A quick peek into the report

Global Biopesticides and Biofertilizers Market Overview

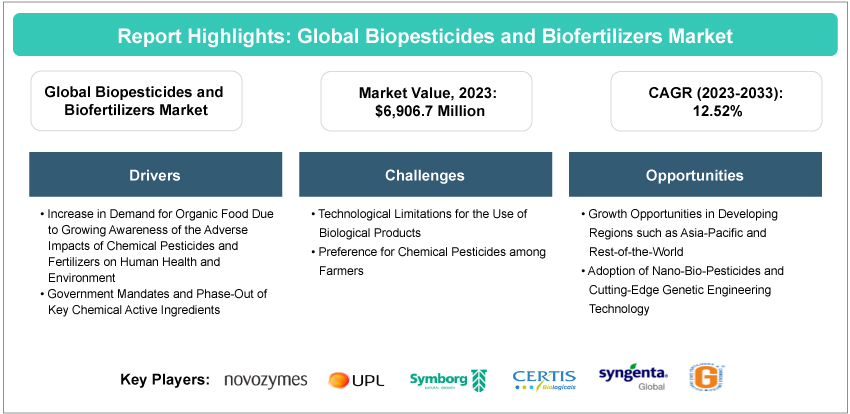

The biopesticides and biofertilizers market was valued at $6,906.7 million in 2023, and it is expected to grow at a CAGR of 12.52% and reach $22,463.3 million by 2033. Biopesticides and biofertilizers are poised to revolutionize agricultural practices by offering several advantages over conventional chemical inputs. These bio-based alternatives require fewer resources and can potentially mitigate pollution and soil degradation associated with traditional agriculture. Research suggests that biopesticides and biofertilizers produced using sustainable methods could substantially reduce environmental impacts, with greenhouse gas emissions potentially decreasing. Furthermore, the adoption of bio-based solutions could lead to a reduction in antibiotic usage, thus lowering the risk of foodborne illnesses and promoting healthier ecosystems. As the market for sustainable agriculture continues to expand, biopesticides and biofertilizers are positioned to play a crucial role in meeting the growing demand for environment-friendly farming practices.

Introduction of Biopesticides and Biofertilizers

The market study on biopesticides and biofertilizers market conducted by BIS Research considered biopesticides to be naturally derived substances or microorganisms used for controlling pests, diseases, or weeds in agriculture. They include living organisms such as bacteria, fungi, viruses, or botanical extracts and are employed as alternatives to traditional chemical pesticides. On the other hand, biofertilizers are formulations containing living microorganisms such as bacteria, fungi, or algae, which enhance the fertility and nutrient availability in the soil. These microorganisms form symbiotic relationships with plants, aiding nutrient absorption and promoting plant growth. Both biopesticides and biofertilizers play a crucial role in eco-friendly and sustainable agricultural systems, aligning with the principles of integrated pest management (IPM) and organic farming. Their use aims to reduce reliance on synthetic pesticides and fertilizers, fostering a more balanced and environment-friendly approach to agriculture.

Market Introduction

The biopesticides and biofertilizers market has witnessed significant growth due to a rising emphasis on sustainable agriculture. Biopesticides, derived from natural sources, offer eco-friendly pest control solutions, reducing environmental impact. Biofertilizers, comprising beneficial microorganisms, enhance soil fertility and nutrient absorption in plants. This market surge is fueled by increasing awareness about the adverse effects of chemical inputs on ecosystems and human health. With a growing demand for organic produce, the adoption of biopesticides and biofertilizers is poised for continued expansion, contributing to a more environment-friendly and sustainable approach to modern agriculture.

Industrial Impact

The biopesticides and biofertilizers market signifies a profound industrial impact across various sectors. These bio-based alternatives offer a sustainable solution to conventional chemical products, reducing environmental harm and promoting ecosystem health. By curbing soil and water contamination, diminishing energy consumption, and preserving biodiversity, biopesticides and biofertilizers foster a more sustainable agricultural landscape. Moreover, their reduced toxicity levels ensure safer working environments for farmers and healthier food for consumers. The biopesticides and biofertilizers market fosters innovation in biotechnology, driving research and development toward more effective formulations and application methods. Regulatory frameworks are essential to ensure product safety and compliance standards. Overall, the rise of biopesticides and biofertilizers marks a transition toward environmentally conscious agriculture, laying the groundwork for a more resilient and sustainable food system.

The key players operating in the biopesticides and biofertilizers market include Novozymes, Symborg, Kiwa Bio-Tech Products Group Corporation, Vegalab SA, UPL, Lallemand Inc., T. Stanes and Company Limited, Chr. Hansen Holding A/S, AgriLife (India) Private Limited, Syngenta, Certis USA L.L.C., Andermatt Group AG, Gujarat State Fertilizers & Chemicals Limited (GSFC), Biolchim SPA, and Biobest Group, among others. These companies are focusing on strategic partnerships, collaborations, and product launches to enhance their product offerings and expand their market presence in the biopesticides and biofertilizers industry.

