Published Year: 2026

AI-Enabled Medical Imaging Solutions Market - A Global and Regional Analysis: Focus on Modality, Pro

The global AI-enabled medical imaging solutions market is projected to reach $18,041.3 million...

Type, Technology, End User, and Regional Analysis - Analysis and Forecast, 2026-2036

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

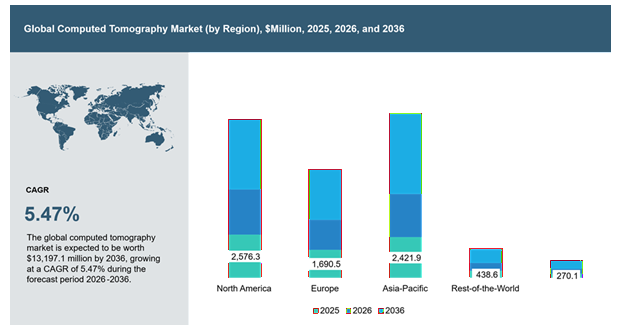

Get Subscription Know MoreThe global computed tomography market, initially valued at $7,397.4 million in 2025, is projected to witness substantial growth, surging to $13,197.1 million by 2036, marking a remarkable compound annual growth rate (CAGR) of 5.47% over the period from 2026 to 2036.

The global computed tomography market is witnessing robust growth, driven by the increasing demand for faster, more accurate, and scalable diagnostic imaging amid rising patient volumes and growing pressure on radiology workflows. Computed tomography has become a critical imaging modality across healthcare systems, particularly in emergency care, oncology, cardiology, and neurology, where rapid and precise cross-sectional imaging is essential for clinical decision-making. The rising burden of chronic diseases, along with increasing CT scan volumes and expanding use in acute and preventive care pathways, is further strengthening the role of CT across hospitals and diagnostic imaging centers. The integration of artificial intelligence into CT workflows is transforming conventional imaging by enabling advanced image reconstruction, automated detection, workflow prioritization, and clinical decision support. CT systems are particularly valuable in high-volume and time-sensitive settings such as trauma care, stroke evaluation, and cancer diagnosis, where rapid triage and accurate interpretation are critical. As healthcare systems shift toward value-based care and operational efficiency, the adoption of advanced CT technologies is accelerating to improve diagnostic consistency, reduce turnaround times, and optimize resource utilization.

Technological advancements in imaging hardware and computational algorithms are significantly enhancing CT capabilities. Innovations such as multi-slice and dual-source systems, spectral imaging, photon-counting detectors, and AI-enabled reconstruction are improving image quality, enabling better tissue characterization, and reducing radiation dose. In addition, the integration of CT systems with digital health infrastructure, including PACS, RIS, and cloud-based platforms, is enabling scalable deployment across multi-site healthcare networks and supporting seamless data sharing and remote diagnostics. The growing emphasis on enterprise imaging and integrated workflow solutions is further driving the transition from standalone imaging systems to connected, workflow-centric platforms. However, the market continues to face challenges, including high capital investment and lifecycle costs, radiation exposure concerns, regulatory complexities, and interoperability issues. Despite these challenges, increasing investments in healthcare infrastructure, expansion of diagnostic imaging networks, and strategic collaborations among imaging vendors and technology providers are expected to drive sustained growth and innovation in the computed tomography market.

Market Introduction

The global computed tomography (CT) market has undergone a notable transformation, driven by continuous technological advancements and increasing integration of artificial intelligence into imaging workflows. Companies are progressively embedding AI-enabled capabilities into CT systems to enhance image reconstruction, automate detection, and improve workflow efficiency. These innovations support a wide range of clinical applications, including oncology, cardiology, neurology, and emergency imaging, enabling faster, more accurate, and standardized diagnostic outcomes.

Key advancements, such as spectral imaging, photon-counting CT, high-slice systems, and AI-driven reconstruction algorithms, highlight the industry’s focus on improving image quality, reducing radiation dose, and increasing diagnostic precision. Additionally, the integration of CT systems with enterprise imaging platforms, including PACS, RIS, and cloud-based solutions, is enhancing interoperability, data sharing, and clinical decision support across healthcare settings.

