Published Year: 2021

Space-Based Broadband Internet Market - A Global and Regional Analysis: Focus on Application, End Us

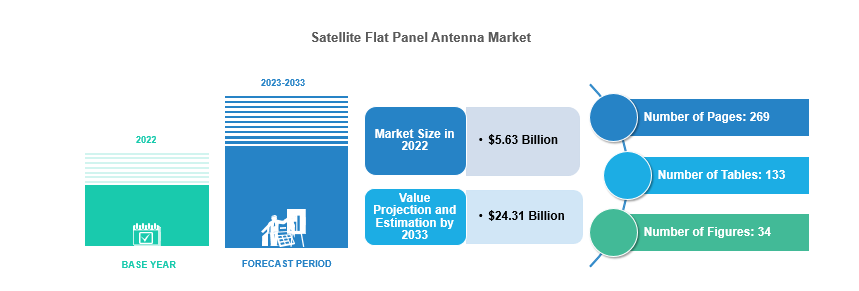

The global space-based broadband internet market is estimated to reach $52,330.8 million in...

Focus on Application, Steering Mechanism, Type, Frequency Band, and Country - Analysis and Forecast, 2023-2033

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights, which are gathered from primary experts.

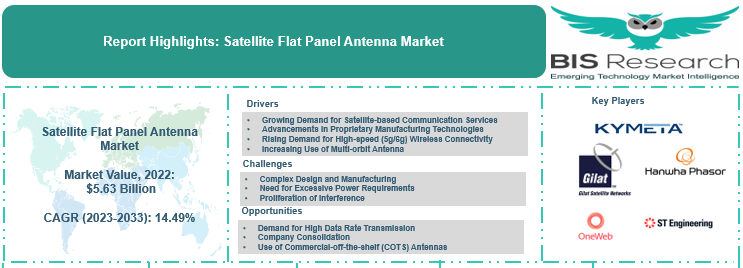

The top solution segment, which is leading, includes satellite flat panel antenna manufacturers that capture around 65% of the presence in the market. Players in other industries, such as satellite operators and telecom operators, account for approximately 20% and 15% of the presence in the market, respectively.

Key Companies Profiled:

Solution Providers

• ALCAN Systems GmbH i.L.

• ALL.SPACE Networks Limited

• Ball Aerospace

• C-COM Satellite Systems Inc

• China Starwin Science & Technology Co., Ltd

• GILAT SATELLITE NETWORKS

• Hanwha Phasor

• Kymeta Corporation

• L3Harris Technologies

• THE MTI CORPORATION

• NXTCOMM

• OneWeb

• ST Engineering

• Starlink

• ThinKom Solutions, Inc.

Satellite Operators

• OQ Technology

• Intelsat

• Avanti Communications Group PLC

• Eutelsat S.A.

• Omnispace, LLC

• OneWeb

• China Satellite Communications Co., Ltd.

Telecom Operators

• Nokia

• ZTE

• China Telecom

• AT&T

• T-Mobile

• Orange

• Jio

• Huawei

Introduction to Global Satellite Flat Panel Antenna Market

A satellite flat panel antenna is a type of directional antenna that focuses its radio signals in a specific direction while providing a wider beam compared to traditional dish antennas. This broader beam enables the antenna to cover a larger area with its signals. It includes a variety of tasks such as receiving and transmitting signals, tracking satellites, facilitating communication, enabling data transfer, ensuring reliable connectivity, and supporting satellite-based services such as television broadcasting and internet access. The global satellite flat panel antenna market is driven by several factors, including the rising demand for high-speed (5G/6G) wireless connectivity, increasing demand for multi-orbit antennas, and advancements in proprietary manufacturing technologies. The application of the global satellite flat panel antenna market is in various fields such as aviation, defense and government, maritime, and telecom. Satellite flat panel antennas enable faster data transmission rates, enhanced network capacity, and reliable and high-speed connectivity in demanding operational scenarios, allowing military personnel to maintain effective communication even in remote and challenging locations.

Market Introduction

Antenna designs have undergone significant evolution and have found applications across diverse fields. Ongoing advancements have enhanced their performance and utility. To ensure efficient evaluation of these designs, effective testing methods are vital. With the rise of Internet of Things (IoT) devices and the emergence of smart cities, flat panel antennas enable seamless connectivity and data exchange among devices, facilitating efficient infrastructure management and enhancing the quality of life.

