Published Year: 2022

Geospatial Imagery Analytics Market - A Global and Regional Analysis: Focus on Application, Solution

The global geospatial imagery analytics market is estimated to reach $32.78 billion in 2032...

Focus on Application and Solution - Analysis and Forecast, 2023-2033

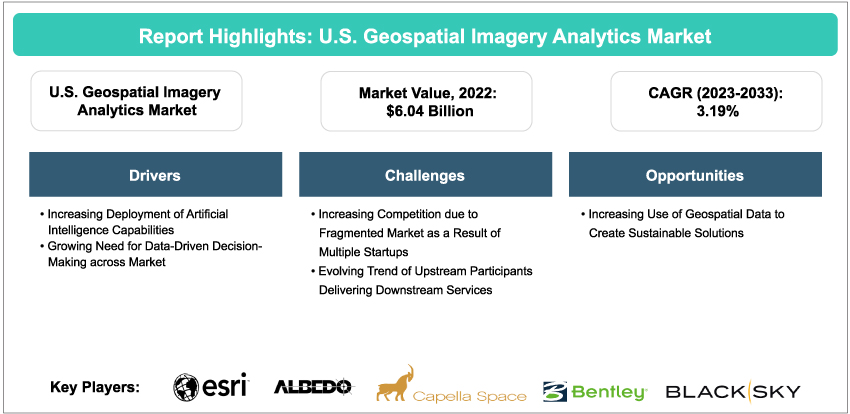

The U.S. geospatial imagery analytics market has experienced remarkable growth in recent years due to the increasing use of geospatial technologies in various industries such as transportation, agriculture, maritime, and defense. The widespread adoption of artificial intelligence (AI), machine learning (ML), and cloud computing geospatial technologies led to the growth of geospatial imagery analytics in the U.S. Regional organizations are consuming large amounts of data generated through remote sensing, geographic information systems (GIS), global positioning systems (GPS), and internal mapping technologies. For instance, in February 2023, IBM and the National Aeronautics and Space Administration (NASA)’ Marshall Space Flight Center signed a collaboration to use artificial intelligence (AI) to process geospatial data quickly. The partnership includes the integration of AI with large datasets from NASA’s Earth observation satellites for quicker and easier climate research analysis. The U.S. geospatial imagery analytics market is characterized by intense competition, with several key players operating in the industry. Notable companies include BENTLEY SYSTEMS, INCORPORATED, BlackSky Technology Inc., Esri, Maxar Technologies Inc., and others. These companies heavily invest in research and development to introduce innovative products. The market also features smaller and medium-sized companies offering specialized products. With the increasing demand for geospatial imagery analytics, the market is anticipated to experience significant growth in the coming years as more industries recognize the benefits of utilizing services such as remote sensing, environmental monitoring, infrastructure, and asset management. The market can be segmented based on application and product, and it is expected to witness continued growth as key players and defense forces invest in advanced technologies to enhance performance and effectiveness, leading to new opportunities for growth and innovation in the sector.

Introduction to the U.S. Geospatial Imagery Analytics

New technologies, such as machine learning (ML) and artificial intelligence (AI), enable businesses and government organizations to analyze large amounts of data in real time for better decision-making. ML and AI algorithms excel in pattern recognition, predictive analysis, and automation, providing valuable insights, optimizing operations, and enhancing overall efficiency. This digital revolution is not only enhancing decision-making processes but also shaping the future of industries across various sectors, including healthcare, finance, transportation, and more. Furthermore, high-resolution satellite images and geospatial data are becoming more widely available, which is one of the factors driving the growth of the market.

Furthermore, the rise in deployment of small-satellite constellations in the U.S. by various companies such as Capella Space, Descartes Labs, Inc., and Planet Labs PBC are capable of cost-effective geospatial solutions. The regional companies have access to high-resolution satellite imagery data through the Earth observation satellites in orbit. There are approximately 1,000 Earth observation satellites, out of which more than 600 of these satellites are being operated by the U.S. Hence, deploying more satellites has decreased the satellite imagery acquisition cost and made it more affordable for geospatial services.

Furthermore, the region is collaborating with commercial geospatial service providers through contracts and partnerships for intelligence and defense needs. For instance, in March 2023, Planet Labs PBC announced that its wholly owned subsidiary, Planet Labs Federal, Inc., secured a contract from the National Reconnaissance Office (NRO) under the Strategic Commercial Enhancements (SCE) Broad Agency Announcement (BAA) program, with a specific focus on Commercial Hyperspectral Capabilities (CHC).

