Published Year: 2022

Global Prostate Cancer Testing Market - A Regional and Country Analysis: Focus on Test Type, Applica

In 2021, the global prostate cancer testing market was valued at $5,246.9 million, and it is...

Focus on Type of Biomarker, Application, End User, and Region - Analysis and Forecast, 2022-2030

U.S. Prostate Cancer Testing Market Industry Overview

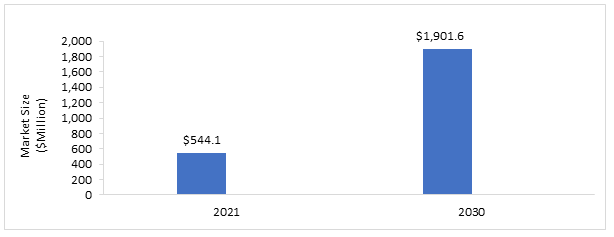

The U.S. prostate cancer testing market is anticipated to reach $1,901.6 million in 2030 from $544.1 million in 2021, with a CAGR of 14.7%, during the forecast period 2022-2030. The growth in the U.S. prostate cancer testing market is expected to be driven by high investments in the field of cancer research and the rising prevalence of prostate cancer in U.S. In addition, the focus of business leaders is establishing a deep understanding to address the unmet needs in clinical research to understand the prostate cancer market.

Market Lifecycle Stage

The U.S. prostate cancer testing market is in progressing phase. PSA screening or testing in a general population has increased the incidence of prostate cancer in recent decades. In addition, prostate cancer testing is essential in precision medicine because it assures the safe and successful use of tailored therapies. The majority of the companies in the U.S. prostate cancer testing market provide biomarker tests that are urine, blood, and tissue-based, as well as testing services. Furthermore, applications of prostate cancer testing are primarily clinical and research.

Figure: U.S. Prostate Cancer Testing Market Snapshot

Source: BIS Research Analysis

Impact

One of the main reasons for the expansion of the prostate cancer testing market in the upcoming years is the rise in prostate cancer cases. Prostate cancer is the second most frequent disease diagnosed in men, and its frequency is rising across the globe. Prostate cancer is thought to be diagnosed in one million additional cases worldwide each year. Due to an aging population, growing urbanization, and accompanying lifestyle changes, the overall incidence of prostate cancer has increased over the past few decades.

Impact of COVID-19

During the coronavirus disease 2019 (COVID-19) pandemic, a number of disease models issued warnings about an excess of cancer fatalities brought on by missed cancer screenings as a result of the general population's quarantine and a lack of healthcare resources. The COVID-19 pandemic has had a negative impact on early diagnosis in the specific case of prostate cancer, the second most common cancer in men, by reducing participation in screening programs and on time from diagnostic testing to surgery/radiotherapy, which may translate into a worse prostate-cancer-specific death rate in the coming years. Additionally, in other areas, including Florida, state governments disallowed non-essential healthcare services.

Significant reductions in cancer screenings were seen in the early stages of the COVID-19 pandemic. According to a research paper published in January 2022 by the University of Florida, screenings for prostate cancer were reduced by 74%. Due to these screening figures, there may have been thousands more cancer deaths in the U.S. than were registered.

For instance, prostate-specific antigen (PSA) testing rates and the identification of several urological malignancies, including prostate cancer, have been found to be declining in significantly afflicted populations. Several Australian urologists worry that men with possibly curable prostate cancer may have missed their chance for a cure due to low screening test uptake during the lockdowns of 2020. According to a research paper published by BMC Urology in June 2022, a total of 4,048,099 PSA tests and 118,328 prostate biopsies were performed in Australia over the six years of data analysis. In the years 2019 and 2020, 68,429 prostate magnetic resonance imaging (MRI) were performed. Between 2015 and 2019, there were, on average, 19,573 prostate biopsies and 678,082 PSA testing performed per year.

Market Segmentation:

Segmentation 1: by Biomarker Type

• Initial Evaluation: Prostate-Specific Antigen (Total PSA, Free PSA)

• Pre-Biopsy/Post-Negative Biopsy Testing

• Post-Biopsy Tissue Testing

Based on biomarker type, the pre-biopsy test in the U.S. prostate cancer testing market is expected to be dominated by the biomarker type segment. This is due to the increasing popularity of prostate cancer testing and rising awareness related to prostate cancer testing.

Segmentation 2: by Application

• Diagnostics Biomarkers

• Prognostics Biomarkers

Based on application, the U.S. prostate cancer testing market is dominated by the diagnostics biomarkers segment owing to the rising R&D activity focused on the development of prostate cancer testing. The diagnosis of prostate cancer has developed a new molecular-based diagnostics technology. To detect clinically relevant cancer upon diagnosis, several tools or therapeutic options are required to improve the patient’s quality of life.

Segmentation 3: by End User

• Cancer Research Institutes

• Diagnostic Laboratories

• Hospitals and Clinics

• Ambulatory Surgical Center (ASCs)

• Others

As of 2021, the U.S. prostate cancer testing market (by end user) was dominated by ambulatory surgical centers (ASCs), holding a 28.55% market share with a market value of $155.3 million.

Segmentation 4: by Region

• Northeast U.S.

• Midwest U.S

• South U.S.

• West U.S.

