Published Year: 2019

Global Military Artificial Intelligence (AI) and Cybernetics Market - Analysis and Forecast, 2019-20

The Global Military Artificial Intelligence Market report by BIS Research projects the market...

Focus on Technology, Application, and Component

Delivery Time: 1-5 Working Days

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

1.1 Drivers

1.1.1 Increasing Expenditure and Modernization of Defense Industry for Developing Military Equipment

1.1.2 Rapid Technological Advancement in Artificial Intelligence and Robotics

1.1.3 Increasing Demand for Cloud Services in Defense

1.2 Restraints

1.2.1 Expensive Development and Maintenance of AI, IoT, and 3D Printing-Based Systems

1.2.2 Rising Cyber Threat for Military Data

1.3 Opportunities

1.3.1 Rising Adoption of AI and Internet of Things for Military Operation

1.3.2 Increasing Demand for Next Generation Battlefield Technologies

1.3.3 Manufacturing of Engine and Structure of Military Vehicles Through 3D Printing

2.1 Key Strategies and Developments

2.1.1 Partnerships, Collaborations, Contracts, and Agreements

2.1.2 Mergers and Acquisitions

2.1.3 Product Launches

2.1.4 Other Developments

2.2 Competitive Benchmarking

3.1 Industry Overview

3.2 Ongoing Defense Programs

3.3 Emerging Technological Trends

3.3.1 Internet of Battlefield Technology

3.3.2 Advanced Analytics and Big Data

3.3.3 Augmented and Virtual Reality

3.3.4 3D Printing of Drones and Missiles

3.3.5 Biotechnology in Defense Industry

3.3.6 Advanced Sensor

3.4 Patent Analysis

3.4.1 Artificial Intelligence

3.4.2 Internet of Things

3.4.3 Wearable Devices

3.5 Supply Chain Analysis

3.5.1 Wearable Devices

3.5.2 IoT (Internet of Things)

4.1 Assumptions and Limitations

4.2 Market Overview

5.1 Market Overview

5.2 Artificial Intelligence

5.2.1 Land

5.2.1.1 Armored Fighting Vehicle

5.2.1.2 Command and Control System

5.2.1.3 Military Unmanned Ground Vehicle

5.2.1.4 Others

5.2.2 Naval

5.2.2.1 Submarine

5.2.2.2 Unmanned Marine Vehicle

5.2.2.3 Ship

5.2.3 Air

5.2.3.1 Unmanned Aerial Vehicle

5.2.3.2 Fighter Jet and Aircraft

5.2.4 Space

5.2.4.1 Satellite

5.2.4.2 Space Launch Vehicle

5.3 3D Printing

5.3.1 Land

5.3.1.1 Military Vehicle (Armored and Unmanned Ground Vehicle)

5.3.1.1.1 Engine

5.3.1.1.2 Structure

5.3.2 Soldier Equipment

5.3.2.1 Helmet

5.3.2.2 Vest

5.3.2.3 Communication Device

5.3.3 Air

5.3.3.1 Unmanned Aerial Vehicle

5.3.3.1.1 UAV Engine

5.3.3.1.2 UAV Aerostructure

5.3.3.2 Aircraft and Missile

5.3.3.3 Engine

5.3.3.3.1 Aerostructure

5.3.3.3.2 Cockpit Control

5.3.3.3.3 Guidance System

5.3.4 Naval

5.3.4.1 Unmanned Marine Vehicle

5.3.4.2 Ship

5.3.5 Space

5.4 Internet of Things

5.4.1 Wi-Fi

5.4.2 RFID

5.4.3 Communication Devices

5.4.4 Others

5.5 Wearable Devices

5.5.1 Smart Clothing

5.5.2 Exoskeleton

5.5.2.1 Passive

5.5.2.2 Powered

5.5.3 Vision and Surveillance

5.5.3.1 Augmented Reality/Virtual Reality

5.5.3.2 Head-Up Display

5.5.3.3 Smart Helmets and Imaging

5.5.4 Others

6.1 Market Overview

6.1.1 Cybersecurity

6.1.2 Surveillance

6.1.3 Data Warfare

6.1.4 Logistics and Transportation

6.1.5 Explosive Ordinance Disposal (EOD)

6.1.6 Health Monitoring

6.1.7 Combat Simulation and Training

6.1.8 Others

7.1 Market Overview

7.2 Hardware

7.2.1 Hardware Next Generation Battlefield Technology Market (by Technology)

7.3 Software

7.3.1 Software Next Generation Battlefield Technology Market (by Technology)

