heavy-duty autonomous vehicle market, driven by strong technological advancements, regulatory support, and major industry players. The U.S. is in charge of companies such as Tesla, Waymo, TuSimple, and Daimler Truck AG, which are investing heavily in autonomous trucking, logistics automation, and AI-driven fleet management. The region's well-established highway infrastructure and growing demand for freight efficiency have accelerated the deployment of self-driving trucks, particularly in long-haul logistics. Additionally, favorable government policies, including regulatory approvals for autonomous vehicle testing and commercial operations, have positioned North America at the forefront of market growth. As adoption increases, the region is expected to drive further innovation and large-scale commercialization of autonomous heavy-duty vehicles.

Recent Developments in the Heavy-Duty Autonomous Vehicle Market

• Aurora Innovation announced plans to operate driverless semi-trucks between Dallas and Houston by the end of 2024. This initiative addresses driver shortages, improves transportation efficiency, and reduces delivery times.

• In July 2024, Vayu Robotics introduced Vayu One, an AI-powered, self-driving delivery vehicle capable of navigating without pre-mapping. The six-foot-long robot can travel at 20 miles per hour and carry up to 100 pounds, offering a scalable and cost-effective solution for goods transport.

• In July 2024, AB Volvo unveiled a new fleet of autonomous loaders and articulated haulers designed for complex construction tasks. These vehicles feature advanced operational control systems, adapting to varied terrain and weather conditions.

• In September 2024, Caterpillar launched its next-gen autonomous drill rigs with enhanced data analytics capabilities. The rigs are designed to optimize mining operations by reducing material waste and improving drilling precision.

• In January 2024, Waymo completed autonomous trials of its Freightliner Cascadia trucks, covering over 700 miles between California and Nevada with no human intervention. The trials demonstrated the efficiency and reliability of autonomous trucking in long-haul freight.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Escalating Transportation Costs

The rising costs associated with transportation are becoming a critical driver for the adoption of heavy-duty autonomous vehicles. Key contributors to escalating transportation costs include increasing fuel prices, labor shortages leading to higher wages for drivers, maintenance expenses for aging fleets, and the impact of stringent regulatory requirements. These factors are pushing industries to seek more efficient and cost-effective solutions, positioning autonomous vehicles as a viable alternative.

Fuel prices, a major cost component in transportation, have been volatile, with global events such as geopolitical tensions and supply chain disruptions driving spikes in fuel costs. Autonomous vehicles can help optimize fuel efficiency through advanced algorithms that ensure optimal driving patterns, significantly reducing fuel consumption. For instance, autonomous trucks developed by Inceptio Technology have demonstrated fuel savings of 3-5% compared to traditional vehicles through their fuel-efficient driving algorithms.

Market Challenges: Heightened Risk of Cyberattacks

The growing reliance on advanced technology and connectivity in heavy-duty autonomous vehicles introduces a significant vulnerability to cyberattacks, posing a critical market restraint. Autonomous vehicles operate using sophisticated networks of sensors, software systems, and vehicle-to-everything (V2X) communication, all of which are potential targets for malicious actors. These attacks compromise operational efficiency and raise serious concerns about safety, privacy, and public trust in autonomous technology. One of the most pressing risks is the potential for hackers to take control of vehicle operations through system breaches. This could lead to dangerous scenarios, such as unauthorized control over braking, steering, or acceleration, endangering lives and disrupting supply chains.

Market Opportunities: Delivering Higher Levels of Automation

The drive to achieve higher levels of automation presents a significant opportunity in the heavy-duty autonomous vehicle market. As industries such as logistics, construction, mining, and public transportation seek to optimize operations, autonomous vehicles capable of advanced automation are emerging as transformative solutions. Higher levels of automation, particularly Levels 4 and 5, reduce the reliance on human intervention, enabling vehicles to operate efficiently, safely, and continuously in various environments.

In the logistics sector, the adoption of higher automation levels addresses critical challenges, including rising transportation costs and driver shortages. Fully automated trucks can operate around the clock without the need for rest breaks, maximizing fleet utilization and improving delivery times. For instance, companies such as Waymo and TuSimple have been piloting Level 4 autonomous trucking solutions that handle long-haul routes with minimal human input. These advancements enhance operational efficiency and significantly lower costs by reducing driver-related expenses and optimizing fuel consumption through intelligent driving systems.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, "The heavy-duty autonomous vehicle market has been experiencing rapid transformation, driven by advancements in AI, sensor technology, and regulatory support across major regions. North America leads the market, with strong investments from companies such as Tesla, Waymo, and Daimler Truck AG, while Asia-Pacific is the fastest-growing region, fueled by China and Japan’s push for autonomous logistics solutions. The logistics sector dominates as fleet operators seek cost reduction, operational efficiency, and 24/7 transport capabilities. While internal combustion engine (ICE) vehicles still lead, the shift toward electric and hybrid models is accelerating, driven by sustainability mandates and emission regulations. Challenges such as high initial deployment costs, cybersecurity risks, and infrastructure limitations remain, but ongoing technological innovations and pilot programs indicate a promising future for fully autonomous heavy-duty transportation."

