Published Year: 2022

Biological Control Agents Market - A Global and Regional Analysis: Focus on Product, Application, an

The global biological control agents market was valued at $4.80 billion in 2021, which is...

Focus on Seed Treatment Product and Application, Supply Chain Analysis, and Country Analysis - Analysis and Forecast, 2022-2027

Global Seed Treatment Market Industry Overview

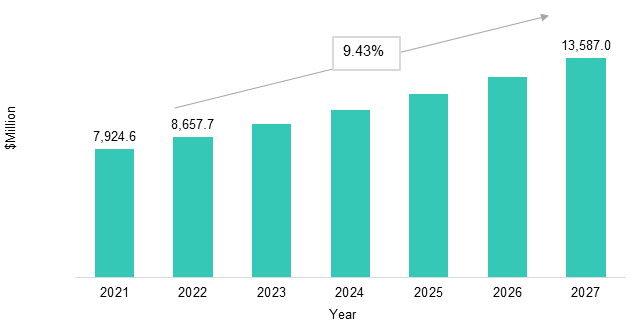

The seed treatment market was valued at $7,924.6 million in 2021, which is expected to grow with a CAGR of 9.43% and reach $13,587.0 million by 2027. The growth in the global seed treatment market is expected to be driven by increasing seed and soil-borne diseases and the growing demand for treated seeds.

Market Lifecycle Stage

The seed treatment market is in the development phase. Increased research and development activities are underway to develop treated seeds, biological seed treatment products, and seed pelleting techniques, which are expected to increase the demand for seed treatment in farming practices.

Increasing investments in the R&D of seed treatment is one of the major opportunities in the global seed treatment market. Moreover, the functions of seed treatment such as seed protection, seedling protection, and seed germination are attracting seed manufacturers, farmers, and animal feed producers.

Impact

• With an increasing precision farming and a rise in seed-borne diseases creating the market opportunity for seed treatment manufacturers. As seed treatment saves the cost in farming practices and enhances seed germination, farmers are adopting seed treatment in their farming practices. Also, North America and Europe are adopting the Agriculture 4.0 revolution trend and increasing biological seed treatment products in farming practices. This creates better opportunities in North American and European markets.

• Additionally, seed treatment products are used in various crop types including oilseeds, cereals & grains, and fruits & vegetables. The growing demand for treated seeds furthermore drives the seed treatment market during the forecast period 2022-2027.

Impact of COVID-19

COVID-19 pandemic directly impacted on manufacturing and transportation activities of the seed treatment market. Due to the pandemic, the supply chain of the seed treatment market was disturbed at the global level. Various governments closed their international trades and production units, due to these seed treatment markets being hampered more at the global level. In mid of 2021, manufacturing and transportation activities of the seed treatment started gradually, and international trades started efficiently. Therefore, the production and consumption of seed treatment products are expected to increase post-COVID-19 pandemic.

Market Segmentation:

Segmentation 1: by Application Technique

• Seed Coating

• Seed Dressing

• Seed Pelleting

The global seed treatment market in the application technique segment is expected to be dominated by the seed coating application technique. All treated seeds are mass-produced and are used seed treatment products for seed coating application techniques commonly in developing counties.

Segmentation 2: by Crop Type

• Oilseeds

• Cereals & Grains

• Fruits & Vegetables

• Others

The global seed treatment market in the crop type is expected to be dominated by cereals and grains crop type. The cereals and grains include rice, wheat, corn, sorghum, and barely. The growing demand of cereals & grains, and the rise in awareness of treated cereals & grains seeds further drive the seed treatment market in near future.

Segmentation 3: by Product Type

• Chemical Seed Treatment

• Non-Chemical Seed Treatment

The global seed treatment market is dominated by the chemical seed treatment segment. Chemical seed treatment includes insecticide, fungicide, nematicide, fertilizer, plant growth nutrients, or a combination of crop protection chemicals. The growing demand for high-value insecticide and fungicide seed treatment products are driving the chemical seed treatment market globally.

Segmentation 4: by Formulation

• Liquid Solution

• Powder

• Emulsion

• Flowable Concentrate

• Water Dispersible Powder for Slurry

• Others

The global seed treatment market is dominated by the liquid solution segment. Due to the ease of use and high effectiveness of seed treatment products, liquid solution seed treatment products are booming in the market. The increasing acceptance of biological seed treatment products and organic farming practices are driving the growth of the liquid solution formulation.

Segmentation 5: by Function

• Seed Protection

• Seed Enhancement

The seed treatment market differentiates depending on its functionality. Based on functionality, the seed treatment market is segmented into two major types, including seed protection and seed enhancement. Seed protection is a primarily important function because it enables the plant to imbibe certain beneficial properties prior to germination.

Segmentation 6: by Region

• North America - U.S., Canada, and Mexico

• Europe - Germany, France, Italy, Spain, Netherlands, and Rest-of-Europe

• China

• U.K.

