Published Year: 2022

Electric VTOL (eVTOL) Aircraft Market - A Global and Regional Analysis: Focus on Design, Range, Use

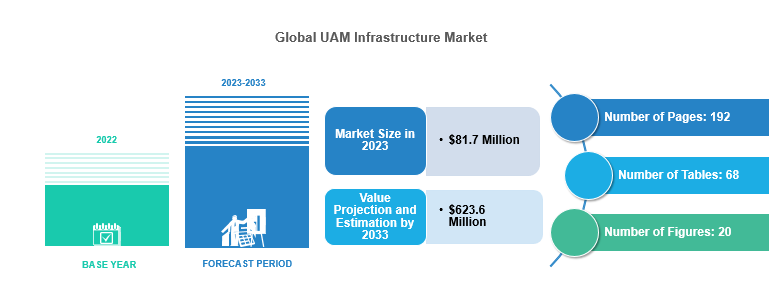

The global electric VTOL (eVTOL) aircraft market is estimated to reach $700.5 million in 2032...

Focus on Operation, Configuration, End User, Ecosystem, and Country - Analysis and Forecast, 2023-2033

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights that are gathered from primary experts.

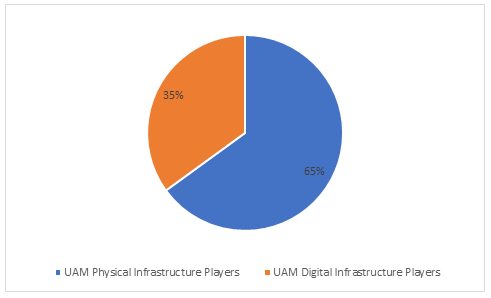

In the UAM infrastructure segment, physical infrastructure facilitators lead the segment, with around 65% of the presence in the market. Players in the digital infrastructure facilitating spectrum account for approximately 35% of the presence in the market.

Key Companies Profiled:

• Altaport, Inc.

• ANRA Technologies

• BETA Technologies

• Bluenest

• Embention

• Ferrovial

• FEV Group

• Groupe ADP

• Kookiejar

• ResilienX

• Skyports Limited

• Skyscape Corporation

• Skyway

• Urban-Air Port Ltd

• UrbanV S.p.A

• Volatus Infrastructure, LLC

The urban air mobility (UAM) infrastructure market has emerged as a crucial component in the development and implementation of futuristic transportation systems. UAM refers to the integration of air transportation into urban environments, enabling on-demand, safe, and efficient aerial mobility for passengers and cargo. This emerging industry aims to alleviate traffic congestion, reduce greenhouse gas emissions, and enhance overall transportation efficiency. The UAM infrastructure market encompasses a wide range of physical and digital assets required to support the operation of urban air vehicles. These assets include vertiports, charging and refueling stations, air traffic management systems, and communication networks. Vertiports serve as the primary hubs for UAM operations, providing takeoff and landing facilities, passenger boarding and disembarking areas, and maintenance and service infrastructure for electric aircraft.

Charging and refueling stations play a vital role in sustaining UAM operations by providing electric power or fuel for the aircraft. As the majority of UAM vehicles are expected to be electric, the development of a robust charging infrastructure is critical to enable efficient and rapid turnaround times for urban air vehicles. Additionally, advanced air traffic management systems and communication networks are essential to ensure the safe and efficient integration of UAM into existing airspace.

As the UAM industry continues to evolve, the infrastructure market is expected to witness substantial growth. It is anticipated that the demand for vertiports, charging stations, and air traffic management systems will increase as more cities embrace UAM as a viable transportation solution. The development of standardized infrastructure solutions, interoperability frameworks, and seamless integration with existing transportation systems will be key factors in shaping the future of the UAM infrastructure market.