Market Segmentation:

Segmentation 1: by Crop Type

• Cereals and Grains

• Oilseeds and Pulses

• Fruits and Vegetables

• Others

Cereals and Grains to Dominate the Global Biopesticides and Biofertilizers Market (by Crop Type)

In 2022, the biopesticides and biofertilizers market was predominantly led by the cereals and grains crop type. Cereals and grains, being staple crops worldwide, have witnessed increased adoption of bio-based solutions due to their crucial role in food security and the need to reduce the environmental impact of farming. In cereal production, biopesticides based on Bacillus thuringiensis (Bt) and biofertilizers rich in nitrogen-fixing bacteria are becoming more popular for managing pests such as corn borers and boosting soil fertility, respectively. For instance, the widespread use of biofungicides containing Trichoderma spp. in controlling fungal diseases in cereal crops showcases the efficacy of biopesticides. The emphasis on sustainable intensification in cereal production, coupled with the desire to minimize synthetic chemical inputs, has driven the preference for biopesticides and biofertilizers in the cereals & grains segment, positioning it as a leader in the biopesticides and biofertilizers market.

Segmentation 2: by Product Type

• Biofertilizers

o Nitrogen Fixing

o Phosphate Stabilizers

o Others

• Biopesticides

o Bioinsecticides

o Biofungicides

o Bioherbicides

o Others

Biopesticides to Dominate the Global Biopesticides and Biofertilizers Market (by Product Type)

In 2022, biopesticides emerged as the leading category in the biopesticides and biofertilizers market, signifying a significant shift toward sustainable and eco-friendly pest management practices. The heightened global awareness of the environmental and health hazards associated with chemical pesticides has driven the demand for biopesticides. These products, derived from natural sources such as bacteria, fungi, and plant extracts, offer effective pest control while minimizing ecological impact. Government regulations promoting the use of bio-based solutions, coupled with consumer preferences for organic produce, have further propelled the use of biopesticides. As the agriculture industry continues to prioritize sustainability, biopesticides are poised to dominate the market, showcasing a paradigm shift toward safer and more environmentally responsible pest control methods.

Segmentation 3: by Source

• Microorganism

o Bacteria

o Fungi

o Others

• Plant-Incorporated Protectants

• Biochemical

Microorgansim to Dominate the Global Biopesticides and Biofertilizers Market (by Source)

Microorganisms, including bacteria, fungi, and viruses, play a pivotal role in the development of biopesticides and biofertilizers due to their natural ability to control pests and enhance soil fertility. Bacillus thuringiensis (Bt), a bacterium widely utilized in biopesticides, produces toxins lethal to certain insect pests, offering an environment-friendly alternative to chemical insecticides. Furthermore, nitrogen-fixing bacteria such as Rhizobium are extensively used in biofertilizers to enhance soil fertility, especially in leguminous crops. The emphasis on harnessing the biological potential of microorganisms aligns with the global push toward sustainable agriculture. Therefore, owning to these factors, microorganism sources led the biopesticides and biofertilizers market in 2022.

Segmentation 4: by Formulation

• Liquid

• Solid

Liquid to Dominate the Global Biopesticides and Biofertilizers Market (by Formulation)

In 2022, the liquid form led the biopesticides and biofertilizers market. The popularity of liquid formulations can be attributed to their ease of application, efficient absorption, and convenient integration into existing farming practices. Liquid biopesticides offer farmers a flexible and straightforward method for pest management, ensuring thorough coverage of crops. Likewise, liquid biofertilizers containing beneficial microorganisms, enzymes, or nutrients present a user-friendly approach to enhancing soil fertility. The convenience of application through irrigation systems further contributes to the appeal of liquid forms in the biopesticides and biofertilizers market.

Segmentation 5: by Region

• North America: North America, U.S., Canada, and Mexico

• Europe: Germany, U.K., France, Italy, Spain, and Rest-of-Europe

• Asia-Pacific: China, Japan, Australia and New Zealand, India, Indonesia, and Rest-of-Asia-Pacific

• Rest-of-the-World: South America and Middle East and Africa

North America led the global biopesticides and biofertilizers market in 2022 owing to a combination of factors that underscore the region's commitment to sustainable agriculture. Stringent regulations on chemical pesticide and fertilizer usage in the U.S. and Canada have driven farmers to adopt eco-friendly alternatives, contributing to the market's growth. Additionally, heightened awareness among North American consumers about the environmental and health impacts of synthetic inputs has led to an increased demand for organic produce, compelling farmers to embrace biopesticides and biofertilizers. Government initiatives and support for sustainable agriculture practices, such as the Organic Certification Program in the U.S., have incentivized the adoption of bio-based solutions.