• Asia-Pacific and Japan - Japan, India, Australia, Malaysia, and Rest-of-Asia-Pacific and Japan

• South America - Brazil, Argentina, Rest-of-South America

• Middle East and Africa - South Africa, Middle East, Kenya, and Rest-of-Middle East and Africa

North America generated the highest revenue of $2.41 billion in 2021, which is attributed to the R&D advancements and supporting government regulations in the North America region. North America is an attractive region for the biological seed treatment market because of the increasing demand for organic food and precision farming.

Recent Developments in Global Seed Treatment Market

• In April 2022, BASF SE opened a new center for sustainable agriculture in North America. This center is expected to increase its biological seed treatment product portfolio in North America. Due to this, the company creates awareness among the farmers and increases its biological seed treatment sales in the U.S., Canada, and Mexico.

• In May 2022, Bayer Vietnam launched Routine Start 280FS, a seed germination product for rice seeds. The growing rice seed-borne diseases and increasing rice cultivation create a demand for rice seed treatment products in Vietnam. Thus, Bayer Vietnam strategically launched a seed treatment product for rice crop in Vietnam.

• In February 2022, Croda International Plc partnered with Xampla, to create biodegradable and microplastic-free seed coatings technology. Due to this partnership, the company focuses on research and development activities and intends to pioneer in biodegradable and microplastic-free seed coatings technology in the global seed treatment market.

• In May 2022, Corteva Agriscience established its Centre for Seed Applied Technologies (CSAT) laboratory in Rosslyn. This helps Corteva Agriscience to increase its seed treatment business in Africa and Middle East countries.

• In May 2022, Syngenta launched the VICTRATO seed treatment product. This product protects soybeans, corn, cereals, cotton, and rice seeds from soil-borne fungal diseases.

Demand – Drivers and Limitations

Following are the demand drivers for the seed treatment market:

• Increased Usage of Commercial Seeds

• Growing Demand for Coated Organic Seeds

• Reduced Risk of Exceeding MRLs

The market is expected to face some limitations too due to the following challenges:

• Stringent Government Regulations

• Lower Shelf Life and High Maintenance

Analyst Thoughts

According to Rakhi Tanwar, Principal Analyst, BIS Research, "The seed treatment market has huge potential in near future. The growing seed-borne and soil-borne diseases create a lucrative business opportunity for seed treatment manufacturers. Simultaneously farmers’ acceptance for seed treatment procedures and the rise in demand of treated seeds further drive the seed treatment market during the forecast period. The supporting government policies for treated seeds in the U.S., Canada, Mexico, Argentina, and Brazil, India are further boosting the seed treatment market."

Focus on Seed Treatment Product and Application, Supply Chain Analysis, and Country Analysis - Analysis and Forecast, 2022-2027

Seed treatment is the process of applying certain physical, chemical, or biological agents to the seed prior to sowing. These agents protect the seeds from pathogens, insects, and other pest attacks. The seeds are very small in size and can easily get contaminated by fungal or bacterial infection. Due to this, farmers are widely accepting seed treatment products and treated seeds to leverage the advantages coupled with them. These seed treatment products are used in various crops including wheat, maize, soybean, canola, cotton, rice, sorghum, solanaceae, leafy vegetables, cucurbits, brassicas, root & bulb vegetables, and forage crops. In this report, the growth rate of the global seed treatment market has been accounted including factors such as products sold in previous years, treated seeds sold in previous years, government supporting policies, and area harvested under the crops, among others.

The key trends in the seed treatment market include emerging biodegradable seed coating technology, seed priming techniques for improved efficacy and a rise in high-value crops cultivation.

The global seed treatment market has seen major development by key players operating in the market, such as new product launches, acquisition & joint ventures, business expansion, partnership, and collaboration.

According to BIS Research analysis, the majority of the companies preferred new product launches and investments as a strategy to further increase their growth in the global seed treatment market. Companies such as Bayer AG, DuPont, BASF SE, and Syngenta have majorly adopted new product launches and investment strategies.

A new entrant can focus on seed treatment products for maize, fodder, soybean, and root crop types. In terms of product type, the rising demand of biological seed treatment products in Europe and North America regions are further driving the seed treatment market.

• Extensive competitive benchmarking of the top 12 players.

• Market sizing for volume and value market.

• Investment landscape including product adoption scenario, funding, and patent analysis

The companies which are manufacturing and commercializing seed treatment products, seed manufacturers, animal feed producers, forage producers, agrochemical manufacturers, research institutions, and regulatory bodies.

The global biological control agents market was valued at $4.80 billion in 2021, which is...

The agricultural adjuvants market is expected to grow from $3,298.6 million in the year 2021...

The Agricultural Surfactant Industry analysis by BIS Research projects that the market is...