Market Introduction

The vertical mobility ecosystem relies on five factors for commercial materialization, which include hardware, infrastructure, operations, regulations, and social acceptance. These five factors influence the vertical mobility business models and shape the systems for adoption in urban demographics. Among these factors, most developments have happened in the hardware segment, with over 100 companies invested in the hardware development phase or in the concept validation phase. In order for the sector to commence operations by 2025, the factors of infrastructure, operations, and regulations should be developed substantially. The growth of urban air mobility (UAM) systems is driving an increasing demand for dedicated UAM infrastructure, and the market has witnessed significant growth in recent years, driven by the increasing development of advanced air mobility systems and the need for efficient transportation solutions in congested urban areas. UAM infrastructure, such as vertiports, charging stations, and air traffic management systems, is being developed to support the safe and efficient operation of UAM vehicles. This infrastructure is designed to cater to the unique requirements of UAM, enabling vertical takeoff and landing, electric propulsion, and integration with existing transportation networks.

Industrial Impact

The UAM infrastructure market is poised to have a profound impact on various industries, ushering in a new era of urban transportation. One of the primary benefits of a well-developed UAM infrastructure is the alleviation of traffic congestion in densely populated cities. By taking to the skies, UAM vehicles can bypass ground-level congestion, reducing travel times and improving overall efficiency. This enhanced mobility will not only benefit commuters but also have far-reaching implications for industries such as logistics and e-commerce, where quick and reliable transportation of goods is crucial.

In the upcoming years, UAM infrastructure market will register an exponential surge in demand from the scaling up of UAM services, with initial high demands for the airport shuttle services segment. Additionally, there will be a requirement for cargo hubs and specialized facilities, driven by the e-commerce and last mile delivery segment, which is expected to grow incrementally in the upcoming years, facilitated by advanced air mobility (AAM) delivery options, that will enhance the handling and logistics. For instance, in November 2022, Skyports and Groupe ADP launched the European vertiport terminal testbed in Paris, France. The testbed vertiport is aircraft agnostic and offers a chance for European eVTOL OEMs to validate the factors of their cargo and unmanned operations.

Market Segmentation:

Segmentation 1: by End User

• Airport Shuttle Service

• Healthcare

• Last Mile Delivery

• Tourism

Airport Shuttle Service End User to Lead the UAM Infrastructure Market

The UAM infrastructure market is led by the airport shuttle services segment, with a 45% share in 2023. Increasing UAM developments and commercialization of UAM operations for passenger and cargo transit in the coming years are driving the growth of the UAM infrastructure market.

As urban air mobility (UAM) continues to revolutionize how people move within cities, airport shuttle services are at the forefront of this transformative shift. These cutting-edge services utilize eVTOL aircraft to provide swift and efficient transportation to and from airports. The UAM airport shuttle services segment offers passengers a seamless travel experience. Instead of relying solely on conventional ground transportation, travelers have the option to board an eVTOL aircraft, which seamlessly navigates urban airspace to transport them to their desired airport destinations. These advanced aircraft combine the agility of helicopters with the efficiency and sustainability of electric propulsion, enabling quick and eco-friendly travel. Passengers can access UAM airport shuttle services through dedicated vertiports or helipads strategically located near or within the premises of major airports.

Segmentation 2: by Operation

• Passenger Gate-to-Gate

• Cargo Gate-to-Gate

• Hybrid Passenger and Cargo Gate-to-Gate

• Off-Nominal Operations

Passenger Gate-to-Gate to Dominate as the Leading Segment by Operation

The passenger gate-to-gate segment is expected to generate huge revenues for the application segment, followed by the cargo gate-to-gate.

The passenger gate-to-gate segment forms a major segment of the potential UAM market, with most major players working toward urban passenger transit as the primary end goal for the commercialization of their offerings. In this segment, various stakeholders collaborate to create a comprehensive ecosystem that ensures safe, efficient, and convenient passenger experiences. The infrastructure catering to this segment is strategically located in urban centers, airports, and other transportation hubs to optimize accessibility and connectivity. Additionally, they are equipped with state-of-the-art facilities such as boarding gates, passenger lounges, and baggage handling systems to enhance comfort and streamline operations. In conjunction with the physical infrastructure, advanced air traffic management systems play a critical role in enabling gate-to-gate operations.