Currently, the trend toward more compact, scalable lighter, and beamforming antenna demonstrates the industry's commitment to improving performance, efficiency, and flexibility. Electronically steered flat panel antennas play a crucial role in maximizing satellite bandwidth efficiency and addressing weight considerations, particularly for mobility applications. In the coming decade, these antennas are expected to dominate the maritime and land-mobile sectors due to their lightweight design and simplified installation procedures. Meanwhile, mechanically steered antennas currently maintain a competitive edge in the aeronautical industry, benefitting from their early market presence and meeting the stringent performance requirements specific to this sector.

The deployment of satellite mega-constellations and the potential to provide global broadband coverage in remote areas have a positive impact on the global satellite flat panel antenna market. Several organizations, research institutes, and government agencies are working to introduce newer technologies into the global satellite flat panel antenna market.

In recent years, satellite flat panel antenna has registered an exponential surge in demand from the defense and government industry, with high demands for secure communications, surveillance, reconnaissance, and intelligence gathering. Additionally, the global satellite flat panel antenna market is expected to experience significant growth in the coming years, driven by the emergence of satellite mega-constellations deployed by prominent companies such as OneWeb, SpaceX, and Amazon's Project Kuiper. They focus on deploying thousands of satellites into orbit, creating a network that enables global connectivity. For instance, in February 2023, OneWeb and Intelsat successfully completed inflight testing of a hybrid low Earth orbit (LEO) and geostationary (GEO) inflight connectivity solution. The tests were conducted on an Intelsat's Bombardier CRJ-700 regional jet fitted with the new electronically steered array (ESA) antenna, which has been built in collaboration with Stellar Blu and OneWeb. This is the first time LEO and GEO satellite connectivity has been seamlessly switched in flight.

Market Segmentation:

Segmentation 1: by Application

• Automotive

• Aviation

• Defense and Government

• Enterprise

• Maritime

• Telecom

• Oil and Gas

• Space

Defense and Government Application to Continue its Dominance as the Leading Application Segment

The global satellite flat panel antenna market is led by the defense and government industry, with a 25.19% share in 2023. Satellite flat panel antennas find application in military/defense sectors, catering to the needs of reliable connectivity over long distances without signal interruptions or losses. They can be deployed on vehicles, aircraft, and ships, providing real-time data transfer, voice communication, and other critical services for situational awareness, command and control, and coordination between forces.

Satellite flat panel antennas are revolutionizing the broadband connectivity landscape by enabling high-speed internet access of up to 400Mbps through low Earth orbit (LEO) and medium Earth orbit (MEO) satellites. The advancements in satellite technology, coupled with the beamforming capabilities of these antennas, are propelling the demand for flat panel antennae. It is expected that the sales of satellite flat panel antennas will continue the same trend in the coming years and contribute significantly to the growth of the global satellite flat panel antenna market during the forecast period. For instance, in September 2021, the Kymeta Corporation launched the u8 MIL hybrid terminal, a military communications solution incorporating Kymeta's software-defined, electronic beam-steering technology. The terminal is designed to be rugged and has a low-profile form factor, making it easy to mount on various military vehicles and vessels. In addition, it enables reliable and high-speed connectivity in demanding operational scenarios, allowing military personnel to maintain effective communication even in remote and challenging locations.

Segmentation 2: by Steering Mechanism

• Electronically Steered Antenna

• Mechanically Steered Antenna

• Hybrid

Electronically Steered Antenna to witness the highest growth between 2023 and 2033.

The global satellite flat panel antenna market is expected to be dominated by the electronically steered antenna segment in 2023, with a 40.0% share in terms of revenue. Ongoing advancements in technology, such as the integration of advanced semiconductor components, improved power efficiency, and enhanced beamforming, are the factors driving the adoption of electronically steered antennas across various industries.

These antennas are ideal for applications that require high precision and fast response times, such as military communications and weather forecasting. For instance, in March 2023, the Space Development Agency (SDA) of the Pentagon awarded a $5 million contract to CesiumAstro, a manufacturer of advanced aerospace communications systems, to develop L band active electronically steered antennas (AESA) that are compatible with the Link 16 tactical data network, a standardized communication system employed by the U.S., North Atlantic Treaty Organization (NATO), and Coalition forces to facilitate the transmission and exchange of real-time tactical information.

Segmentation 3: by Type

• Flat Panel Antenna for Satellite Communication (Satcom)

• Flat Panel Antenna for Terrestrial Communication

Flat Panel Antenna for Satellite Communication (Satcom) to Witness the Highest Growth between 2023 and 2033

The global satellite flat panel antenna market is expected to be dominated by flat panel antenna for satellite communication (Satcom) in 2023, with a 53.46% share in terms of revenue. The growing demand for high-speed broadband connectivity and reliable communication services is driving the adoption of flat panel antennas in satellite communication.