Recent Developments in the Global Biopesticides and Biofertilizers Market

• In September 2023, Biobest Group N.V., in collaboration with Aqua Capital, GIC, and Biotrop management, finalized a binding agreement for Biobest's acquisition of Biotrop Participações s.a. This strategic decision may bring about several implications for the involved companies, potentially influencing their market positioning and activities in the biopesticides and biofertilizers market.

• In August 2023, Bionema Group Ltd., a leading U.K.-based developer and manufacturer specializing in biocontrol technology, biostimulants, and biofertilizers, unveiled a new range of biofertilizer products designed for various uses across the country. These applications encompass agriculture, horticulture, forestry, sports turf, and amenities. The fresh line comprises four biofertilizers, each containing live microbes. These microbes play a crucial role in enhancing plant nutrition by either mobilizing or increasing the accessibility of nutrients in soils and substrates.

• In May 2023, Renaissance BioScience Corp., a leading figure in bioengineering for the global agriculture and food industries, announced that its request for a field study had been authorized by the Pest Management Research Agency (PMRA) of the Canadian government. The approval is related to the company's groundbreaking RNA interference (RNAi) biopesticide delivery technology, recognized for its environmentally friendly and sustainable features.

• In November 2022, Taiwan successfully developed a biopesticide devoid of toxins, offering protection against stubborn pests. The country is poised to be the first to undertake large-scale production of this innovative product. The achievement signifies a significant step forward in agricultural innovation and pest management for Taiwan in the biopesticides and biofertilizers market.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Increase in Demand for Organic Food Due to Growing Awareness of the Adverse Impacts of Chemical Pesticides and Fertilizers on Human Health and Environment

Organic farming is gaining increased advocacy as an optimal alternative to conventional techniques, aiming to minimize the overall environmental impact. According to the Organic Trade Association, in 2022, sales of organic food in the U.S. surpassed $60 billion for the first time, marking yet another significant milestone for the resilient organic industry. Significant growth in the organic food industry worldwide is projected to fuel the growth of the biopesticides and biofertilizers market.Moreover, according to the United Nations Environment Programme Report 2022, the negative impacts of pesticides on human health encompass both immediate and prolonged effects. Approximately 385 million instances of non-fatal unintentional pesticide poisoning and around 11,000 fatalities occur annually. Additionally, there are 1 to 2 million cases of self-poisoning each year, leading to approximately 168,000 deaths. Scientific evidence highlights significant links between occupational or residential exposure to specific pesticide groups (or pesticides in general) and various adverse health outcomes, including cancers, neurological disorders, immunological issues, and reproductive effects. Exposure to pesticides during pregnancy or childhood has been linked to childhood leukemia. While existing data on pesticide residues in food suggests low dietary risks, the broader spectrum of health concerns associated with pesticide exposure remains substantial.

While direct human health effects from fertilizers are infrequent, they can be severe during specific stages of the fertilizer life cycle. Instances of such impacts may include inhaling ammonia and dust particles from manure. Although storage and transport accidents are uncommon, when they do occur, they can lead to substantial loss of human life. For example, the incident in Tianjin, China, in 2015 resulted in 173 fatalities, and the incident in Beirut, Lebanon, in 2020, claimed 220 lives.

As biopesticides and biofertilizers are chemical-free, they do not have any residual effect that harms humans, animals, or the environment. Hence, the biopesticides and biofertilizers market demand is increasing with the growing popularity of organic foods.

Market Challenges: Technological Limitations for the Use of Biological Products

Biological products are prone to contamination and have a short or limited shelf life. According to an article published in the International Journal of Pharmaceutical & Biological Archives, one of the main issues with agricultural inoculation technology is the ability of microorganisms to survive storage. The other problematic parameters that affect the shelf life of inoculants are water activity, exposure to sunlight, culture mediums, the physiological state of the microorganisms when harvested, and temperature maintenance during storage. The compatibility of microbial inoculants with other agricultural products, such as chemical fungicides and herbicides, presents another issue with their use in the soil.

The following are some of the main technological barriers to the use of biological products:

• Using ineffective and inappropriate strains for production

• Insufficient technical, skilled, and experienced staff

• The lack of superior carrier materials or the usage of alternative materials by manufacturers without verifying the material's quality

• Limited shelf life as a result of numerous biotic and abiotic stress factors

Moreover, products containing biofertilizers have a short shelf life and are highly contaminated. The microorganisms used as biofertilizers become nonviable when exposed to high temperatures. Therefore, it's essential to keep them in a cool, dry environment. The primary challenge with agricultural inoculation technology is the survival of microorganisms during storage; additional challenges stem from various factors such as culture medium, harvesting microorganisms' physiological state, dehydration process, drying rate, temperature maintenance during storage, and water activity of inoculants. These challenges affect the microorganisms' shelf life.