The growing demand for rapid diagnostics, rising imaging volumes, and increasing focus on early disease detection are further accelerating CT adoption across both developed and emerging markets. As healthcare systems continue to prioritize efficiency, accuracy, and patient outcomes, ongoing innovations in computed tomography are expected to play a critical role in shaping the future of diagnostic imaging and clinical workflows.

Global Computed Tomography Market (by Region), $Million, 2025, 2026, and 2036

Industrial Impact

The global computed tomography (CT) market has witnessed substantial growth, driven by the increasing demand for high-accuracy diagnostic imaging, rising imaging volumes, and the need for efficient and scalable radiology workflows. Key players such as Canon Inc., Carestream Health Inc., Siemens Healthineers AG, FUJIFILM Holdings Corporation, GE HealthCare, Koninklijke Philips N.V., Koning Health, NeuroLogica Corp., Neusoft Corporation, Shenzhen Anke High-tech Co., Ltd., Shanghai United Imaging Healthcare Co., Ltd., Planmed Oy, VATECH, and Xoran Technologies are playing a pivotal role in advancing CT technologies through continuous innovation and strategic investments.

These companies are actively focusing on the development and integration of advanced technologies, including AI-enabled imaging, spectral and photon-counting CT, and low-dose systems, which are transforming diagnostic capabilities and accelerating technology upgrade cycles, particularly in mature markets. Such innovations are enhancing image quality, improving diagnostic confidence, and enabling more precise disease detection across clinical areas such as oncology, cardiology, and neurology.

At the same time, increasing demand from emerging markets is encouraging manufacturers to develop cost-effective, scalable, and modular CT systems tailored to resource-constrained settings, thereby expanding access to advanced imaging. Strategic collaborations between imaging companies, AI solution providers, and healthcare institutions are further supporting innovation and market expansion.

Additionally, the integration of CT systems with digital health infrastructure, including PACS, RIS, and cloud-based platforms, is improving workflow efficiency, enabling remote diagnostics, and supporting data-driven clinical decision-making. Overall, CT systems are enhancing diagnostic accuracy, reducing turnaround times, and improving patient outcomes, while also driving broader transformation across the medical imaging and healthcare ecosystem.

Market Segmentation

Segmentation 1: By Type

• Stationary CT Scanners

• Portable CT Scanners

Stationary CT Scanners to Dominate the Computed Tomography Market (by Type)

In terms of type, the stationary CT scanners segment is expected to lead the computed tomography market, accounting for a significant share due to its widespread deployment across hospitals and diagnostic imaging centers. These systems offer advanced imaging capabilities, including high-slice configurations, faster scan speeds, and broader clinical applications such as cardiology, oncology, and trauma care. Their ability to support high patient throughput and seamless integration with hospital IT systems further reinforces their market dominance.

Segmentation 2: By Technology

• High-Slice CT

• Mid-Slice CT

• Low-Slice CT

• Cone Beam CT

High-Slice CT to Dominate the Computed Tomography Market (by Technology)

In terms of technology, high-slice CT is expected to lead the global computed tomography market, driven by its advanced imaging capabilities, faster scan speeds, and superior diagnostic accuracy. These systems are widely adopted in developed healthcare settings for complex applications such as cardiology, oncology, and trauma imaging, where precision and speed are critical. Their ability to support high patient throughput and integrate with advanced software solutions further strengthens their adoption across high-volume clinical environments.

Segmentation 3: By End User

• Hospitals and Ambulatory Surgery Centers

• Diagnostic Centers

• Others

Hospitals and Ambulatory Surgery Centers to Dominate the Computed Tomography Market (by End User)

In terms of end users, hospitals and ambulatory surgery centers are expected to lead the global computed tomography market, growing at a CAGR of 4.89%, driven by their high patient volumes, comprehensive care capabilities, and access to advanced imaging infrastructure. These facilities typically handle complex and emergency cases, requiring high-performance CT systems for applications such as trauma, oncology, and cardiovascular imaging. Additionally, strong capital budgets and integration with hospital IT systems further support the dominance of this segment.

