Published Year: 2024

Europe EV Fleet Management System Market: Focus on Application, Product, and Country - Analysis and

The Europe EV fleet management system market is projected to reach $1,875.1 million by 2033...

Focus on Application, Product, and Country - Analysis and Forecast, 2024-2033

Delivery Time: 1-5 Working Days

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

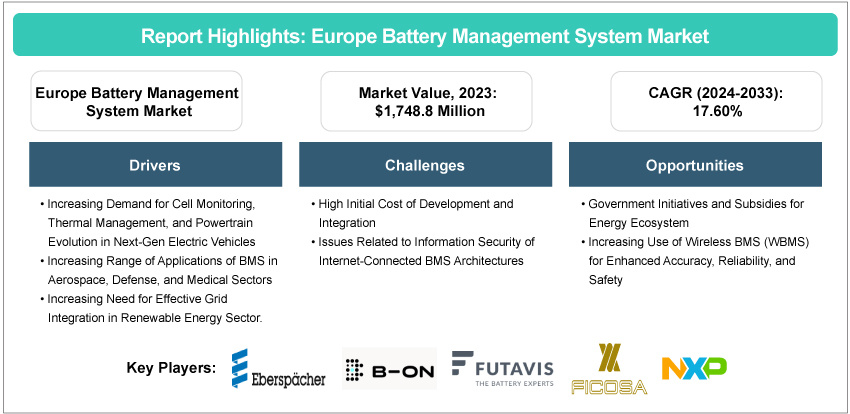

The Europe battery management system market was valued at $1,748.8 million in 2023 and is expected to reach $8,882.4 million by 2033, with a CAGR of 17.60% from 2024 to 2033. The market is in a growth phase and is projected to experience significant expansion. Market players investing in research, infrastructure development, and strategic partnerships are anticipated to capitalize on the increasing demand for battery management systems, driven by advancements in technology and development in power storage methods, over the forecast period from 2024 to 2033.

Introduction of Battery Management System

A battery management system (BMS) is an integral component in the management and regulation of rechargeable batteries. It ensures the optimal functioning of battery cells by monitoring key parameters such as voltage, temperature, and state of charge. The BMS provides protection against overcharging, over-discharging, and thermal runaway, thereby enhancing battery safety and longevity. It balances the charge among individual cells to maximize efficiency and lifespan. In addition, the BMS facilitates communication with other electronic systems, enabling better integration and control in applications ranging from electric vehicles to renewable energy storage systems. Its role is critical in optimizing battery performance, ensuring reliability, and improving overall energy management.

Market Introduction

The Europe battery management system (BMS) market is experiencing robust growth, driven by the increasing adoption of electric vehicles (EVs), renewable energy storage systems, and portable electronics. As governments across Europe implement stringent emissions regulations and promote sustainable energy initiatives, the demand for efficient battery management solutions has surged. The market benefits from advancements in battery technologies and the integration of BMS with IoT for enhanced monitoring and control. Key players are focusing on innovation and strategic partnerships to enhance their market presence. Germany, the U.K., and France are leading the market due to their strong automotive and renewable energy sectors. Overall, the Europe BMS market is poised for significant expansion, driven by technological advancements and supportive regulatory frameworks.

Industrial Impact

The Europe battery management system (BMS) market significantly impacts various industries by enhancing energy efficiency and sustainability. In the automotive sector, BMS technology is pivotal for the performance and safety of EVs, contributing to the region's transition to greener transportation. The renewable energy industry benefits from BMS by optimizing the storage and utilization of energy from solar and wind sources, thereby supporting grid stability and energy reliability. Industrial applications, including manufacturing and logistics, leverage BMS to ensure uninterrupted power supply and operational efficiency. Additionally, the rise of smart grid projects and IoT integration is further driving the adoption of BMS, making it a cornerstone for Europe’s industrial modernization and environmental goals.

The key players operating in the Europe battery management system market include B–On, Analog Devices, Inc., Eberspächer, Ewert Energy Systems, Inc., Ficosa Internacional SA, Futavis GmbH, Infineon Technologies AG, LG Energy Solution, NXP Semiconductors, and Panasonic Holdings Corporation, among others. These companies are focusing on strategic partnerships, collaborations, and acquisitions to enhance their product offerings and expand their market presence.

