Coagulation factor deficiency is a group of rare blood disorders where the body lacks essential clotting proteins, leading to prolonged bleeding. The most well-known types are Hemophilia A (Factor VIII deficiency), Hemophilia B (Factor IX deficiency), and von Willebrand Disease. These disorders can be inherited or acquired due to conditions like liver disease. Historically, treatment relied on regular infusions of clotting factor concentrates, but modern science is rapidly transforming the landscape with long-acting biologics, non-factor therapies, and gene therapy.

According to BIS Research, the global coagulation factor deficiency market is valued at $13.62 billion and is set to grow significantly in the next 10 years.

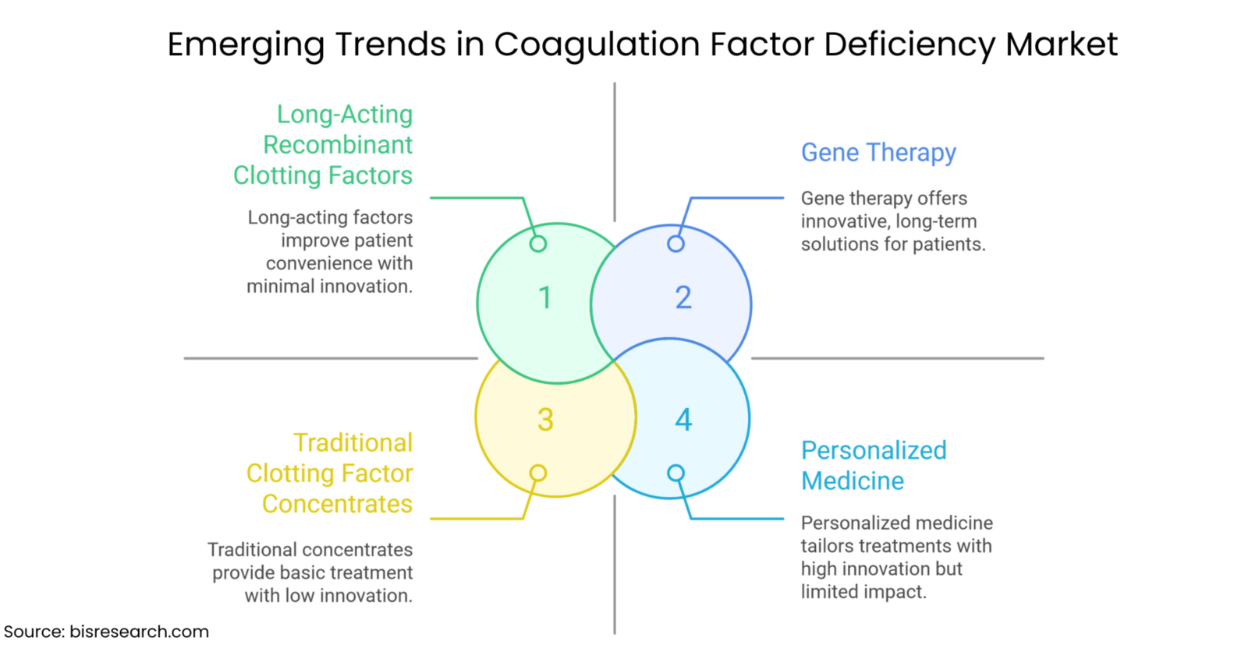

By 2025, treatment for coagulation factor deficiency has evolved from reactive management to proactive, life-enhancing therapies. Traditional plasma-derived infusions have been replaced by recombinant clotting factors engineered for extended half-life. These long-acting factor VIII and IX therapies reduce the frequency of injections and improve adherence.

One major milestone was the FDA approval of Altuviiio (efanesoctocog alfa) in 2023, a novel Factor VIII replacement that bypasses limitations imposed by von Willebrand factor. Patients now experience stable clotting protection for up to a week, drastically reducing bleeding episodes.

Another leap forward is non-factor therapy. For example, Hemlibra (emicizumab), a bispecific antibody mimicking Factor VIII, has revolutionized Hemophilia A care. Administered subcutaneously, it provides steady prophylaxis, even in patients with inhibitors—and shifts severe hemophilia into a manageable condition.

Emerging approaches like RNA interference (RNAi) and anti-TFPI antibodies (e.g., fitusiran, concizumab) are reshaping the field. Rather than replace missing factors, they rebalance the coagulation system, opening doors for patients with poor response to traditional treatment.

Discover BIS Research Surgical Procedure Volume Database – your key to real-world, country-level procedural insights across MedTech.

The defining development is the arrival of gene therapy for hemophilia. In 2022, Hemgenix (etranacogene dezaparvovec) became the first FDA-approved gene therapy for Hemophilia B, enabling patients to produce their own Factor IX after a single infusion. Trials showed 96% of patients discontinued regular prophylaxis and sustained FIX levels over 40%.

In 2023, Roctavian (valoctocogene roxaparvovec) was approved for Hemophilia A. Over 70% of patients treated experienced zero bleeds for a year post-infusion. While the price tags (up to $3.5 million per dose) raise access concerns, the long-term cost savings and lifestyle improvements support their viability.

Meanwhile, next-generation biologics continue gaining ground. Therapies like Mim8 and NXT007 aim to outperform Hemlibra with more potent Factor VIII mimetics. RNAi drugs like fitusiran, which lower antithrombin levels, show promise in boosting natural thrombin production and reducing bleeds.

Get to Know More About Market Trends and Growth Download Sample Report Here

The coagulation factor deficiency landscape in 2025 is shaped by a mix of established pharmaceutical leaders and agile biotech startups. Industry giants like Roche (with its groundbreaking bispecific antibody Hemlibra), Novo Nordisk (developing novel anti-TFPI therapies), Pfizer (advancing gene therapy for hemophilia B), Sanofi and Sobi (creators of Altuviiio), and Takeda (a long-time provider of plasma-derived clotting factor concentrates) dominate the global market. At the same time, biotech innovators are redefining bleeding disorder treatment. BioMarin launched the first Hemophilia A gene therapy (Roctavian), while UniQure and CSL Behring brought Hemgenix for Hemophilia B to market. Spark Therapeutics, now part of Roche, remains at the forefront of gene therapy platforms. New-generation disruptors like Alnylam Pharmaceuticals (pioneering RNAi-based hemophilia drugs) and Sangamo Therapeutics (exploring gene-editing technologies) are rapidly pushing boundaries.

Niche-focused startups such as Hemab Therapeutics are also gaining attention for developing prophylactic therapies for rare bleeding disorders like Factor VII deficiency and Glanzmann thrombasthenia—offering transformative options for previously neglected patients. Together, these companies are accelerating the shift toward safer, more durable, and more accessible therapies for coagulation factor deficiency.

Explore More Insights on Healthcare Industry

The goal for 2025 and beyond is clear: curative or near-curative treatment that allows patients to live bleed-free lives without constant monitoring or infusions. Gene therapies, rebalancing agents, and subcutaneous prophylactics are rewriting the rules.

We are entering an era where bleeding disorders are no longer a life-limiting condition. The field is rapidly converging on durability, accessibility, and personalization, with innovations tailored to patient needs and lifestyles.

Looking to enter a new market but unsure where to start? At BIS Research, we provide first-hand insights directly from key opinion leaders (KOLs), backed by rigorous primary and secondary research. Whether you're exploring opportunities in product type, region or deficiency type in the coagulation factor deficiency market, our segmentation-driven approach helps you tap into real market growth potential. Our strategic intelligence empowers you to make informed, confident decisions—from product positioning to pricing and regulatory planning.