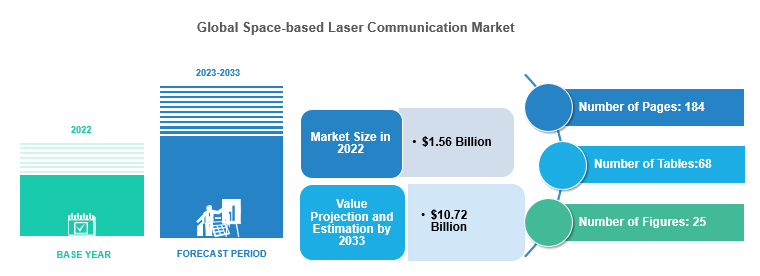

A quick peek into the report

Space-Based Laser Communication Market Report Coverage

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights gathered from primary experts.

The top established space-based laser communication providers hold around 79% of the presence in the market. The start-ups in the market hold around 21% of the global space-based laser communication market.

Key Companies Profiled:

• Bridgecomm

• General Atomics

• HENSOLDT

• LASER LIGHT COMMUNICATIONS INC

• Mynaric

• ODYSSEUS SPACE SA

• Skyloom

• SPACE MICRO, INC.

• Tesat-Spacecom GmbH & Co.

• Thales Alenia Space

Space-Based Laser Communicatiom Industry and Technology Overview

Introduction to Global Space-based Laser Communication Market

The global space-based laser communication market has experienced remarkable growth in recent years due to the deployment of second-generation satellites equipped with inter-satellite links (ISL). This growth is primarily driven by technologies such as artificial intelligence (AI), electronically steered antennas (ESAs), miniaturization of parts, and inter-satellite links (ISLs) that enhance communication performance both on the ground and in space. Additionally, the market growth is influenced by mega constellations from notable companies such as OneWeb, SpaceX, and Amazon's Project Kuiper in low Earth orbit (LEO) and medium Earth orbit (MEO). In 2023, the satellites deployed in low orbit, such as those from Starlink, are now incorporating laser terminals. These satellites form a constellation with optical inter-satellite links (OISLs), creating a robust mesh network in space. Telesat's LightSpeed constellation also plans to include optical satellite links upon its full deployment, and OneWeb is considering adding optical links in its phase two rollout. Amazon's Kuiper constellation has been designed from the outset to enable inter-satellite links. Notable companies include Tesat-Spacecom GmbH & Co., SKYLOOM, Bridgecomm, and Mynaric, among others. These companies heavily invest in research and development to introduce innovative and advanced laser terminals. The market can be segmented based on end user, application, solution, component, and range, and it is expected to witness continued growth as key players and government space agencies invest in advanced technologies to enhance performance and effectiveness, leading to new opportunities for growth and innovation in the sector.

Market Introduction

The global space-based laser communication market has witnessed significant growth and advancements in recent years. Laser-based satellite communication offers a promising opportunity to extend terrestrial network functionalities to satellite networks, effectively bridging the digital divide and enabling many applications. These applications encompass virtual private networks, edge computing, advanced 5G/6G services, seamless internet connectivity to and from space, and communication with airborne assets. The current capabilities of conventional satellite systems fall short of providing such extensive functionalities.

Furthermore, satellite constellations are expected to drive the market during the forecast period. These constellations provide global or near-global coverage, ensuring that at least one satellite is available at any time and location on Earth. This continuous coverage is particularly valuable for applications such as telecommunications, Earth observation, data relay, and global positioning systems, where uninterrupted connectivity and data acquisition are essential. The availability of satellite constellations opens new possibilities for a wide range of industries, including telecommunications, space exploration, climate monitoring, surveillance and security, and more.

Industrial Impact

The space-based laser communication market has a transformative impact by revolutionizing global communication networks with higher data rates and lower latency. This technology enhances space exploration, enables real-time control of missions, and fosters global connectivity through satellite mega constellations, bridging digital divides. It drives innovation and business opportunities across sectors such as satellite manufacturing, IoT, and data analytics. Moreover, it supports data-driven insights for scientific research, environmental monitoring, and disaster response. This growth fuels economic expansion, job creation, and educational advancements while prompting discussions on security, regulation, and sustainable space operations.

Market Segmentation:

Segmentation 1: by End User

• Government and Military

• Commercial

Based on End User, Commercial Segment to Lead the Global Space-Based Laser Communication Market

The global space-based laser communication market (by end user), including the commercial segment, is expected to dominate the market with a share of 92.72% in 2033. Its market value witnessed $1.45 billion in 2022 and is projected to reach $9.94 billion by 2033, registering a CAGR of 13.31% in the forecast period 2023-2033.