Segmentation 4: By Region

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Rest-of-Europe

• Asia-Pacific

o China

o Japan

o India

o Australia

o South Korea

o Rest-of-Asia-Pacific

• Latin America

o Brazil

o Mexico

o Rest-of-Latin America

• Middle East and Africa

o Turkey

o Israel

o Rest-of-Middle East and Africa

North America to Dominate the Computed Tomography Market (by Region)

North America is expected to lead the global computed tomography market, supported by a highly mature U.S. market and a relatively capacity-constrained Canadian market. The U.S. benefits from a high installed base, strong replacement cycles, and advanced imaging infrastructure, positioning it among the most CT-intensive markets globally, while Canada operates with comparatively lower scanner availability and more centralized infrastructure, creating opportunities for capacity expansion and improved access.

The region also benefits from widespread integration of electronic health records (EHRs), PACS, and RIS systems, enabling efficient workflow management, seamless image sharing, and effective adoption of advanced CT technologies across hospitals and diagnostic imaging centers. Utilization levels remain consistently high, with strong procedural volumes across emergency, inpatient, and outpatient settings in the U.S., and high-efficiency system usage in Canada despite infrastructure limitations.

Recent Developments in the Computed Tomography Market

• In Jan 2026, Planmed Oy announced that its Planmed Verity XFI weight-bearing CT scanner received CE marking under the European Union Medical Device Regulation (EU MDR).

• In May 2025, FUJIFILM Corporation received FDA 510(k) clearance for an updated version of the SCENARIA View CT system, incorporating advanced workflow and automation enhancements. Key updates include AutoPose, an AI-based positioning tool that automatically identifies anatomical regions from localization images and sets optimal scan and reconstruction ranges, and RemoteRecon, which enables reconstruction parameter processing on an external workstation connected to the CT system.

• In June 2024, FUJIFILM Corporation launched FCT iStream, a compact 128-slice CT system, and said it was designed for the hospital and outpatient market. The company highlighted four proprietary technologies-HiMAR Plus, Intelli IPV, SynergyDrive, and IntelliODM to improve image sharpness, streamline workflow through AI automation, and reduce patient dose.

Demand – Drivers, Challenges, and Opportunities

Market Drivers

Rising Disease Burden and Increasing CT Scan Volumes Driving Demand for CT Scanners: The global demand for computed tomography (CT) scanners is strongly driven by the rising burden of chronic diseases and the corresponding increase in CT scan volumes across healthcare systems. According to the World Health Organization, nearly 20 million new cancer cases were reported in 2022, with projections expected to reach approximately 35 million by 2050, highlighting the growing need for advanced diagnostic imaging. CT plays a critical role in early detection, staging, and monitoring across oncology, cardiology, neurology, and emergency care, particularly as cardiovascular diseases remain the leading cause of global mortality. The expansion of emergency and trauma care services is further increasing CT utilization, given its importance in rapid clinical decision-making. At the same time, advancements in multi-slice CT systems, faster acquisition speeds, and improved image quality are enabling higher patient throughput, supporting increased scan volumes. The integration of CT into routine clinical workflows, including preventive screening programs such as low-dose CT for lung cancer, is also driving repeat imaging and longitudinal monitoring. Additionally, demographic factors such as aging populations and urbanization, along with improving healthcare infrastructure in emerging markets, are expanding access and utilization, collectively reinforcing sustained demand for high-performance CT systems globally.