The TAM of the pre-biopsy/post-negative biopsy testing segment is expected to grow at a CAGR of 4.5% during the forecast period 2022-2030 in the South U.S. prostate cancer testing market. Several established diagnostics manufacturers in this region who are focusing on expanding their portfolios in prostate cancer testing and are collaborating with service providers and pharmaceutical giants to co-market prostate cancer testing solutions with its complementary precision medicine solutions. Moreover, the U.S. government is currently undertaking several initiatives to develop tests for cancer and provide funds to new start-ups in the cancer diagnostics field.

Recent Developments in the U.S. Prostate Cancer Testing Market

• In September 2022, Veracyte, Inc. announced the publishing of data in the Journal of the National Cancer Institute to demonstrate the company’s decipher prostate genomic classifier may help identify African American men with early, localized prostate cancer who are most likely to harbor more aggressive disease.

• In August 2019, BioReference Laboratories, Inc. announced the selection by The IPA Association of America (TIPAAA) as its provider of laboratory services and to assist with data analytics for its members’ patients. The agreement is designed to enhance patient care and offers collaborative health management tools to TIPAAA members, which includes more than 667 medical organizations in 39 states. The members can have convenient access to BioReference’s comprehensive laboratory testing menu, including routine and specialty tests, as well as the 4Kscore for detecting aggressive prostate cancer.

• In June 2021, Thermo Fisher Scientific announced submissions open for the Oncomine Clinical Research Grant program to support clinical research projects in oncology. The grant aims to provide funding for high-quality molecular profiling studies focusing on the impact of immune-based treatments for cancer patients.

Demand - Drivers and Limitations

The following are the demand drivers for the U.S. prostate cancer testing market:

• Rising Prevalence of Prostate Cancer in the U.S.

• Increasing Number of Prostate Cancer Screening and Testing

• Government Initiatives Related to Prostate Cancer

The market is expected to face some limitations due to the following challenges:

• High Probability of False Positives during Prostate Cancer Testing

• Clinical Gaps Related to Prostate Cancer Testing

Analyst View

According to Nitish Kumar, Principal Analyst, BIS Research, “Prostate cancer testing includes various tests being followed for past several years. The treatment starts with the prostate cancer screening that includes preliminary tests, i.e., prostate-specific antigen test and digital rectal exam (DRE). If prostate cancer is suspected based on the results of screening tests or symptoms and an elevated PSA test, the patient is referred to a urologist. To determine whether cancer has spread beyond the prostate, the following testing is undertaken, i.e., pre-biopsy test (biomarker test which is blood-based and urine-based biomarker) and imaging (mp-MRI (Multi-parametric Magnetic Resonance Imaging)), prostate biopsy, and post-biopsy procedures such as tissue-based biopsy”.

Focus on Type of Biomarker, Application, End User, and Region - Analysis and Forecast, 2022-2030

Tests for prostate cancer are crucial for the early diagnosis and effective treatment of the condition. The most frequent initial diagnosis for prostate cancer is prostate-specific antigen (PSA) testing, which may or may not need follow-up tests to confirm the tumor's presence. The use of prostate cancer testing offers a number of advantages, including aiding in the early discovery of the disease at localized stages and assisting individuals in achieving effective health management. The usage of prostate cancer testing is on the rise all around the world, but it is more prevalent in developing nations with rising healthcare standards.

PSA screening or testing in a general population has increased the incidence of prostate cancer in recent decades. In addition, prostate cancer testing is essential in precision medicine because it assures the safe and successful use of tailored therapies. The majority of the companies in the U.S. prostate cancer testing market provide biomarker tests that are urine, blood, and tissue-based, as well as testing services. Furthermore, applications of prostate cancer testing are primarily clinical and research.

There are high investments in the field of cancer research driven by top-line revenue growth. Business leaders are establishing a deep understanding to address the unmet needs in clinical research to understand the prostate cancer market. One of the major developments in the market for prostate cancer testing is the increased emphasis on biomarker research. With the recent advancements in high throughput technological platforms in proteomics, genomics, and immunology, the discovery of biomarkers has quickened. The producers are concentrating on creating prostate cancer biomarkers that can predict the severity of the disease and guide in making better treatment choices.

The U.S. prostate cancer testing market is currently witnessing several developments, primarily aimed toward bringing new products and services. Major manufacturers of prostate cancer testing products, along with the service providers, are actively undertaking significant business strategies to translate success in research and development into the commercial clinical setting. Companies such as mdxhealth, Danaher., Bio-Techne, Veracyte, Inc., OPKO Health, Inc., and Cleaveland Diagnostics. have majorly adopted partnerships, collaborations, and joint venture strategies.

A new entrant can focus on various prostate cancer testing offerings by the established players in the prostate cancer testing market. The market is fragmented with established market leaders such as mdxhealth, Danaher, Bio-Techne, Veracyte, Inc., and OPKO Health, Inc., who have had their presence in the market for the past many years. The new entrants can focus on their strategy of product launch and expansion for prostate cancer testing.

The following can be considered the USPs of the report:

• Extensive competitive benchmarking of the top 20 players to offer a holistic view of the U.S. prostate cancer testing market landscape

• Market ranking analysis based on product portfolio, recent developments, and regional spread

• Investment landscape, including product adoption scenario, funding, and patent analysis

The companies manufacturing prostate cancer testing, service providers, pharmaceutical companies, research institutions, etc., should buy this report.

In 2021, the global prostate cancer testing market was valued at $5,246.9 million, and it is...

The report focuses solely on the extensive stage small cell lung cancer treatment, which...

The U.S. solid tumor testing market is projected to reach $18,287.6 million by 2032 from...

The lung cancer genomic testing medicine market was valued at $1,262.0 million in 2020 and is...