In the satellite communications industry, most flat panel antennas are waveguide-based, employing either horn or slot array antennas with mechanical steering, printed circuit board (PCB) antennas, or active electronically steered arrays. For instance, C-COM Satellite Systems Inc, a global provider of mobile auto-deploying satellite antenna systems, is directing its efforts toward developing a novel modular and cost-effective Ka band antenna tailored for the next generation of mobile satellite communications. This antenna will be designed to operate within the Ka band frequency range and possess conformal properties.

Segmentation 4: by Frequency Band

• L and S Band (1 GHz – 4 GHz)

• C and X Band (4 GHz – 12 GHz)

• Ku, K, and Ka Band (13 GHz – 40 GHz)

Ku, K, and Ka Band (13 GHz – 40 GHz) to Witness the Highest Growth between 2023 and 2033

The global satellite flat panel antenna market is expected to be dominated by Ku, K, and Ka bands (13 GHz – 40 GHz) in 2023, with a 50.40% share in revenue due to the rising demand for new and advanced high-throughput satellite services.

Advancements in satellite technology, such as the deployment of high-capacity satellites and advanced modulation techniques, have increased the capabilities and efficiency of the Ku, K, and Ka bands. For instance, in March 2022, Intellian Technologies unveiled the manufacturing plan of phased array flat panel antennas designed for Ku and Ka band low Earth orbit (LEO) and medium Earth orbit (MEO) satellite networks. Intellian has developed electronically steered antennas (ESA) to deliver exceptional performance. These antennas leverage Intellian's extensive experience and expertise in advanced antenna design, manufacturing, and reliable connectivity with non-geostationary satellites orbit (NGSO). The ground-breaking design of these antennas incorporates Intellian's leading phased array chipset, structure, and software, seamlessly integrated into a modular system that enables efficient production and worldwide distribution of this innovative ESA technology.

Segmentation 5: by Region

• North America - U.S. and Canada

• Europe - U.K., Germany, France, Russia, and Rest-of-Europe

• Asia-Pacific - Japan, India, China, South Korea, and Rest-of-Asia-Pacific

• Rest-of-the-World - Middle East and Africa and South America

North America was the highest-growing market among all the regions, registering a CAGR of 14.77%. North America is anticipated to gain traction in terms of satellite flat panel antenna production owing to the presence of a large number of satellite flat panel antenna manufacturers such as ThinKom Solutions, Inc., Kymeta Corporation, NXTCOMM, and Starlink (Space X). Moreover, favorable government regulatory policies are also expected to support the growth of the satellite flat panel antenna market in Europe and Asia-Pacific during the forecast period.

In North America, the U.S. is anticipated to show the highest growth in the satellite flat panel antenna market among other countries, such as the U.S. and Canada. U.S. is anticipated to grow at a CAGR of 14.99%. The growth of the U.S. in the satellite flat panel antenna market is mainly due to factors such as the increasing use of satellite technology in defense and military applications and the ability of these antennas to deliver high-speed broadband and satellite internet services to remote areas, among others.

Recent Developments in the Satellite Flat Panel Antenna Market

• In May 2023, Dallas Fort Worth International Airport (DFW) partnered with AT&T to improve connectivity and critical infrastructure through a comprehensive wireless platform (CWP). AT&T plans to invest $10 million in modernizing and expanding the network covering the airport, supporting airport operations, and enhancing the free public Wi-Fi in terminals. Additionally, AT&T would establish a private 5G network for internal use by the airport to address the increasing demand for Internet of Things (IoT) use cases and the digitization of airport operations.

• In April 2023, ALL.SPACE Networks Limited partnered with Kratos Defense & Security Solutions, Inc. to develop advanced terminal solutions for software-defined satellite ground systems. It features a multi-beam antenna.

• In April 2023, OneWeb was selected to conduct two trials for the U.K. government's ‘Very Hard to Reach Premises’ connectivity program. The trials aim to connect the most remote homes and businesses in the U.K. and take place in the Shetland Islands and on Lundy Island. OneWeb's LEO network would deliver high-speed, low-latency connectivity for the trials through its partners BT and Clarus.

• In March 2023, under a contract with Sierra Nevada Corporation (SNC), ThinKom Solutions, Inc. delivered its ThinAir Ka2517 phased array Satcom antenna systems for installation on Sierra Nevada's new RAPCON-X aircraft.