Market Segmentation:

Segmentation 1: by Application

• Automotive

• Renewable Energy

• Consumer Electronics

• Industrial

• Telecommunications

• Others

Automotive Segment to Dominate Europe Battery Management System Market (by Application)

In Europe, the battery management system (BMS) is pivotal in the automotive sector, particularly for managing and safeguarding lithium-ion batteries in electric vehicles (EVs). It optimizes battery performance and longevity by monitoring states such as voltage, temperature, and charge status. By precisely controlling and regulating charging and discharging processes, the BMS enhances vehicle efficiency and ensures cells operate within safe parameters, balancing the charge to prevent overcharging or deep discharging. Advanced BMS also integrates with vehicle telematics systems, offering real-time data for predictive maintenance and energy management. This integration significantly extends battery life, improves vehicle reliability, and maximizes efficient battery power use, contributing to environmental sustainability. The BMS' role in preventing battery failures and reducing emissions makes it a leading application in the Europe battery management market, offering substantial benefits over traditional battery technologies and enhancing the overall value proposition of electric vehicles.

Segmentation 2: by Battery Type

• Lithium-Ion

• Lead-Acid

• Nickel-Based

• Other Batteries

Lithium-Ion to Dominate Europe Battery Management System Market (by Battery Type)

Lithium-ion (Li-ion) batteries dominate the Europe battery management system (BMS) market due to their superior performance and reliability. Known for their high energy density, lightweight, and long cycle life, Li-ion batteries are ideal for automotive, consumer electronics, renewable energy, and more. Integrating BMS with Li-ion batteries optimizes usage by monitoring voltage, current, and temperature, ensuring safe and efficient operation. Their high energy-to-weight ratio provides more power in less space, which is crucial for portable devices and electric vehicles. With extended lifespans and rapid charging capabilities, Li-ion batteries reduce maintenance costs and enhance convenience. Minimal self-discharge allows for longer storage without significant charge loss, making them the leading battery type in this market segment.

Segmentation 3: by System Type

• Centralized

• Distributed

• Modular

Recent Developments in the Europe Battery Management System Market

• In June 2024, LG Energy Solution teamed up with Analog Devices, Inc. to gain a competitive edge in battery management total solution.

• In April 2024, B–ON and Chery Group unveiled a strategic partnership, including the formation of a joint venture and the launch of the Pelkan electric light commercial vehicle, reinforcing B–ON's market presence and product diversification.

• In March 2024, LG Energy Solution announced plans to collaborate with Qualcomm Technologies, Inc. to develop advanced diagnostic solutions for battery management systems (BMS). These strategic partnerships underscore LG Energy Solution's commitment to innovation and excellence in BMS technology.

• In Oct 2023, Shizen Energy Inc. (Shizen Energy) and Luxembourg-based B–ON Group (B–ON) agreed to enter a discussion of joint investment in Japanese electric vehicle start-up eMotion Fleet Inc.

• In November 2023, NXP Semiconductors introduced its next-generation battery cell controller IC, enhancing the performance and safety of the battery management system (BMS).

• In September 2022, NXP Semiconductors partnered with Elektrobit to co-develop a software platform supporting its HVBMS reference design. To further strengthen its position in the Europe battery management system market, the company should focus on collaborating more with automotive manufacturers in Europe to develop next-generation BMS, keeping in mind specific regional regulatory requirements and market demands, ensuring seamless integration and compliance.

Demand - Drivers, Limitations, and Opportunities

Market Demand: Increasing Demand for Cell Monitoring, Thermal Management, and Powertrain Evolution in Next-Gen Electric Vehicles

The Europe battery management system (BMS) market is witnessing substantial growth, driven by the increasing demand for advanced cell monitoring, thermal management, and powertrain evolution in next-generation electric vehicles (EVs). These technological advancements are critical for enhancing the performance, safety, and efficiency of EVs, positioning Europe as a key player in the global automotive industry.

Advanced cell monitoring systems are essential for ensuring the optimal performance and longevity of battery packs in EVs. By providing real-time data on the health, charge state, and temperature of individual cells, these systems enable proactive management and maintenance, preventing potential failures and extending battery life. The rising complexity and capacity of modern battery packs necessitate sophisticated BMS solutions that can handle the intricacies of cell-level monitoring.

Thermal management is another crucial aspect driving the demand for advanced BMS technologies. Efficient thermal management systems are vital for maintaining the safe operating temperatures of battery packs, particularly during high-demand conditions such as rapid charging and discharging. Innovations in thermal management not only enhance the safety of EVs but also improve their overall performance and reliability, making them more attractive to consumers and manufacturers alike.

The evolution of powertrain technologies is also a significant factor contributing to the growth of the BMS market. As EV manufacturers strive to improve the efficiency and power output of their vehicles, the integration of advanced BMS solutions becomes increasingly important. These systems optimize the energy flow within the powertrain, ensuring maximum efficiency and performance.

Market Challenge: High Initial Costs of Development and Integration

The high initial cost of development and integration stands as a significant restraint in the Europe battery management system (BMS) market. This financial barrier can impede the rapid adoption and widespread implementation of advanced BMS technologies, particularly among small and medium-sized enterprises (SMEs) and emerging players in the market.

