A quick peek into the report

Global Digital Diagnostics Market Overview

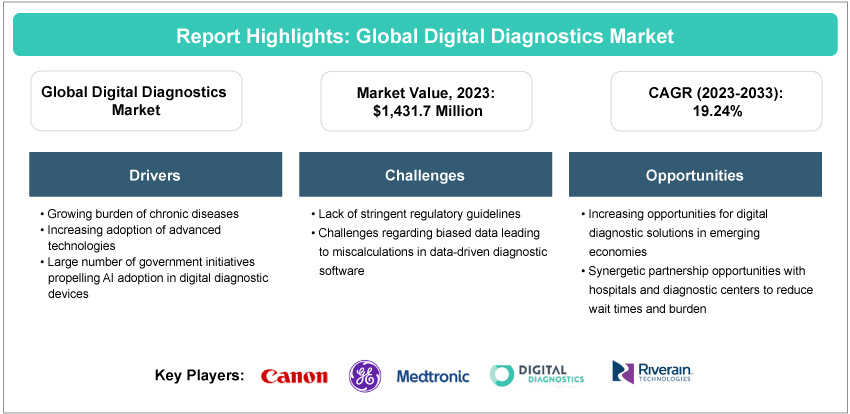

The global digital diagnostics market is projected to reach $8,319.2 million by 2033 from $1,431.7 million in 2023, growing at a CAGR of 19.24% during the forecast period 2023-2033. The market is set to experience substantial growth and transformation due to technological advancements, rising interest in telehealth solutions, and a shift towards personalized healthcare.

Market Lifecycle Stage

The global digital diagnostics market is characterized by intense competition, as established entities and emerging players compete for a share of the market. The anticipated growth and transformation of the market bring forth both challenges and opportunities, rendering it a dynamic landscape to observe in the upcoming years. While the digital diagnostics sector continues to grow, companies are expected to confront challenges linked to adhering to regulations, safeguarding data, and coping with market saturation. Nonetheless, there are opportunities for those who can quickly adapt to technological advancements, establish strategic partnerships, and meet the changing needs of customers.

Industry Impact

The digital diagnostics market is reshaping industries, particularly healthcare, by ushering in transformative changes. Advanced technologies such as artificial intelligence and machine learning are enhancing the precision and speed of medical diagnostics, revolutionizing patient care. The integration of data analytics not only provides valuable insights into population health but also drives evidence-based decision-making by healthcare organizations and policymakers. The competitive landscape is evolving, fostering innovation as companies vie to offer cutting-edge diagnostic solutions.

The industry's advancements in digital diagnostics research and development continually address population health trends, disease prevalence, and treatment outcomes. As a result, the digital diagnostics market's impact extends beyond technological integration for diagnosis, making it an integral component of global health strategies and broader ecosystem.

Market Segmentation:

Segmentation 1: by Application

• Cardiology

• Oncology

• Neurology

• Pathology

• Others

Oncology to Dominate the Global Digital Diagnostics Market (by Application)

The oncology segment dominated the global digital diagnostics market (by application) in FY2022.

The oncology sector dominates the digital diagnostics market for various compelling reasons. Given the intricate nature of cancer diagnosis and treatment, there is a need for sophisticated and precise diagnostic tools, with digital diagnostics providing advanced solutions through imaging and molecular diagnostics.

Segmentation 2: by End User

• Hospitals

• Clinical Laboratories

• Others

Hospitals to Dominate the Global Digital Diagnostics Market (by End User)

The hospitals segment dominated the global digital diagnostics market (by end user) in FY2022.

Hospitals hold a substantial portion of the end user segment in the global digital diagnostics market due to their pivotal role as primary centers for medical diagnostics. The incorporation of digital technologies within hospital settings serves to optimize diagnostic procedures, resulting in improved efficiency and accuracy.

Segmentation 3: by Product

• Hardware

• Software

Software to Dominate the Global Digital Diagnostics Market (by Product)

The global digital diagnostics market (by product) was dominated by the software segment in FY2022. Digital diagnostics heavily relies on advanced software applications for tasks such as image analysis, data interpretation, and diagnostic decision support.