Industrial Impact

The U.S. geospatial imagery analytics market is witnessing rapid growth due to the growing demand for integrated domain awareness solutions, the deployment of small-satellite constellations, and the need for real-time data for surveillance or commercial purposes.

The increasing deployment of small satellites for Earth observation applications is another factor that is driving the geospatial imagery analytics in the region. In 2022, the region contributed more than 140 Earth observation satellites in orbit. The high-resolution remote sensing data is utilized by various geospatial imagery analytics providers for offering solutions to commercial and government organizations. For instance, Planet Labs PBC, a satellite imagery data provider, manages terabytes of satellite datasets through its satellite constellation of more than 150 satellites. The company provides satellite imagery data access to users through its web-based tools, such as the application programming interface (API). However, compliance with regulations and international agreements regarding the collection, storage, and use of geospatial data can be complex and may vary by region.

Market Segmentation:

Segmentation 1: by Application

• Aviation

• Maritime

• Agriculture and Forestry

• Sustainability and Natural Resource Monitoring

• Oil and Gas

• Energy

• Logistics/Shipping

• Defense

• Civil Government

• Construction and Infrastructure Development

• Healthcare

• Surveying/Cartography

• Disaster Management

• Business Intelligence

• Finance and Insurance

• Mining

Construction and Infrastructure Development in Application Section to Dominate the U.S. Geospatial Imagery Analytics Market

The construction and infrastructure development segment of the U.S. geospatial imagery analytics market is estimated to be $0.88 billion in 2022 and is expected to grow up to $1.34 billion by 2033, growing at a CAGR of 4.07%. The Building Information Modeling (BIM) industry's rapid evolution caused a significant impact on both the construction and the design industries. BIM and GIS integration development brings a new way of thinking about construction and planning. This process includes a transition from 2D to 3D, building information modeling on the digital front. Additionally, GIS data is required to plan various infrastructure operations such as roads, trains, and airports.

Segmentation 2: by Solution

• Data Acquisition

• Data Processing

• Analytics

• Integrated Delivery Platform

Analytics in Product Section to Dominate the U.S. Geospatial Imagery Analytics Market by Solution

The U.S. geospatial imagery analytics market is expected to be dominated by analytics in 2023, with $2.57 billion in 2022 in terms of revenue, and is expected to reach $3.57 billion in 2033. In this market, there are companies such as Orbital Insight that offer AI-powered software platforms. The Orbital Insight platform can perform analytics using a variety of geospatial data sources, including satellite and aerial images, location data, automatic identification system (AIS) data, and more. Similarly, EOS Data Analytics, a cloud-based solutions provider, offers the EOSDA platform for tasks such as crop monitoring, land observation, and forest monitoring. This platform leverages deep learning algorithms to analyze satellite imagery and deliver actionable insights.

Recent Developments in the U.S. Geospatial Imagery Analytics Market

• In August 2023, Umbra Lab Inc. secured a significant SBIR Phase II contract valued at $1.25 million from AFWERX. This contract is focused on addressing critical challenges within the Department of the Air Force (DAF), specifically in the realm of space-based moving target indication (MTI). Umbra would harness its cutting-edge, cost-effective space systems, known for their wide-bandwidth capabilities and unique paired flight operation. Umbra’s goal is to develop and demonstrate maritime and ground-moving target indication capabilities.

• In August 2023, BlackSky Technology Inc. and Rocket Lab U.S., Inc. signed an agreement for five launches of BlackSky's satellites. This increased the capacity of BlackSky's constellation and introduced new capabilities. BlackSky's next-generation Gen-3 satellites were designed to produce images with up to 35-centimeter resolution.

• In July 2023, Spire Global, Inc. was selected by RDC Aviation to provide its customers with insights into global flight and aviation data. Spire delivered its flight report, which uses satellite and ground-based automatic dependent surveillance-broadcast (ADS-B) data to provide actionable metadata about flights, aircraft, and airlines. RDC would use Spire's data to analyze airport charges and navigation costs for its database of over 3,000 airports. This data would be used to help airlines and airports make informed decisions about pricing and operations.