Segmentation 2: by Application

• Technology Development

• Earth Observation and Remote Sensing

• Data Relay

• Communication

• Surveillance and Security

• Research and Space Exploration

Based on Application, Communication Segment to Dominate the Global Space-Based Laser Communication Market

The global space-based laser communication market is expected to be dominated by the communication application in 2023. Space-based laser communication emerges as a notably auspicious technology poised to offer future broadband communication solutions. Among the forefront contributors in propelling satellite communication systems, TNO occupies a distinguished role. By teaming up with Hyperion Technologies, TNO is actively engaged in the advancement of the CubeCat laser terminal, tailored to cater to the specific demands of the SmallSat market.

Segmentation 3: by Solution

• Space-to-Space

• Space-to-Other Application

• Space-to-Ground Station

Segmentation 4: by Component

• Optical Head

• Laser Receiver and Transmitter

• Modulator and Demodulator

• Pointing Mechanism

• Others

Segmentation 5: by Range

• Short Range (Below 5,000 Km)

• Medium Range (5,000-35,000 Km)

• Long Range (Above 35,000 Km)

Segmentation 6: by Region

• North America - U.S. and Canada

• Europe - U.K., France, Germany, Russia, and Rest-of-Europe

• Asia-Pacific - China, India, Japan, and Rest-of-Asia-Pacific

• Rest-of-the-World - Latin America and Middle East and Africa

North America to Dominate Global Space-Based Laser Communication Market (by Region)

North America is anticipated to grow at a CAGR of 14.09%. The presence of a larger number of established space-based laser communication providers is driving the market in the region. The presence of major industry players such as General Atomics, Bridgecomm, Atlas Space Operation, and Ball Aerospace & Technologies within the region with growth strategies such as partnerships are paving the way for market opportunities.

The U.S. is one of the significant countries with various key players producing laser communication terminals. With a strong focus on space exploration, national security, and communication infrastructure, the U.S. remains at the forefront of laser communication technology, continuously exploring new applications and pushing the boundaries of high-speed, secure, and reliable data transmission in space and beyond. For instance, in August 2022, the Defense Advanced Research Projects Agency (DARPA) chose five commercial satellite operators, including SpaceX, Telesat, SpaceLink, Viasat, and Amazon's Kuiper, for its Space-Based Adaptive Communications Node (Space-BACN) project.

Recent Developments in the Global Space-based Laser Communication Market

• In August 2023, Space Development Agency (SDA) awarded a contract worth $3 million to design and develop an optical ground station for data transmission with satellites in low Earth orbit (LEO) and for the demonstration of connections with space-based optical communication terminals. SDA, under the U.S. Space Force, is building a vast constellation of military satellites, each equipped with multiple laser communication terminals. The ground terminal will include a substantial telescope along with laser transmitters and receivers. It must be compatible with optical communication terminals on SDA's satellites, which are supplied by various manufacturers.

• In June 2023, Mynaric secured a contract with Raytheon Technologies to supply optical communication terminals for the Space Development Agency (SDA)'s Tranche 1 Tracking Layer program. Raytheon Technologies, the recipient of the seven-vehicle mission satellite constellation, was awarded this prestigious program.

• In June 2023, LASER LIGHT COMMUNICATIONS INC signed a partnership with Nokia worth $25 million to start building LASER LIGHT's projected worldwide all-optical network. LASER LIGHT would utilize Nokia optical and IP solutions and technologies solely in the deal to allow the first stage of its proposed Extended Ground Network System (XGNS) to reach and service different places.

• In May 2023, Tesat-Spacecom GmbH & Co. announced a partnership with SES to develop and integrate the Quantum Key Distribution (QKD) payload for the EAGLE-1 satellite. The primary objective of this collaboration between SES and TESAT is to achieve a crucial milestone in Europe's pioneering quantum secure communications initiative, EAGLE-1. This payload includes the Scalable Optical Terminal SCOT80, which establishes a secure optical link from space to the ground, and the QKD module of the satellite.

• In May 2023, Mynaric announced that it entered into a definitive agreement for the sale of CONDOR Mk3 terminals to Loft Federal, a subsidiary of Loft Orbital. Loft Federal was selected to produce, deploy, and operate NExT – the Space Development Agency (SDA)'s Experimental Testbed and utilized the terminals to support secure and reliable communications. Terminal deliveries were primarily scheduled for the first half of 2024.

Demand – Drivers and Limitations

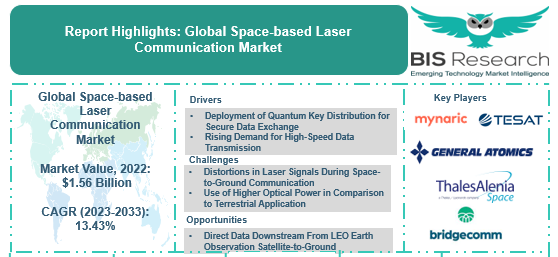

Market Demand Drivers: Deployment of Quantum Key Distribution for Secure Data Exchange

The need for robust security measures becomes even more critical in the global space-based laser communication market, where high-speed and long-range data transmission is essential. The deployment of QKD systems using laser communication is still in its early stages, but there is growing interest in the technology from government agencies, financial institutions, and other organizations that need to protect their data from attack. As the technology matures and the cost of QKD systems decreases, more widespread deployment of QKD systems using laser communication is expected during the forecast period.