Developing state-of-the-art BMS involves substantial investment in research and development, sophisticated design processes, and the acquisition of high-precision components. These activities demand significant capital expenditure, which can be a considerable burden for companies with limited financial resources. Furthermore, the integration of BMS into existing systems requires extensive modifications and upgrades to infrastructure, further escalating costs.

This financial challenge is exacerbated by the need for compliance with stringent regulatory standards and certifications specific to the European market. Achieving these certifications necessitates rigorous testing and validation processes, which are both time-consuming and costly. The additional expense associated with meeting these regulatory requirements can deter companies from investing in the latest BMS technologies.

Moreover, the rapidly evolving nature of battery technology and BMS solutions means that companies must continuously invest in innovation to stay competitive. This constant need for technological upgrades can strain financial resources and deter long-term investment in advanced BMS solutions.

The high initial cost of development and integration also impacts the overall market dynamics by limiting the entry of new players and reducing competitive pressures. This can slow the pace of innovation and the availability of cost-effective solutions, ultimately affecting the growth trajectory of the BMS market in Europe.

Market Opportunity: Government Initiatives and Subsidies for Energy Ecosystem

The European Union's launch of several government initiatives and subsidies aimed at enhancing the energy ecosystem presents substantial opportunities for the battery management system (BMS) market. These strategic initiatives, including the European Green Deal and the Fit for 55 packages, are designed to drastically reduce greenhouse gas emissions and promote the widespread adoption of renewable energy sources, directly benefiting the BMS market.

Initiated in 2020, the European Green Deal aims to establish Europe as the first climate-neutral continent by 2050. This initiative encourages significant investments in renewable energy and energy efficiency, providing fertile ground for the growth of BMS technologies. BMS solutions are critical for optimizing the performance and safety of energy storage systems, which are essential components of renewable energy installations and electric vehicles (EVs). The substantial investments driven by the European Green Deal ensure that advanced BMS technologies will play a pivotal role in achieving climate neutrality by enhancing the efficiency and reliability of energy storage solutions.

Launched in 2021, the Fit for 55 package aims to reduce greenhouse gas emissions by 55% by 2030 compared to 1990 levels. This initiative focuses on increasing the use of renewable energy and improving energy efficiency across the European Union. Subsidies and financial incentives provided under the Fit for 55 packages support the adoption of advanced BMS technologies. These technologies are essential for making energy storage systems more efficient and reliable, which is crucial for the integration of renewable energy into the grid and supporting the growing market for EVs.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst, BIS Research, “The Europe battery management system market is set for substantial growth, fueled by the rising demand for electric vehicles and sustainable energy solutions. Government regulations and policies promoting advanced battery technologies, coupled with significant investments in research and development for BMS innovations, are expected to drive the market forward. Leading market players are concentrating on strategic partnerships, collaborations, mergers, and acquisitions to broaden their market reach and enhance their product portfolios, ensuring strong growth in the upcoming years."

Focus on Application, Product, and Country - Analysis and Forecast, 2024-2033

A battery management system (BMS) is an electronic system that manages and regulates the performance of rechargeable batteries. It ensures the optimal functioning of battery cells by monitoring critical parameters such as voltage, temperature, and state of charge. The BMS protects the battery from conditions such as overcharging, over-discharging, and overheating, which can lead to reduced battery life or safety hazards. Additionally, it balances the charge among individual cells to maximize efficiency and longevity. The BMS also facilitates communication with other electronic systems, enabling better integration and control in various applications, such as electric vehicles, renewable energy storage systems, and portable electronics.

Key business opportunities in the Europe battery management system market include catering to the rising demand for EVs and renewable energy storage solutions driven by stringent emissions regulations and government incentives for sustainable technologies. Additionally, the market offers growth prospects through advancements in IoT integration and smart grid projects.

Existing market players in the battery management System (BMS) industry are adopting strategies such as mergers and acquisitions to consolidate market presence, launching innovative products to meet evolving technological demands, forming strategic partnerships and collaborations to expand their market reach, and investing in research and development to drive advancements in BMS technology. They are also focusing on business expansions to tap into emerging markets and enhance their competitive edge.

A new entrant can focus on partnering with existing battery management solution providers. Also, start-ups can focus on funding, launching new innovative products, and expanding their sales and distribution networks.

The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the Europe battery management system market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the Europe battery management system market landscape

• Qualitative and quantitative analysis of the Europe battery management system market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Battery management solution providers can buy this report.

The Europe EV fleet management system market is projected to reach $1,875.1 million by 2033...