Published Year: 2025

Data Center Power Distribution Units and Power Supply Units Market - A Global and Regional Analysis

The global data center PDUs and PSUs market is projected to reach $73,376.5 million by 2035...

Focus on Data Center Type, Application, Power Architecture, Distribution, Power Supply, Component and Region - Analysis and Forecast, 2025-2035

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

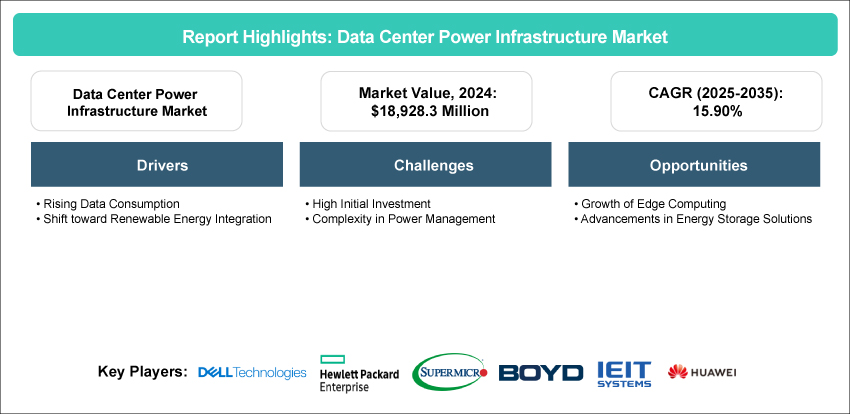

The data center power infrastructure market was valued at $18,928.3 million in 2024 and is projected to reach $101,901.4 million by 2035, growing at a CAGR of 15.90%. The increasing demand for cloud computing, artificial intelligence (AI), and data storage solutions has been driving this market growth. As industries continue digitizing, the need for robust, scalable, and energy-efficient data center power infrastructure market has expanded rapidly. Additionally, the rising focus on sustainability, energy efficiency, and the integration of renewable energy sources in data centers has been further contributing to the data center power infrastructure market's growth. Innovations in power management, such as intelligent power distribution units (PDUs), are also expected to play a key role in meeting the growing power demands of modern data centers.

Market Introduction

The data center power infrastructure market focuses on developing and deploying advanced power solutions to meet the growing demand for digital services, cloud computing, and data storage. Data center power infrastructure market has been driven by the increasing need for efficient, scalable, and reliable power systems as data centers become central to the global digital economy. Key components are essential to ensure seamless operations while minimizing energy consumption. As the industry moves toward sustainability, there is a significant emphasis on integrating renewable energy sources, improving power efficiency, and optimizing energy management to meet both operational demands and environmental goals. The growing adoption of digital technologies and the expansion of AI, big data, and IoT further drive the need for robust and sustainable power infrastructure in data centers worldwide.

Industrial Impact

The industrial impact of the data center power infrastructure market is significant across multiple sectors, such as technology, telecommunications, and energy. As data centers expand to support the increasing demand for cloud services, artificial intelligence, and data storage, the need for reliable, scalable, and efficient power infrastructure becomes essential. The data center power infrastructure market is driving advancements in power distribution systems and electrical components to ensure continuous and optimized power delivery, thereby supporting the uninterrupted operation of critical data services. As digital ecosystems evolve, the demand for power infrastructure that can handle higher loads while reducing energy consumption has been reshaping operational practices. The growth in data center power infrastructure has been promoting innovation in power management, improving operational efficiency, and ensuring that businesses meet the rising energy demands of modern data-intensive applications.

The companies involved in the data center power infrastructure market include key industry players such as Dell Inc., Hewlett Packard Enterprise Development LP, Super Micro Computer, Inc., Boyd, IEIT SYSTEMS CO., LTD., Huawei Technologies Co., Ltd., Cisco Systems, Inc., Schneider Electric, Vertiv Group Corp., Eaton, Rittal Pvt. Ltd., NetApp, Arista Networks, Inc., Modine, and Mitsubishi Electric Corporation. These companies have been enhancing their capabilities through strategic partnerships, technological innovations, and investments in research and development. Their continuous focus on providing reliable, efficient, and scalable power solutions has been driving the growth of the data center power infrastructure market, supporting the increasing demand for data processing, storage, and management capabilities.