Segmentation 3: by Configuration

• Private Operations

• Public Operations

• Single Fleet Operators

• Multiple Fleet Operators

• Piloted Operations

• Autonomous Operations

• Vertiplex

Public Operations to Dominate as the Leading Segment by Configuration

The UAM infrastructure market is led by the public operations in the configuration segment, with a 20% share in 2023, and is expected to grow to 30% by 2033, owing to the commercialization of UAM operations. Increasing UAM developments and commercialization of UAM operations for passenger and cargo transit in the coming years are driving the growth of the UAM infrastructure market.

The public operations segment of the vertiports in the UAM market represents a pivotal aspect of the evolving transportation landscape, focusing on the public-facing operations and services offered at these specialized facilities. Public vertiports should be designed to handle high volumes of passengers, ensuring efficient passenger flow, security screening, and ticketing services. Integration with existing public transportation networks and seamless intermodal connectivity is a key aspect of public vertiports. Public vertiports will be built once the segment commercializes the volume of operations, as the public vertiports are cost-intensive, and collaborative usage will reduce the net expenses incurred for the infrastructure. This will also potentially allow for cross-collaboration of services in the near future.

Segmentation 4: by Ecosystem

• Physical Infrastructure

• Digital Infrastructure

Physical Infrastructure to Witness the Highest Growth between 2023 and 2033

The UAM infrastructure market is dominated by the physical infrastructure segment in 2023, with a 92.53% share in terms of revenue due to the high demand for UAM ground segment physical infrastructure to accommodate and initiate the UAM operations.

In terms of physical infrastructure, the UAM market is characterized by the need for vertiports, landing pads, and charging stations strategically distributed throughout urban landscapes. These structures must be carefully designed to accommodate UAM platforms, ensuring safe and efficient operations while optimizing available space. The UAM digital infrastructure offerings are constituted of four elements, namely, the control center (systems for remote surveillance), air traffic management (ATM), unmanned traffic management (UTM), and navigation aids and connecting networks.

Segmentation 5: by Country

• U.S.

• U.K.

• U.A.E.

• Saudi Arabia

• France

• Australia

• Italy

• Netherlands

• South Korea

• China

• Japan

• India

• Brazil

• Germany

• Singapore

The U.S. has the highest growing market in the countries, registering a CAGR of 21.43%. The U.S. market for UAM infrastructure is poised for significant growth and is expected to be one of the largest markets globally. With a favorable regulatory environment and significant investments in research and development, the market is expected to reach substantial revenue figures. The market size is driven by the country's large urban population, economic potential, and favorable business ecosystem. The country has most of the major global eVTOL developers, including Archer Aviation, Joby Aviation, Wisk Aero, Jaunt Air Mobility, and many others, who are rapidly advancing their prototype development toward certification and operational induction. Out of the over $5 billion invested globally in the development of the UAM ecosystem, the U.S. accounts for the largest investment base and development of the eVTOL platforms. All these factors potentially make the U.S. a multi-billion-dollar market for UAM services.

Recent Developments in the UAM Infrastructure Market

• In May 2023, Ferrovial and Milligan announced a partnership to develop a network of vertiports in the U.K. Milligan would act as the real estate identification and assessment partner for the development of urban vertiports.

• In April 2023, Skyway and Skyportz announced a strategic partnership to develop complacent infrastructure for the Australian UAM segment.

• In March 2023, Kookiejar and Terminal Holdings, an Abu Dhabi-based ground handling service provider, signed a memorandum of understanding (MoU) for collectively building and operating vertiports for the growing UAM sector.

• In March 2023, Ferrovial and Eve Air Mobility signed a letter of intent (LoI) to explore the integration of Eve’s urban air traffic management (UATM) software solutions in the vertiports developed by Ferrovial.

• In January 2023, Skyway and Siemens announced a collaboration to factor in the electrical and digital infrastructure that would be essential to support vertiport operations.