Focus on Application, Propulsion, Vehicle Type, Level of Autonomy, Sensor Type, and Region - Analysis and Forecast, 2024-2033

The heavy-duty autonomous vehicle (HDAV) market offers the integration of automation, AI-driven navigation, and real-time data analytics into large commercial vehicles such as trucks, buses, and industrial transporters. These vehicles use advanced driver assistance systems (ADAS), LiDAR, radar, and machine learning algorithms to operate with minimal or no human intervention. The market is driven by logistics automation, increased safety measures, rising fuel efficiency demands, and advancements in smart mobility infrastructure.

The HDAV market offers several business opportunities, including:

• AI-Driven Logistics: Development of autonomous freight transport and smart route optimization solutions to enhance supply chain efficiency

• Electric and Hybrid Heavy Vehicles: Expansion in battery-electric and hydrogen-powered heavy-duty autonomous trucks for sustainable transport

• Fleet Management Systems: Investment in cloud-based, AI-driven fleet monitoring solutions for real-time vehicle tracking and predictive maintenance

• Autonomous Public Transport: Deployment of self-driving buses and shuttles in urban areas to reduce congestion and improve mobility

• Mining and Industrial Automation: Adoption of autonomous heavy machinery for safer and more cost-effective operations in mining and construction

• Cybersecurity and Data Protection: Development of secure autonomous vehicle communication protocols to prevent cyber threats

Leading companies in the HDAV market have been implementing various strategies, including:

• Mergers and Acquisitions: Companies such as Daimler Truck AG, Volvo, and Waymo are acquiring AI and autonomous technology firms to enhance their capabilities.

• Strategic Partnerships: Collaborations between automakers, AI developers, and logistics firms are accelerating the deployment of self-driving trucks.

• Product Innovation and Development: The companies have been investing in Level 4 and Level 5 autonomous technology, including improved sensor fusion and AI-powered navigation.

• Regional Expansion: Companies are entering emerging markets in Asia-Pacific and the Middle East to capitalize on the growing demand for autonomous freight transport.

• Sustainability Initiatives: Companies are adopting hydrogen and electric autonomous trucks to comply with strict emissions regulations.

A new entrant in the HDAV market should prioritize:

• AI-based route optimization for autonomous logistics and freight transport

• Advanced LiDAR, RADAR, and sensor fusion technology for enhanced vehicle perception

• Cybersecurity solutions to safeguard autonomous vehicle networks from hacking threats

• Electric and hydrogen-powered heavy-duty autonomous trucks for zero-emission transport

• Fleet management platforms integrating real-time monitoring, predictive maintenance, and fuel optimization

• Autonomous public transport solutions, including self-driving buses and shuttle services

The unique selling proposition (USP) of this report lies in its comprehensive market intelligence, offering:

• In-depth analysis of emerging autonomous vehicle technologies, including AI-powered navigation and sensor advancements

• Key market trends and business drivers, enabling companies to identify growth opportunities and expansion strategies

• Detailed segmentation by application, propulsion type, level of autonomy, sensor type, and region, ensuring targeted market insights

• Competitive benchmarking and company profiles, providing insights into leading players and disruptive innovations in the HDAV market

• Regulatory and safety compliance coverage, ensuring alignment with global autonomous vehicle policies, sustainability goals, and cybersecurity standards

This report is essential for a wide range of stakeholders, including:

• Automotive and Commercial Vehicle Manufacturers: To develop and deploy autonomous heavy-duty trucks and buses

• Logistics and Freight Companies: To leverage autonomous trucking solutions for cost-efficient and sustainable freight transport

• Technology Providers: To innovate LiDAR, AI-based navigation, cybersecurity, and V2X communication solutions

• Government and Regulatory Agencies: To develop policies for autonomous vehicle integration, safety standards, and sustainability initiatives

• Investors and Venture Capitalists: To identify high-growth segments in the autonomous trucking and logistics space

• Infrastructure Developers: To support the expansion of smart roads, charging stations, and vehicle-to-infrastructure (V2I) communication

The Middle East and Africa commercial vehicles market is projected to reach $93,258.3 million...

The autonomous vehicle market is anticipated to grow at a CAGR of 20.78% during the forecast...