Market Challenges: Distortions in Laser Signals During Space-to-Ground Communication

Laser signals can experience distortions due to atmospheric conditions, presenting a significant challenge in achieving optimal signal quality. To address this issue, adaptive optics systems, which often utilize deformable mirrors, are employed to correct for the distortions caused by the atmosphere. Despite the benefits of adaptive optics, atmospheric turbulence remains a persistent challenge for laser communications. The unpredictable nature of turbulence can still lead to fluctuations and variations in signal quality, impacting the overall performance of laser communication systems.

Market Opportunities: Direct Data Downstream from LEO Observation Satellite-to-Ground

Laser communication offers a number of advantages over radio wave communication for direct data downstream from LEO observation satellites. Lasers can transmit data at much higher speeds than radio waves, significantly improving the throughput of data from satellites to the ground. In this process, LEO observation satellites capture various data types, such as high-resolution images, environmental measurements, and other sensor readings during their orbits around the Earth.

Analyst’s Thoughts

According to Nilopal Ojha, Principal Analyst, BIS Research, “The space-based laser communication market represents a transformative frontier in the satellite communication industry, poised to revolutionize global connectivity. With the ever-increasing demand for high-speed data transmission, space-based laser communication offers a paradigm shift from traditional radio frequency systems. The convergence of various factors such as decreasing launch costs, advancements in laser technology, and the insatiable appetite for bandwidth-intensive applications such as 5G, IoT, and Earth observation, are propelling this market. Moreover, space-based laser communication promises lower latency, higher data rates, and enhanced security compared to its RF counterparts, opening up possibilities for not only the commercial satellite market but also defense and scientific missions. However, it is essential to acknowledge the inherent challenges, including atmospheric interference, beam divergence, and optical component reliability in the unforgiving space environment, that must be overcome for widespread adoption. The competitive landscape is dynamic, featuring both established aerospace giants and innovative start-ups vying for supremacy in this burgeoning sector. Government support, international collaboration, and regulatory frameworks will significantly influence market dynamics. Moreover, the space-based laser communication market is at a critical juncture, with immense growth potential contingent on technological breakthroughs and strategic partnerships, promising a future where the cosmos becomes the backbone of global connectivity.”

Space-Based Laser Communication Market - A Global and Regional Analysis

Focus on End User, Application, Solution, Component, Range, and Country - Analysis and Forecast, 2023-2033

Frequently Asked Questions

Space-based laser communication involves the transmission of data through laser beams between satellites and ground stations or between satellites themselves. This technology offers advantages over traditional radio-frequency communication, including higher data transmission rates, reduced latency, and enhanced security. Space-based laser communication systems consist of various components that work together to facilitate this data transfer. Some of the key components used in such laser terminals include an optical head, laser receiver and transmitter, modulator and demodulator, pointing mechanism, and others.

The global space-based laser communication market has seen major key players such as Tesat-Spacecom GmbH & Co., SKYLOOM, and Bridgecomm, which are capable of providing global space-based laser communications of diverse ranges. Key players are expanding their market presence by targeting new geographic regions and untapped markets to establish local offices, distribution networks, and partnerships to better serve customers and address specific regional needs.

New global space-based laser communication developers should focus on developing compact and lightweight laser terminals that can be easily integrated into various satellite platforms, including SmallSats and mega-constellations. Additionally, a strong focus on sustainable practices, regulatory compliance, and exceptional customer support can help build credibility and foster long-term partnerships with key players in the industry, establishing a competitive advantage in this rapidly evolving market.

The following can be seen as some of the USPs of the report:

• Unique title capturing global space-based laser communication market

• A dedicated section on growth opportunities and recommendations

• A qualitative and quantitative analysis of the global space-based laser communication market based on application and product, such as by component and range

• Quantitative analysis

• Regional-level qualitative analysis of the global space-based laser communication market

• A detailed company profile comprising established players and some start-ups that are capable of significant growth with an analyst view

Companies developing space-based laser terminals should buy this report. Additionally, satellite communications equipment manufacturers, EO and HTS satellite operators, data downlink service providers, such as relay network and ground station operators, financial institutions and investors, agencies funding FSOC research, optoelectronic system players, system integrators, and R&D organizations should also buy this report to get insights about the space-based laser communication demand and how they could benefit from it.