• In March 2023, OneWeb and mu Space signed a multi-year, multi-million-dollar agreement to provide OneWeb's low Earth orbit (LEO) connectivity solutions to mainland Southeast Asia, including Thailand, Laos, Cambodia, Vietnam, and Malaysia.

• In February 2023, GILAT SATELLITE NETWORKS received a multimillion-dollar contract from a leading integrator in the Asia-Pacific region for ER7000 Satcom on-the-move antenna to enable satellite-based internet for passenger trains.

Demand – Drivers and Limitations

Following are the drivers for the satellite flat panel antenna market:

• Growing Demand for Satellite-Based Communication Services

• Advancement in Proprietary Technologies

• Rising Demand for High-Speed (5G/6G) Wireless Connectivity

• Increasing Use of Multi-Orbit Antenna

Following are the challenges for the satellite flat panel antenna market:

• Complex Design and Manufacturing

• Need for Excessive Power Requirements

• Proliferation of Interference

Following are the opportunities for the satellite flat panel antenna market:

• Demand for High Data Rate Transmission

• Company Consolidation

• Use of Commercial Off-The-Shelf (COTS) Components

Analyst’s Thoughts

According to Nilopal Ojha, Principal Analyst, BIS Research, “The deployment of Satcom solutions is on the rise, and affordable Satcom -on-the-move is scaling up across applications. Connected cars in the automotive domain and consumer segment remote connectivity services are areas that are driving the Satcom terminal numbers, especially in the small form factor segments specifically designed for on-the-move and/or deployable use cases. This growing number of smaller Satcom terminals is further driven by the growth of LEO-based connectivity services from participants such as Starlink and OneWeb. All these developments indicate a strong and steady demand for Satcom terminal components, of which small-form-factor antenna solutions play a significant role. The demand for flat panel antennas for Satcom terminals across multiple applications will continue to grow moving forward. This study estimates the demand for the same and discusses the opportunity areas which are yet to materialize.”

Focus on Application, Steering Mechanism, Type, Frequency Band, and Country - Analysis and Forecast, 2023-2033

The global satellite flat panel antenna market refers to a phased array antenna that is made up of many tiny antennas each with a phase shifter that can control the direction of signal emitted. By controlling the phase shift of each antenna, the beam can be steered in any specific direction while providing a wider beam compared to traditional dish antennas. This broader beam enables the antenna to cover a larger area with its signals. Flat panel antennas are utilized in various applications, including military, naval, and commercial aircraft radar systems.

The key trends in the market include the growing need for high-speed data transmission, broadband connectivity, low profile and lightweight design . Many companies such as Kymeta Corporation, OneWeb, Starlink, GILAT SATELLITE NETWORKS, and among others are actively involved in the development of satellite flat panel antenna technologies for various applications. Other technological trends are the use smart and adaptive antennas, emergence of low Earth orbit (LEO) satellite networks, advanced beamforming and phased array technologies.

The global satellite flat panel antenna market has seen major development by key players operating in the market, such as business expansion activities, investments, contracts, partnerships, collaborations, mergers, and agreements. According to BIS Research, the majority of the companies preferred collaborations, contracts, and agreements as strategies to further increase their growth in the global satellite flat panel antenna market. Companies such as ThinKom Solutions, Inc., Ball Aerospace, ALCAN Systems GmbH i.L., C-COM Satellite Systems Inc, OneWeb and Hanwha Phasor have majorly adopted partnership, contract, collaboration, and agreement strategies.

There is an increasing demand for multi-orbit antennas and advancements in proprietary manufacturing technologies. Hence, the new entrants can focus on enhancing the performance, efficiency, and cost-effectiveness of flat panel antenna designs in the global satellite flat panel antenna market and go for the latest manufacturing technologies. In addition, the new entrants should focus on advancements in fifth-generation (5G) and the forthcoming sixth-generation (6G) mobile communication systems.

The following can be seen as some of the USPs of the report:

• A dedicated section focusing on various technologies adopted by the key players operating in the global satellite flat panel antenna market.

• A dedicated section on growth opportunities and recommendations.

• A qualitative and quantitative analysis of the global satellite flat panel antenna market at the regional and country level, and the analysis of applications, sector, platform and software technology.

Companies that manufacturers satellite flat panel antennas and satellite terminals, satellite operators and telecom operators should buy this report.

The global space-based broadband internet market is estimated to reach $52,330.8 million in...

The global hybrid-satellite cellular terminal market is expected to reach $696.4 million by...