Figure 1: Global Next-Generation Ultrasound Systems Market (by Development and Strategies), January 2017-March 2021

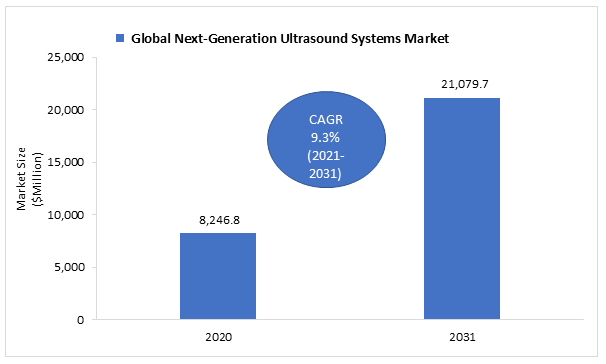

Figure 2: Global Next-Generation Ultrasound Systems Market, 2020-2031

Figure 3: Leading Players in the Global Next-Generation Ultrasound Systems Market, 2020

Figure 4: Next-Generation Ultrasound Systems Market Share (by Product Type), 2020

Figure 5: Growth Share Matrix (by Application), 2020-2031

Figure 6: Growth Share Matrix (by Portability), 2020-2031

Figure 7: Growth Share Matrix (by Technology), 2020-2031

Figure 8: Growth Share Matrix (by Region), 2020-2031

Figure 3.1: Research Methodology

Figure 3.2: Primary Research

Figure 3.3: Secondary Research

Figure 3.4: Data Triangulation

Figure 3.5: Bottom-Up Approach

Figure 4.1: Global Next-Generation Ultrasound Systems Market (by Development and Strategies), January 2017-March 2021

Figure 4.2: Global Next-Generation Ultrasound Systems Market; Key Partnerships, Alliances, and Business Expansion Activities (by Company), 2017-2020

Figure 4.3: Global Next-Generation Ultrasound Systems Market; Key Regulatory and Legal Activities, 2017-2021

Figure 4.4: Global Next-Generation Ultrasound Systems Market; Key New Offerings, 2017-2021

Figure 4.5: Some of the Leading Players in the Global Next-Generation Ultrasound Systems Market, 2020

Figure 4.6: Global Next-Generation Ultrasound Systems Market Share (by Technology), 2020

Figure 4.7: Global Next-Generation Ultrasound Systems Market Share (by Product Type), 2020

Figure 4.8: Global Next-Generation Ultrasound Systems Market Share (by Application), 2020

Figure 4.9: Global Next-Generation Ultrasound Systems Market Share (by Portability), 2020

Figure 4.10: Global Next-Generation Ultrasound Systems Market Share (by End User), 2020

Figure 4.11: Global Next-Generation Ultrasound Systems Market Share (by Region), 2020

Figure 4.12: Growth Share Matrix (by Technology), 2020-2031

Figure 4.13: Growth Share Matrix (by Product Type), 2020-2031

Figure 4.14: Growth Share Matrix (by Application), 2020-2031

Figure 4.15: Growth Share Matrix (by Portability), 2020-2031

Figure 4.16: Growth Share Matrix (by End User), 2020-2031

Figure 4.17: Growth Share Matrix (by Region), 2020-2031

Figure 5.1: Regulatory Process for Medical Devices in the U.S.

Figure 5.2: MDR Transitional Provisions (EU)

Figure 5.3: Regulatory Process for Medical Devices in the China

Figure 5.4: Regulatory Process for Medical Devices in Japan

Figure 5.5: U.S. Reimbursement System

Figure 5.6: Germany Reimbursement System

Figure 5.7: France Reimbursement System

Figure 5.8: U.K. Reimbursement System

Figure 6.1: Market Dynamics

Figure 7.1: Global Next-Generation Ultrasound Systems Market (by Technology)

Figure 7.2: Global Next-Generation Ultrasound Systems Market Share (by Technology), 2020 and 2031

Figure 7.3: Global Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 7.4: Global 4D/3D Ultrasound Systems Market, $Million, 2020-2031

Figure 7.5: Global 2D Ultrasound Systems Market, $Million, 2020-2031

Figure 7.6: Global Others (Fusion Imaging, Tissue Harmonic Imaging) Market, $Million, 2020-2031

Figure 8.1: Global Next-Generation Ultrasound Systems Market (by Product Type)

Figure 8.2: Global Next-Generation Ultrasound Systems Market Share (by Product Type), $Million, 2020 and 2031