Demand – Drivers, Challenges, and Opportunities

Market Drivers: Increasing Deployment of Artificial Intelligence Capabilities

Geospatial imagery analytics extensively employs artificial intelligence (AI) to efficiently tackle complex and crucial tasks, delivering high precision in tasks such as object detection, land cover classification, change detection, and environmental monitoring, among others. Machine learning, as a subset of AI, serves as the enabling technology that makes this level of accuracy attainable. Additionally, geospatial artificial intelligence (GeoAI), the fusion of spatial analytics and artificial intelligence, is a powerful approach used to gain insights from geospatial data, allowing for a deeper understanding and comprehensive analysis of such information. Companies such as Esri provide an ArcGIS platform that integrates spatial data with imagery from sources such as satellites, drones, or aircraft.

Market Challenges: Increasing Competition Due to Fragmented Market as a Result of Multiple Start-Ups

The geospatial market in the region is fragmented, and multiple key players such as Esri, Trimble Inc., Satellogic, Spire Global, and Planet Labs PBC are providing satellite imagery data and analytics solutions. Additionally, the region has several start-ups, such as Capella Space, Orbital Insight, and DroneDeploy, that have gained significant market presence. So, the presence of various geospatial players in the region increases the competition in the market and provides customers with more options, such as pricing, customization, and innovation in geospatial services.

Market Opportunities: Increasing Use of Geospatial Data to Create Sustainable Solutions

Geospatial technology serves as a valuable tool for promoting sustainable development and empowering policymakers and planners to make well-informed, evidence-based decisions that consider the long-term impacts on the environment, economy, and society. Machine learning methods and algorithms have greatly expanded the potential of geospatial technology in supporting sustainable development and surpassing expectations. Its cost-effective data acquisition across various spatial-temporal scales and information richness enhances the ability to analyze, process, and visualize scenarios, leading to deeper insights into the interconnected pillars of sustainability.

Analyst’s Thoughts

According to Nilopal Ojha, principal analyst at BIS Research, “The U.S. geospatial imagery analytics market is poised for significant growth in the coming years, driven by increasing demand from a wide range of industries, technological advancements, and government support. Key trends that are expected to shape the market include the rise of cloud-based geospatial analytics, the increasing use of AI and ML, and the growing adoption of geospatial imagery analytics for smart cities. For companies operating in the market, it is important to focus on developing cloud-based solutions that incorporate AI and ML and target the smart cities market. Additionally, companies should focus on developing innovative new applications for geospatial imagery analytics.”

Focus on Application and Solution - Analysis and Forecast, 2023-2033

Geospatial imagery analytics is a field of data analysis that focuses on extracting meaningful information and insights from various forms of geospatial imagery, which includes satellite images, aerial photographs, and remotely sensed data. This analysis involves the interpretation and processing of visual data to understand patterns, changes, and trends related to the Earth's surface and its features. The different types of solutions are data acquisition, data processing, analytics, and integrated delivery platforms.

The U.S. geospatial imagery analytics market has seen major key players such as BENTLEY SYSTEMS, INCORPORATED, BlackSky Technology Inc., Capella Space, DataCapable Inc., and Esri, which are capable of providing U.S. geospatial imagery analytics of diverse ranges. Key players are expanding their market presence by targeting new geographic regions and untapped markets to establish local offices, distribution networks, and partnerships to better serve customers and address specific regional needs.

New U.S. geospatial imagery analytics developers should focus on developing cutting-edge artificial intelligence and machine learning techniques for advanced image analysis, offering customized solutions tailored to specific industries, real-time capabilities, and integration with IoT and sensor data.

The following can be seen as some of the USPs of the report:

• Unique title capturing the U.S. geospatial imagery analytics market

• A dedicated section on growth opportunities and recommendations

• A qualitative and quantitative analysis of the U.S. geospatial imagery analytics market based on application and product

• Quantitative analysis

• Regional-level qualitative analysis of the U.S. geospatial imagery analytics market

• A detailed company profile comprising established players and some start-ups that are capable of significant growth with an analyst view

Companies developing geospatial imagery analytics systems should buy this report. Additionally, end users such as defense organizations should also buy this report to get insights about the U.S. geospatial imagery analytics demand and how they could benefit from it.

The global geospatial imagery analytics market is estimated to reach $32.78 billion in 2032...