Demand – Drivers and Limitations

Following are the drivers for the UAM infrastructure market:

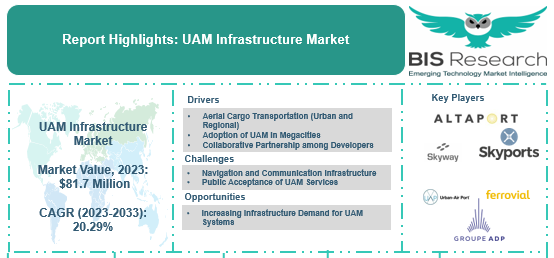

• Urban and Regional Aerial Cargo Transportation

• Adoption of Urban Air Mobility in Megacities

• Collaborative Partnership among UAM Infrastructure Developers and eVTOL Manufacturers

Following are the challenges for the UAM infrastructure market:

• Constraints in Navigation and Communication Infrastructure Supporting UAM

• Public Acceptance of UAM Services

• Lack of Electrical Infrastructure for UAM Charging

• Real Estate and Financing Challenges in Developing UAM Infrastructure

Following are the opportunities for the UAM infrastructure market:

• Increasing Infrastructure Demand for UAM Operations

• Repurposing Existing Aviation Infrastructure into Vertiport Hubs

Analyst’s Thoughts

Nilopal Ojha, Principal Analyst, BIS Research, states, “The unmanned industry is witnessing significant growth in recent years, and this shift is due to the increasing application of unmanned platforms for various applications, thereby presenting a major opportunity for the growth of more robust and connected UAM infrastructure for smooth operations in the urban landscape. Further, the UAM infrastructure in U.S., Japan, Australia, and Germany is expanding continuously due to the large urban population of the countries, economic potential, and favorable business ecosystem.”

Focus on Operation, Configuration, End User, Ecosystem, and Country - Analysis and Forecast, 2023-2033

The key trends in the UAM infrastructure market are:

Urban Passenger Air Metro: Urban passenger air metro offers an alternative mode of transport by utilizing airspace to alleviate traffic congestion and provide rapid transit options for well-off urban dwellers. Many eVTOL players are primarily focusing on addressing this market.

Operational Environment: The operational environments of UAM pose unique challenges due to the presence of low altitude operations constraints and dense buildings. Low altitude operations constraints encompass various factors such as limited airspace availability, high population density, and complex urban infrastructure. These constraints necessitate the development of sophisticated flight management systems.

Configuration Decisions: The redundancy factor will influence the decision to bring about multiple drop-off points in an urban air transit route, and the point should be configurable to be adept for servicing hybrid systems that can require refueling/charging.

The global UAM infrastructure market has seen major key players such as Skyports, Urban-Air Port, Skyway, and Ferrovial, which are capable of providing various elements of the UAM infrastructure essential for facilitating UAM operations. Key players are offering modular and customized physical infrastructure and digital infrastructure solutions and target the diverse market via contracts, agreements, and partnerships through their global presence.

New UAM infrastructure developers, which include physical infrastructure and digital infrastructure facilitators, should focus on providing highly specialized end-to-end solutions and services for the widely diversified UAM industry, where interoperability will become a key factor once commercial-scale UAM operations scale up. This will differentiate their product offerings from the other facilitators. Modular elements can also potentially scale up the offerings of the developers in both segments respectively.

The following can be seen as some of the USPs of the report:

• Unique title capturing the UAM infrastructure market.

• A dedicated section on growth opportunities and recommendations.

• A qualitative and quantitative analysis of UAM infrastructure market based on application and product.

• Quantitative analysis of end user sub-segment, which includes:

o Airport Shuttle Services

o Healthcare

o Last Mile Delivery

o Tourism

• Country-level forecast on UAM infrastructure, which includes operation segments such as passenger gate-to-gate, cargo gate-to-gate, hybrid passenger and cargo gate-to-gate, and off-nominal operations and ecosystem segments, which include physical infrastructure and digital infrastructure.

• A detailed company profile comprising established players and some startups that are capable of significant growth with an analyst view.

Companies facilitating the development of UAM infrastructure, which includes physical infrastructure, digital infrastructure, or both, and providing end-to-end UAM services. Additionally, end users such as eVTOL OEMs, aviation infrastructure operators, and civil infrastructure developers should also buy this report to get insights about the emerging UAM infrastructure demand and how they could benefit from it.

The global electric VTOL (eVTOL) aircraft market is estimated to reach $700.5 million in 2032...

The U.S. urban air mobility market is estimated to reach $18,813.0 million in 2035, at a...

The urban air mobility industry analysis by BIS Research projects the market to have a...