Data Center Power Infrastructure Market Segmentation:

Segmentation 1: by Data Center Type

• Hyperscale Data Centers

• Colocation and Retail Data Centers

• Enterprise Data Centers

• Others

Colocation and Retail Data Centers to Lead the Market (by Data Center Type)

Colocation and retail data centers are expected to dominate the data center power infrastructure market by data center type, driven by their widespread adoption and critical role in supporting enterprise and cloud workloads. These facilities require advanced power infrastructure solutions to ensure high availability, scalability, and energy efficiency. Due to their growing demand for space and power density, colocation and retail data centers present substantial opportunities for the deployment of intelligent power distribution units and robust cooling technologies. As businesses increasingly outsource their IT infrastructure needs, these data center types will continue to lead investment and innovation in power infrastructure, shaping the future landscape of the data center power infrastructure market.

Segmentation 2: by Application

• Conventional and Non-AI Data Centers

• AI Data Centers

Conventional and Non-AI Data Centers to Lead the Market (by Application)

Conventional and non-AI data centers are expected to dominate the data center power infrastructure market by application, driven by their established presence and ongoing demand for traditional computing and storage services. These data centers require reliable and efficient power systems to support various enterprise applications, cloud services, and legacy workloads. Despite the rise of AI-focused facilities, the volume and diversity of conventional data centers ensure continued investment in power infrastructure solutions such as power distribution units. Their critical role in business continuity and data management positions them as key contributors to data center power infrastructure market growth in the foreseeable future.

Segmentation 3: by Power Architecture

• 12 V DC Rack?Level PSU Architecture

• 48 V DC Rack-Level PSU Architecture

• 400V ± DC Rack Power Architecture

48 V DC Rack-Level PSU Architecture to Lead the Market (by Power Architecture)

The 48 V DC rack-level power supply unit (PSU) architecture is expected to dominate the data center power infrastructure market by power architecture, driven by its efficiency, scalability, and compatibility with modern high-density IT equipment. This architecture reduces power conversion losses and simplifies power distribution within racks, improving energy efficiency and reducing cooling requirements.

As data centers increasingly adopt high-performance computing and AI workloads, the 48 V DC rack-level PSU offers a reliable and cost-effective solution to meet these demands. Its growing adoption has been influencing the design of next-generation data centers, making it a key driver in the evolution of data center power infrastructure market.

Segmentation 4: by Distribution

• Centralized

• Distributed

Centralized to Lead the Market (by Distribution)

Centralized power distribution is expected to dominate the data center power infrastructure market by distribution type, owing to its efficiency in managing large-scale power delivery and simplifying infrastructure management. This approach enables consolidated control over power sources, enhances reliability, and reduces operational complexity in data centers.

As data centers continue to scale and require robust power management solutions, centralized distribution offers advantages in optimizing energy use, improving system uptime, and supporting redundancy strategies. Its widespread adoption positions it as a preferred choice for modern data center designs, driving growth in the data center power infrastructure market.

Segmentation 5: by Power Supply

• Rack Level

o AC-DC

o DC-DC

• Infrastructure Level

o AC Supply

o DC Supply

Rack Level to Lead the Market (by Power Supply)

The rack-level power supply is expected to dominate the data center power infrastructure market by power supply type due to its ability to provide targeted and efficient power delivery directly to individual server racks. This approach enhances flexibility, simplifies maintenance, and improves redundancy by allowing independent power management at the rack level.

As data centers increase in density and complexity, rack-level power supplies support scalability and high availability requirements, making them essential for modern data center operations. Their growing adoption has been driving innovation and investment in power infrastructure solutions tailored to meet evolving IT demands in the data center power infrastructure market.

Segmentation 6: by Component

• Power Supply

o AC/DC and DC/DC Converters

o Multi-Phase Voltage Regulator Modules (VRMs)

o Fixed and Hot-Swap Power Modules

o Digital Power Control Units

• Power Distribution and Management

o Power Distribution Units (PDUs)

o Intelligent/Metered PDUs

o Busbar and Busway Systems

o Automatic Transfer Switches (ATS)

o Switchgear

Power Distribution and Management to Lead the Market (by Component)

Power distribution and management systems are expected to dominate the data center power infrastructure market by component, driven by their critical role in ensuring reliable and efficient delivery of electricity throughout the facility. These systems encompass power distribution units (PDUs), switchgear, circuit breakers, and intelligent monitoring solutions that enable precise control and optimization of power usage.