Figure 8.3: Global Next-Generation Ultrasound Systems Market (Diagnostic Ultrasound Systems), $Million, 2020-2031

Figure 8.4: Global Next-Generation Ultrasound Systems Market (Therapeutic Ultrasound Systems), $Million, 2020-2031

Figure 9.1: Global Next-Generation Ultrasound Systems Market (by Portability)

Figure 9.2: Global Next-Generation Ultrasound Systems Market Share (by Portability), $Million, 2020 and 2031

Figure 9.3: Global Next-Generation Ultrasound Systems Market (Cart/Trolley-Based Systems), $Million, 2020-2031

Figure 9.4: Global Next-Generation Ultrasound Systems Market (Handheld Devices and Wearables), $Million, 2020-2031

Figure 9.5: Global Next-Generation Ultrasound Systems Market (Portable Systems), $Million, 2020-2031

Figure 10.1: Revenue Contribution of Different Applications, $Million, 2020 and 2031

Figure 10.2: Global Next-Generation Ultrasound Systems Market (General Imaging), $Million, 2020-2031

Figure 10.3: Global Next-Generation Ultrasound Systems Market (Cardiovascular Imaging), $Million, 2020-2031

Figure 10.4: Global Next-Generation Ultrasound Systems Market (Vascular Imaging), $Million, 2020-2031

Figure 10.5: Global Next-Generation Ultrasound Systems Market (Obstetrics and Gynecology Imaging), $Million, 2020-2031

Figure 10.6: Global Next-Generation Ultrasound Systems Market (Lung Imaging), $Million, 2020-2031

Figure 10.7: Global Next-Generation Ultrasound Systems Market (Urology Imaging), $Million, 2020-2031

Figure 10.8: Global Next-Generation Ultrasound Systems Market (Orthopedics/Musculoskeletal Imaging), $Million, 2020-2031

Figure 10.9: Global Next-Generation Ultrasound Systems Market (Other Imaging), $Million, 2020-2031

Figure 11.1: Global Next-Generation Ultrasound Systems Market (by End User)

Figure 11.2: Global Next-Generation Ultrasound Systems Market Share (by End User), $Million, 2020 and 2031

Figure 11.3: Global Next-Generation Ultrasound Systems Market (Hospitals), $Million, 2020-2031

Figure 11.4: Global Next-Generation Ultrasound Systems Market (Diagnostic Centers), $Million, 2020-2031

Figure 11.5: Global Next-Generation Ultrasound Systems Market (Ambulatory Surgical Centers) $Million, 2020-2031

Figure 11.6 : Global Next-Generation Ultrasound Systems Market (Others) $Million, 2020-2031

Figure 12.1: Global Next-Generation Ultrasound Systems Market (by Region), $Million, 2020 and 2031

Figure 12.2: North America: Incremental Revenue Opportunity (by Technology), 2020-2031

Figure 12.3: North America Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.4: North America Next-Generation Ultrasound Systems Market (by Technology) $Million, 2020-2031

Figure 12.5: North America Next-Generation Ultrasound Systems Market (by Product Type), $Million, 2020-2031

Figure 12.6: North America Next-Generation Ultrasound Systems Market (by Application), $Million, 2020-2031

Figure 12.7: North America Next-Generation Ultrasound Systems Market (by End User), $Million, 2020-2031

Figure 12.8: North America Next-Generation Ultrasound Systems Market (by Portability), $Million, 2020-2031

Figure 12.9: North America Next-Generation Ultrasound Systems Market (by Country), $Million, 2020-2031

Figure 12.10: U.S. Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.11: Canada Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.12: Europe: Incremental Revenue Opportunity (by Technology), 2020-2031

Figure 12.13: Europe Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.14: Europe Next-Generation Ultrasound Systems Market (by Technology), $Million, 2020-2031

Figure 12.15: Europe Next-Generation Ultrasound Systems Market (by Product Type), $Million, 2020-2031

Figure 12.16: Europe Next-Generation Ultrasound Systems Market (by Application), $Million, 2020-2031

Figure 12.17: Europe Next-Generation Ultrasound Systems Market (by End User), $Million, 2020-2031

Figure 12.18: Europe Next-Generation Ultrasound Systems Market (by Portability), $Million, 2020-2031

Figure 12.19: Europe Next-Generation Ultrasound Systems Market (by Country), $Million, 2020-2031

