Published Year: 2021

Global Solid Tumor Testing Market: Focus on Technology, Cancer Type, Application, End User, and Comp

The global solid tumor testing market is projected to reach $40,660.6 million by 2030 from...

Focus on Technology, Cancer Type, Type of Biomarker, By Application, by End User, and Region - Analysis and Forecast, 2022-2032

Delivery Time: 1-5 Working Days

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know MoreU.S. Solid Tumor Testing Market Industry Overview

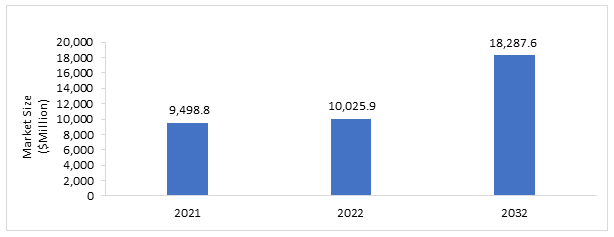

The U.S. solid tumor testing market was estimated to be at $9,498.8 million in 2021, which is expected to grow with a CAGR of 6.19% during the forecast period 2022-2032 and reach $18,287.6 million by 2032. The growth in the U.S. solid tumor testing market is expected to be driven by increasing awareness of early tumor diagnosis and tests along with the increasing geriatric population. Furthermore, increasing cancer incidences in the pediatric population.

Market Lifecycle Stage

The U.S. solid tumor testing market is progressing rapidly. Significant increases in the research and development activities pertaining to solid tumor testing are underway to develop better testing kits and assays, which are expected to increase due to the rising frequency and efficiency of cancer testing products. The recent allocation of $6.44 billion to NCI in FY2019, as per the Department of Health and Human Services Appropriations Act and the 21st Century Cures Act, has further brightened the prospects for key players to bring a diagnostic or therapeutic innovation to the market with conditional support (pertaining to innovation or diagnostic/therapeutic breakthrough and a relative grant triggered from NCI).

Figure: U.S. Solid Tumor Testing Market

Source: BIS Research Analysis

Impact

• The presence of major service providers of solid tumor testing in the U.S. has a major impact on the market. For instance, Illumina, Inc. acquired GRAIL which is a cancer detection healthcare company. With this acquisition, Illumina, Inc. can accelerate the adoption of this lifesaving Galleri blood test worldwide which is known to detect 50 different cancer types.

• Companies such as QIAGEN partnered with PGDx for molecular cancer testing. With the help of this, laboratories will be able to receive standardized reporting from QIAGEN and receive access to QIAGEN’s QCI Interpret One for rapid next-generation sequencing tests.

Impact of COVID-19

It is known that people with cancer are more susceptible to infectious agents due to their impaired immune systems. However, this was found inconsistent with COVID-19. The very early studies found that people with cancer are more susceptible to COVID-19 and its severe complications, especially for patients with lung or hematological cancers. However, some of the most recent, larger studies found no increased risk of death due to cancer type or timing of cancer treatment.

There were numerous consequences due to the COVID-19 pandemic, especially because of the reduced access to care for other illnesses. As the number of individuals becoming ill from COVID-19 kept increasing and for the protection of healthy individuals from being affected by the disease, all non-urgent healthcare facilities were suspended in the U.S. by the recommendation of the American Cancer Society and other organizations. Even though these measures were necessary, they led to delays in cancer diagnosis, screening, and treatment. This led to increased later-stage cancer diagnoses and, in turn, cancer deaths that may have been preventable.

Market Segmentation:

Segmentation 1: by Technology

• Next-Generation Sequencing

• Polymerase Chain Reaction

• Fluorescence In-Situ Hybridization

• Immunohistochemistry

• Liquid Chromatography/Mass Spectrometry

• Other Technologies

Based on technology, the U.S. solid tumor testing market is expected to be dominated by the next-generation sequencing technology. This is due to the high accuracy and efficiency of next-generation sequencing techniques.