As data centers grow in complexity, the need for advanced power distribution and management becomes essential to maintain uptime, improve energy efficiency, and support scalability. Their prominence in maintaining operational continuity positions them as key components driving growth in the data center power infrastructure market.

Segmentation 7: by Region

• North America: U.S., Canada, and Mexico

• Europe: Germany, France, U.K., Italy, Netherlands, Ireland, and Rest-of-Europe

• Asia-Pacific: China, Japan, South Korea, Australia, India, and Rest-of-Asia-Pacific

• Rest-of-the-World

North America is expected to lead the data center power infrastructure market, supported by its robust regulatory environment, technological advancements, and significant investments in data center development.

The U.S. and Canada are at the forefront of adopting energy-efficient power systems, modular infrastructure, and renewable energy integration to meet growing demand in the data center power infrastructure market. Strong collaboration between public and private sectors, innovation in power management technologies, and rising requirements for high-performance computing have been driving the region’s market dominance. North America’s emphasis on improving power reliability, reducing operational costs, and enhancing scalability positions it as a key player in shaping the future of data center power infrastructure market.

Recent Developments in the Data Center Power Infrastructure Market

• In February 2025, Hyperscale Data announced plans to expand its Michigan data center from 30MW to 300MW in partnership with a local utility. The company has been negotiating a formal agreement to complete the power upgrade within 44 months, which will enhance its ability to meet the growing demand for AI and high-performance computing services. Hyperscale has been transitioning into a pure-play data center operator and has been exploring strategic options, including raising capital or forming joint ventures.

• In January 2025, the U.K. government announced a $17.27 billion investment in data center projects as part of its AI action plan, including establishing AI growth zones and a new supercomputer to enhance the U.K.'s computing capabilities. These initiatives align with the U.K.’s strategy to promote AI development and digital infrastructure. The greenfield projects will support the growing demand for data centers and digital services, particularly in the AI and HPC sectors.

• In May 2024, Oracle announced plans to open two new public cloud regions in Morocco to support AI-driven innovation and digital transformation across Africa. The regions in Casablanca and Settat are expected to provide local and regional businesses with access to Oracle Cloud Infrastructure (OCI), helping them modernize applications and utilize advanced AI, data, and analytics capabilities. The move is part of Oracle's broader strategy to expand its digital infrastructure footprint, aligning with Morocco's goal to modernize public services and foster growth opportunities in the region.

• In May 2024, Oracle announced plans to open two new public cloud regions in Morocco to support AI-driven innovation and digital transformation across Africa. The regions in Casablanca and Settat will provide local and regional businesses access to Oracle Cloud Infrastructure (OCI), helping them modernize applications and leverage advanced AI, data, and analytics capabilities.

Demand - Drivers, Limitations, and Opportunities

Market Drivers: Rising Data Consumption

Rising data consumption is a major driver in the data center power infrastructure market, as the demand for data storage, processing, and transmission continues to grow. The proliferation of cloud services, streaming platforms, big data analytics, and the Internet of Things (IoT) has significantly increased the amount of data generated worldwide. As businesses and consumers rely more on digital technologies for daily operations, the need for robust data center infrastructures to manage, store, and process this data becomes increasingly critical.

Several industry instances highlight how rising data consumption has been influencing the data center power infrastructure market. Cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud have been expanding their data center networks to meet the growing demand for storage and processing power. These companies have been investing in high-capacity uninterruptible power supplies (UPS), intelligent power distribution units (PDUs), and energy-efficient cooling systems to support the increasing workloads. Additionally, data centers that support industries such as e-commerce, media streaming, and telecommunications have been experiencing rapid growth in energy demand due to the constant need for real-time data delivery and storage.

Furthermore, the potential for growth in the data center power infrastructure market remains strong as data consumption is expected to continue increasing. The rapid adoption of new technologies such as artificial intelligence (AI), machine learning, and 5G networks will further drive the demand for high-performance data centers. As the volume of data expands, the need for power-efficient, scalable, and sustainable solutions will become even more critical. The continued rise in data consumption will have a lasting impact on the data center power infrastructure market, driving innovation and leading to more sustainable and resilient power systems for data centers.

Market Challenges: High Initial Investment

High initial investment remains a significant restraint in the data center power infrastructure market. The upfront costs associated with building and upgrading power systems, such as uninterruptible power supplies (UPS), power distribution units (PDUs), energy storage solutions, and cooling systems, can be substantial. These investments are required to ensure reliable, scalable, and energy-efficient operations, particularly as the demand for data center services continues to rise. Many companies must allocate significant capital to meet both the infrastructure needs and sustainability goals, which may delay or limit the expansion of data center capacity, especially for smaller operators or those in emerging markets.