Segmentation 4: by Region

• North America

• Europe

• Asia-Pacific

• Latin America

• Middle East and Africa

North America holds the largest share during the forecast period 2023-2033, and Asia-Pacific is expected to witness the highest CAGR for the forecast period 2023-2033.

Demand – Drivers, Restraints, and Opportunities

Market Drivers:

Growing burden of chronic diseases: With the rising incidence of chronic diseases, early diagnostic intervention is a key factor leading to the growth of digital diagnostic solutions worldwide. Digital diagnostics, powered by artificial intelligence, machine learning, and deep learning algorithms, help alleviate the burden of an increasing patient population and further provide faster diagnosis.

Market Restraints:

Challenges regarding biased data leading to miscalculations in data-driven diagnostic software: The bias introduced by the underrepresentation of certain population segments can result in skewed outcomes from AI-enabled medical devices, potentially leading to misdiagnoses. This obstacle in adopting AI-enabled medical devices as reliable clinical decision-support tools stems from concerns about their accuracy and reliability. These inherent biases within AI systems and the potential for inaccurate diagnoses or prognoses pose a threat to patient safety, raising questions about the accountability of stakeholders in healthcare settings, thereby hindering the growth of the digital diagnostics market.

Market Opportunities:

Increasing Opportunities for Digital Diagnostic Solutions in Emerging Economies: Emerging economic countries face multiple challenges, such as limited specialized medical professionals and growing burden of patients. This creates a need for accurate diagnosis and automated tools that assist and lighten the load for physicians. Digital diagnostic solutions can bridge the gap between remote communities and medical centers.

Analyst View

According to Swati Sood, Principal Analyst at BIS Research, “The global digital diagnostics market is experiencing growth driven by a confluence of factors. One of the primary drivers is the increasing adoption of artificial intelligence. Moreover, the market is driven by a growing number of government initiatives and increasing burden of chronic diseases. Furthermore, burdened hospitals and laboratories act as an opportunity for the market players to strategically partner and further expand their business.”

Digital Diagnostics Market - A Global and Regional Analysis

Focus on Application, Product, End User, and Country - Analysis and Forecast, 2023-2033

Frequently Asked Questions

Ans: Digital diagnostics refers to the application of digital technologies, including software, algorithms, and electronic devices, in the process of diagnosing medical conditions and diseases. This field involves the integration of advanced technologies such as artificial intelligence, machine learning, and data analytics to enhance the accuracy and efficiency of diagnostic procedures in healthcare. Digital diagnostics encompass a variety of applications, including but not limited to digital imaging, in vitro diagnostics, point-of-care testing, telemedicine, wearable devices, and health information technology. The overarching goal is to leverage digital tools to improve the precision, accessibility, and overall effectiveness of medical diagnoses.

Ans: The digital diagnostics market has witnessed several trends, and here are some key trends observed in this market:

• Increasing number of startups in the market: Investment in this sector has experienced a consistent upward trend, marked by the entry of numerous startups introducing inventive products. The growing need for prompt and precise diagnostics, combined with notable technological progress, has paved the way for well-funded startups to thrive in this field.

• Partnerships and collaborations among market players: Partnerships in the digital diagnostics market drive accelerated innovation by integrating diverse technologies and accessing specialized expertise while also facilitating market expansion and regulatory compliance through resource-sharing and collaborative efforts.

These are only a few illustrations of the major trends in the industry.

Ans: The global digital diagnostics market is currently witnessing several developments, primarily aimed at bringing new products and entering into collaborations and partnerships. Major manufacturers of products are actively undertaking significant business strategies to translate success in research and development into the commercial clinical setting. Many players are also looking forward to collaborations with hospitals and clinical laboratories.

Ans: A new entrant can focus on developing innovative diagnostic solutions. The market majorly consists of top established players such as Canon, Inc., GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers, and VUNO, Inc. The new entrants can focus on their strategy of product launches and global expansions.

• Market Growth Potential

• Patent Analysis

• Regulatory Framework

• Market Dynamics

• Market Opportunities

• Detailed Segmentation such as Application, End User, and Product

• Region and Country-Level Market Size and Forecast for Application, End User, and Product

• Competitive Landscape

Ans: Manufacturers, CROs, CMOs, and CDMOs focusing on MedTech can buy this report.