Segmentation 2: by Cancer Type

• Breast Cancer

• Prostate Cancer

• Colorectal Cancer

• Lung Cancer

• Melanoma

• Endometrial Cancer

• Lymphoma

• Thyroid Cancer

• Brain Cancer

• Other Cancer Types

Based on cancer type, the U.S. solid tumor testing market is dominated by breast cancer, owing to an increasing number of patients suffering from breast cancer and also more awareness and better diagnosis of cancer.

Segmentation 3: by Type of Biomarker

• Genetic Biomarker

o Molecular Biomarker

o Cellular Biomarker

o Imaging Biomarker

• Protein Biomarker

o Predisposition Biomarker

o Diagnostic Biomarker

o Prognostic Biomarker

o Predictive Biomarker

The genetic biomarkers segment dominates the U.S. solid tumor testing market; however, the protein biomarkers segment shows the largest CAGR of 6.61%. The growth in this segment is mainly due to the growth in research and development, which is leading to the discovery of more biomarkers.

Segmentation 4: by Application

• Clinical

o Diagnostics

o Treatment and Monitoring

o Screening

o Prognosis

• Research

o Biomarker Discovery

o Personalized Medicine

The clinical application dominated the application segment. This is because the solid tumor testing market is already well established with many clinical applications. However, the research segment has a higher CAGR of 6.61% as compared to 5.92% for clinical and is expected to grow at a fast pace during the forecast period. Research has increased due to the emergence of personalized medicine.

Segmentation 5: by End User

• Hospitals

• Pharmaceutical and Biotechnology Companies

• Contract Research Organizations

• Academic Research Institutions

• Other End Users

Hospitals dominated the end-user segment. This is due to an increasing number of oncologists playing a key role in the recommendation and data interpretation of solid tumor tests. Due to this, most tests are performed through the hospitals, thereby making it a dominating segment of the market and its growth.

Segmentation 6: by Region

• The Southern U.S.

• The Midwest U.S.

• The Mid-Atlantic U.S.

• The West U.S.

• The Southwest U.S.

• New England

The Southern U.S. dominated the regions with a revenue of $2,614.7 in 2021. The high incidence of cancer in a few states like California, Florida, and Texas are the key areas for solid tumor testing market growth.

Recent Developments in U.S. Solid Tumor Testing Market

• In December 2021, Opko Health, Inc. secured FDA approval for its 4Kscore test that is approved for men 45 years or older who haven’t had a prior prostate biopsy or are biopsy negative.

• In April 2021, NeoGenomics Laboratories. launched biomarker assist KRAS single gene test. This test is used for advanced or metastatic small cell lung cancer patients.

• In November 2020, NeoGenomics Laboratories. started mobile phlebotomy services for liquid biopsy tests. These tests include InVisionFirst-Lung, which is a non-small cell lung liquid biopsy test, and the NeoLab liquid biopsy test, which is used for all solid tumors and hematological cancers.

• In February 2020, QIAGEN obtained a CE mark for its therascreen PIK3CA mutation assay. This test can be used to identify breast cancer.

Demand – Drivers and Limitations

Following are the demand drivers for the U.S. solid tumor testing market

• Rising Advancements in Solid Tumor Testing and Rapid Usage of Liquid Biopsy

• Early Cancer Detection with Multi-Cancer Tests

• Increasing Adoption of Inorganic Growth Strategies in the Market

• Spike Increase in the Research Funding from National Cancer Institute

• Rapid Adoption of Genetic Testing

The market is expected to face some limitations too due to the following challenges:

• Reimbursement Cuts in the U.S.

• High Pricing Pressure

Analyst Thoughts

According to Nitish Kumar, Principal Analyst, BIS Research, “U.S. solid tumor testing market is a well-established market and is expected to grow further in the coming years due to the continuous increase in awareness and need of cancer testing in the U.S.”

Focus on Technology, Cancer Type, Type of Biomarker, By Application, by End User, and Region - Analysis and Forecast, 2022-2032

The global solid tumor testing market is projected to reach $40,660.6 million by 2030 from...