Hyperscale data center operators have invested billions into their global infrastructures, including energy-efficient and renewable power systems. While these investments offer long-term benefits in terms of energy savings and sustainability, the high initial costs could be a barrier to entry for smaller players in the data center power infrastructure market. Additionally, operators seeking to upgrade existing facilities to meet rising demand for computing power and sustainability standards may encounter significant financial hurdles in securing the necessary funding for such large-scale infrastructure upgrades.

Furthermore, the potential for innovation in financing and technology solutions may reduce the impact of high initial investments. As power infrastructure becomes more modular and scalable, operators could deploy solutions incrementally, lowering upfront costs. Furthermore, the development of more cost-efficient and energy-dense technologies, along with greater availability of renewable energy options, could help reduce long-term capital expenditures. These advancements could enable more players in the market, especially smaller and regional operators, to enter or expand their presence in the data center industry.

Market Opportunities: Growth of Edge Computing

The growth of edge computing presents a significant opportunity in the data center power infrastructure market. As more data processing occurs at the edge of networks rather than centralized data centers, the demand for localized, high-efficiency power infrastructure grows. Edge computing allows for faster processing of data and lower latency, but it requires data centers to be closer to end users and to operate with optimized power systems to handle fluctuating workloads. These decentralized systems must be highly resilient and energy-efficient to support the diverse range of edge applications, creating a strong market demand for specialized power infrastructure solutions.

For instance, IBM has been at the forefront of combining edge computing with AI-powered solutions. IBM’s edge computing systems are increasingly being deployed in remote areas to support manufacturing, logistics, and agriculture industries. These systems require robust and resilient power infrastructure to handle real-time data processing and analytics in environments with limited access to traditional power grids.

Furthermore, the future potential of edge computing in the data center power infrastructure market is vast. As industries continue to adopt edge computing for real-time applications, the demand for localized power infrastructure will continue to rise. This trend will encourage further innovation in energy-efficient, modular power systems capable of supporting these distributed facilities. The development of smarter, more scalable power solutions that could be deployed rapidly across edge locations will be key to meeting the growing demands of edge computing. Additionally, as these edge data centers become more energy-conscious, opportunities will emerge for integrating renewable energy sources and advanced energy storage systems to optimize power consumption further and reduce environmental impact.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The global data center power infrastructure market is expected to experience significant growth in the coming years, driven by the increasing demand for cloud services, artificial intelligence (AI), and big data applications. As industries across the globe continue to rely more on data-driven solutions, the need for robust, efficient, and scalable power infrastructure becomes critical. Power systems in data centers must support the ever-growing data processing and storage requirements while ensuring operational reliability and minimizing downtime. The rising adoption of advanced technologies, such as edge computing and 5G networks, has been further accelerating the demand for power infrastructure that can handle higher loads and provide consistent performance. The market has also been witnessing a shift toward more resilient and energy-efficient power solutions to address the increasing power demands of modern data centers.”

Focus on Data Center Type, Application, Power Architecture, Distribution, Power Supply, Component and Region - Analysis and Forecast, 2025-2035

The market study conducted by BIS Research defines the data center power infrastructure market as a sector focused on the design, deployment, and management of power systems that ensure reliable, efficient, and scalable electricity delivery to data center operations.

Key business opportunities in the data center power infrastructure market include the growing demand for scalable and efficient power solutions driven by the rise in cloud computing, AI, and big data applications.

Existing players have been focusing on partnerships and collaborations to enhance their technology portfolios and expand market reach. Companies have also been investing in advanced power distribution systems, modular solutions, and AI-driven power management technologies to stay competitive in an increasingly energy-conscious and data-intensive environment.

A new entrant can focus on partnering with existing data center power infrastructure providers. Also, start-ups can focus on funding, launching new innovative products, and expanding their sales and distribution networks.

The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the data center power infrastructure market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the data center power infrastructure market landscape

• Qualitative and quantitative analysis of the data center power infrastructure market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Data center operators, cloud service providers, infrastructure developers, equipment manufacturers, and energy solution providers should buy this report.

The global data center PDUs and PSUs market is projected to reach $73,376.5 million by 2035...