Ongoing research and development are necessary to enhance the performance of biological products. However, challenges in funding, expertise, and understanding the complex interactions within ecosystems can slow down progress.

Addressing these technological limitations is crucial for the broader adoption of biopesticides and biofertilizers, ensuring they become more competitive alternatives to traditional chemical-based solutions in modern agriculture.

Market Opportunities: Growth Opportunities in Developing Regions such as Asia-Pacific and Rest-of-the-World

An opportunity in the biopesticides and biofertilizers market lies in the potential for growth in developing regions, particularly in areas such as Asia-Pacific and the Rest-of-the-World (RoW). These regions present favorable conditions for the expansion of the bio-based agricultural solutions market.

Food and Agriculture Statistics (FAOSTAT) reports that the U.S., Brazil, China, and Argentina are now the world's top pesticide consumers. The increase in middle-class families, population growth, and disposable income have all contributed to the rise in food demand in these areas. As a result, to increase crop yields, pesticide use has increased. However, these areas now face serious problems with pollution, contaminated soil, and worries about the detrimental effects of chemical pesticides on the food chain. Governments are pushing for integrated pest management techniques as a solution to these issues.

Government organizations finance large-scale production and promote the use of biopesticides by enacting advantageous regulatory policies and offering subsidies in nations such as China and India, where farmers generally own smaller landholdings and struggle financially. Over in South America, a similar trend is noted. Owing to low entry barriers and a comparatively small number of producers, the biopesticides market in these regions offers opportunities for new players. Significant agricultural industry participants are currently making investments in these regions' developing markets. In the Asia-Pacific and South American regions, biopesticide consumption is predicted to rise as farmer awareness of the advantages of applying these pesticides develops.

In developing nations, particularly those in Southeast Asia, the use of pesticides in agriculture is rising quickly. According to WHO data, the percentage of pesticides used in developing nations is 20%, and this percentage is rising. According to reports, Vietnam's imports of pesticides have increased by 10%, Laos's by 55%, and Cambodia's by 61% annually.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The biopesticides and biofertilizers market is likely to grow multi-fold in the coming years, owing to the rapidly growing demand for sustainable agriculture, increasing awareness of the environmental impact of chemical inputs, and increasing demand for organic produce. This increased interest aligns with increasing environmental awareness, shifting consumer preferences, and advancements in bio-agriculture, creating a favorable landscape for the widespread acceptance and expansion of the biopesticides and biofertilizers market. Moreover, substantial investments in the biopesticides and biofertilizers market further reinforce its growth potential. As investors recognize the economic and environmental benefits of biopesticides and biofertilizers, increased funding is facilitating research, development, and scaling of production processes. The biopesticides and biofertilizers market is expected to witness significant growth in the coming years, and the key players in the market are focused on strategic partnerships, collaborations, mergers, and acquisitions to expand their market presence and enhance their product offerings.”

Global Biopesticides and Biofertilizers Market

A Global and Regional Analysis, 2023-2033

Frequently Asked Questions

Ans: The market study conducted by BIS Research considered the definition of biopesticides to be naturally derived substances or microorganisms used for controlling pests, diseases, or weeds in agriculture. They include living organisms such as bacteria, fungi, viruses, or botanical extracts and are employed as alternatives to traditional chemical pesticides. On the other hand, biofertilizers are formulations containing living microorganisms such as bacteria, fungi, or algae, which enhance the fertility and nutrient availability in the soil. These microorganisms form symbiotic relationships with plants, aiding in nutrient absorption and promoting plant growth.

Ans: The key business opportunities in the biopesticides and biofertilizers market are growth opportunities in developing regions such as Asia-Pacific and Rest-of-the-World, and the adoption of nano-biopesticides and cutting-edge genetic engineering technology presents significant opportunities.

Ans: The biopesticides and biofertilizers market is poised to grow over time, compelling companies to come up with collaborative strategies to sustain themselves in the intensely competitive market. Companies with an identical product portfolio with a need for additional resources often partner and come together for joint venture programs, which help the companies gain access to one another’s resources and facilitate them to achieve their objectives faster.

Ans: A new entrant can focus on partnering with the existing biopesticides and biofertilizers market. Also, start-ups can focus on funding, launching new innovative products, and expanding their sales and distribution networks.

Ans: The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the biopesticides and biofertilizers market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the biopesticides and biofertilizers market landscape

• Qualitative and quantitative analysis of the biopesticides and biofertilizers market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Ans: Biopesticide and biofertilizer manufacturers, government agencies, agrochemical companies, farmers and growers, and investors can buy this report.