Market Restraints

High Capital Investment and Lifecycle Costs Associated with CT Systems: The high capital investment and ongoing lifecycle costs associated with computed tomography (CT) systems remain a major restraint to market adoption, particularly in cost-sensitive healthcare settings. CT scanners require significant upfront investment, typically ranging from approximately $285,000–$360,000 for 16-slice systems to over $1.3 million–$2.1 million for advanced 256+ slice configurations, in addition to substantial installation costs related to site preparation, radiation shielding, cooling systems, and infrastructure upgrades. Beyond acquisition, recurring expenses such as annual service contracts, often between $70,000 and $150,000, along with costs for maintenance, component replacements (e.g., X-ray tubes and detectors), and software upgrades, further increase the total cost of ownership. Rapid technological advancements, including AI integration, spectral imaging, and dose optimization features, are also shortening upgrade cycles, compelling providers to invest in newer systems to remain competitive. Additionally, ongoing regulatory compliance, quality assurance, and certification requirements add to operational expenditures, collectively creating financial constraints that can delay procurement decisions and limit adoption, especially in emerging markets.

Market Opportunities

Expansion of CT Access in Emerging and Underserved Markets: A significant opportunity in the computed tomography (CT) market lies in expanding access across emerging and underserved regions, where imaging infrastructure remains limited. Many low- and middle-income countries continue to face gaps in the availability of CT systems, leading to delayed diagnosis and treatment of critical conditions such as cancer, cardiovascular diseases, and trauma. Improving access to CT imaging in these regions can significantly enhance early detection, clinical outcomes, and overall healthcare efficiency. This opportunity is further supported by increasing healthcare investments, government initiatives, and efforts to strengthen diagnostic capabilities across Asia-Pacific, the Middle East, and Africa. Vendors that offer cost-effective systems, mobile CT solutions, and flexible service models are well-positioned to address these unmet needs and capture growth in these high-potential markets.

Analyst’s Thoughts

According to Priyanshi Upadhyay, Research Analyst – BIS Research, “The computed tomography market is poised for significant growth, driven by the rising demand for advanced diagnostic imaging, increasing prevalence of chronic diseases such as cancer and cardiovascular disorders, and continuous technological advancements in CT systems. As healthcare systems increasingly prioritize early and accurate diagnosis, CT imaging is becoming a critical tool in clinical decision-making across emergency care, oncology, and cardiology. The integration of artificial intelligence, low-dose imaging technologies, and innovations such as spectral and photon-counting CT is expected to transform imaging capabilities by improving diagnostic accuracy, enhancing workflow efficiency, and reducing radiation exposure. These advancements are enabling faster image acquisition, improved tissue characterization, and more precise disease detection.

With ongoing investments in research and development, expansion of healthcare infrastructure, and growing adoption in emerging markets, the computed tomography market presents strong opportunities for innovation and global expansion, particularly as providers focus on improving patient outcomes and operational efficiency.”

Type, Technology, End User, and Regional Analysis - Analysis and Forecast, 2026-2036

Ans: Computed tomography (CT) is an advanced medical imaging technique that uses X-rays and computer processing to create detailed cross-sectional images of the body. It enables healthcare professionals to visualize internal structures such as bones, organs, blood vessels, and tissues with high precision.

Ans: To strengthen their position in the computed tomography market, companies are adopting several strategic initiatives. These include the integration of artificial intelligence (AI) to enhance image analysis, improve workflow efficiency, and enable predictive diagnostics. Companies are also focusing on the development of low-dose CT systems to reduce radiation exposure while maintaining high image quality.

Ans: The following are the USPs of this report:

• Market regulations and key trends in the computed tomography market

• Market dynamic analysis of the opportunities, trends, and challenges in the market

Ans: This report is valuable for medical imaging device manufacturers, hospitals, diagnostic imaging centers, research institutions, radiology labs, and healthcare IT and AI solution providers involved in the development and implementation of computed tomography technologies. It will also benefit pharmaceutical and biotech companies leveraging imaging-based diagnostics, as well as investors, policymakers, and healthcare consultants interested in understanding market trends and opportunities for technological innovation, market expansion, and strategic collaboration.

The global AI-enabled medical imaging solutions market is projected to reach $18,041.3 million...

The global spine X-ray and computed tomography market was valued at $916.0 million in 2020 and...