Figure 12.20: Germany Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.21: U.K. Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.22: France Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.23: Italy Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.24: Spain Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.25: Switzerland Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.26: Sweden Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.27: Rest-of-Europe Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.28: Asia-Pacific Incremental Revenue Opportunity (by Technology), 2020-2031

Figure 12.29: Asia-Pacific Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.30: Asia-Pacific Next-Generation Ultrasound Systems Market (by Technology), $Million, 2020-2031

Figure 12.31: Asia-Pacific Next-Generation Ultrasound Systems Market (by Product Type), $Million, 2020-2031

Figure 12.32: Asia-Pacific Next-Generation Ultrasound Systems Market (by Application), $Million, 2020-2031

Figure 12.33: Asia-Pacific Next-Generation Ultrasound Systems Market (by End User), $Million, 2020-2031

Figure 12.34: Asia-Pacific Next-Generation Ultrasound Systems Market (by Portability), $Million, 2020-2031

Figure 12.35: Asia-Pacific Next-Generation Ultrasound Systems Market (by Country), $Million, 2020-2031

Figure 12.36: Japan Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.37: China Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.38: India Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.39: Australia and New Zealand Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.40: South Korea Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.41: Rest-of-Asia-Pacific Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.42: Latin America Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 12.43: Middle East and Africa Next-Generation Ultrasound Systems Market, $Million, 2020-2031

Figure 13.1: Share of the Companies Profiled (by Ownership Type)

Figure 13.2: Canon, Inc.: Overall Financials, $Million, 2018-2020

Figure 13.3: Canon, Inc.: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.4: Canon, Inc.: Net Revenue (by Region), $Million, 2018-2020

Figure 13.5: Canon, Inc.: R&D Expenditure, $Million, 2018-2020

Figure 13.6: Fujifilm Holdings Corporation: Overall Financials, $Million, 2018-2020

Figure 13.7: Fujifilm Holdings Corporation: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.8: Fujifilm Holdings Corporation: Net Revenue (by Region), $Million, 2018-2020

Figure 13.9: Fujifilm Holdings Corporation: R&D Expenditure, $Million, 2018-2020

Figure 13.10: General Electric Company: Overall Financials, $Million, 2018-2020

Figure 13.11: General Electric Company: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.12: General Electric Company: Net Revenue (by Region), $Million, 2018-2020

Figure 13.13: General Electric Company: R&D Expenditure, $Million, 2018-2020

Figure 13.14: Hitachi, Ltd.: Overall Financials, $Million, 2018-2020

Figure 13.15: Hitachi, Ltd.: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.16: Hitachi, Ltd.: Net Revenue (by Region), $Million, 2018-2020

Figure 13.17: Hitachi, Ltd.: R&D Expenditure, $Million, 2018-2020

Figure 13.18: Hologic, Inc.: Overall Financials, $Million, 2018-2020

Figure 13.19: Hologic, Inc.: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.20: Hologic, Inc.: Net Revenue (by Region), $Million, 2018-2020

Figure 13.21: Hologic, Inc.: R&D Expenditure, $Million, 2018-2020

Figure 13.22: Koninklijke Philips N.V.: Overall Financials, $Million, 2018-2020

Figure 13.23: Koninklijke Philips N.V.: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.24: Koninklijke Philips N.V.: Net Revenue (by Region), $Million, 2018-2020

Figure 13.25: Koninklijke Philips N.V.: R&D Expenditure, $Million, 2018-2020

Figure 13.26: Samsung Electronics Co., Ltd.: Overall Financials, $Million, 2018-2020

Figure 13.27: Samsung Electronics Co., Ltd.: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.28: Samsung Electronics Co., Ltd.: Net Revenue (by Region), $Million, 2018-2020

Figure 13.29: Samsung Electronics Co., Ltd.: R&D Expenditure, $Million, 2018-2020

Figure 13.30: Shimadzu Corporation: Overall Financials, $Million, 2018-2020

Figure 13.31: Shimadzu Corporation: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.32: Shimadzu Corporation: Net Revenue (by Region), $Million, 2018-2020

Figure 13.33: Shimadzu Corporation: R&D Expenditure, $Million, 2018-2020

Figure 13.34: Siemens Healthineers AG: Overall Financials, $Million, 2018-2020

Figure 13.35: Siemens Healthineers AG: Net Revenue (by Segment), $Million, 2018-2020

Figure 13.36: Siemens Healthineers AG: Net Revenue (by Region), $Million, 2018-2020

Figure 13.37: Siemens Healthineers AG: R&D Expenditure, $Million, 2018-2020