8.1 Market Overview

8.2 North America

8.2.1 North America Next Generation Battlefield Technology Market (by Technology)

8.2.1.1 U.S.

8.2.1.2 Canada

8.3 Europe

8.3.1 Europe Next Generation Battlefield Technology Market (by Technology)

8.3.1.1 U.K.

8.3.1.2 Germany

8.3.1.3 France

8.3.1.4 Russia

8.3.1.5 Italy

8.3.1.6 Rest-of-Europe

8.4 Asia-Pacific

8.4.1 Asia-Pacific Next Generation Battlefield Technology Market (by Technology)

8.4.1.1 China

8.4.1.2 India

8.4.1.3 South Korea

8.4.1.4 Japan

8.4.1.5 Australia

8.4.1.6 Rest-of-Asia-Pacific

8.5 Rest-of-the-World

8.5.1 Rest-of-the-World Next Generation Battlefield Technology Market (by Technology)

8.5.1.1 Middle East and Africa

8.5.1.2 Latin America

9.1 BAE Systems

9.1.1 Company Overview

9.1.2 Role of BAE Systems in Global Next Generation Battlefield Technology Market

9.1.3 Financials

9.1.4 SWOT Analysis

9.2 The Boeing Company

9.2.1 Company Overview

9.2.2 Role of The Boeing Company in Global Next Generation Battlefield Technology Market

9.2.3 Financials

9.2.4 SWOT Analysis

9.3 Exone

9.3.1 Company Overview

9.3.2 Role of Exone in Global Next Generation Battlefield Technology Market

9.3.3 Financials

9.3.4 SWOT Analysis

9.4 Elbit Systems

9.4.1 Company Overview

9.4.2 Role of Elbit Systems in Global Next Generation Battlefield Technology Market

9.4.3 Financials

9.4.4 SWOT Analysis

9.5 FLIR Systems Inc.

9.5.1 Company Overview

9.5.2 Role of Flir Systems Inc. in Global Next Generation Battlefield Market

9.5.3 Financials

9.5.4 SWOT Analysis

9.6 General Dynamics

9.6.1 Company Overview

9.6.2 Role of General Dynamics in Global Next Generation Battlefield Technology Market

9.6.3 Financials

9.6.4 SWOT Analysis

9.7 Harris Corporation

9.7.1 Company Overview

9.7.2 Role of Harris Corporation in Next Generation Battlefield Technology Market

9.7.3 Financials

9.7.4 SWOT Analysis

9.8 IBM

9.8.1 Company Overview

9.8.2 Role of IBM in Next Generation Battlefield Technology Market

9.8.3 Financials

9.8.4 SWOT Analysis

9.9 Lockheed Martin Corporation

9.9.1 Company Overview

9.9.2 Role of Lockheed Martin Corporation in Global Next Generation Battlefield Technology Market

9.9.3 Financials

9.9.4 SWOT Analysis

9.10 Leidos

9.10.1 Company Overview

9.10.2 Role of Leidos in Global Next Generation Battlefield Technology Market

9.10.3 Financials

9.10.4 SWOT Analysis

9.11 Northrop Grumman Corporation

9.11.1 Company Overview

9.11.2 Role of Northrop Grumman Corporation in Global Next Generation Battlefield Technology Market

9.11.3 Financials

9.11.4 SWOT Analysis

9.12 Raytheon Company

9.12.1 Company Overview

9.12.2 Role of Raytheon Company in Global Next Generation Battlefield Technology Market

9.12.3 Financials

9.12.4 SWOT Analysis

9.13 Rheinmetall Group

9.13.1 Company Overview

9.13.2 Role of Rheinmetall Group in Global Next Generation Battlefield Technology Market

9.13.3 Financials

9.13.4 SWOT Analysis

9.14 SparkCognition

9.14.1 Company Overview

9.14.2 Role of SparkCognition in Next Generation Battlefield Technology Market

9.14.3 SWOT Analysis

9.15 Thales Group

9.15.1 Company Overview

9.15.2 Role of Thales Group in Global Next Generation Battlefield Technology Market

9.15.3 Financials

9.15.4 SWOT Analysis

9.16 Other Key Players

9.16.1 3D System Corporation

9.16.2 High Tech Robotic System

9.16.3 Leonardo

9.16.4 Stratasys

9.16.5 Saab.

10.1 Scope of the Report

10.2 Global Next Generation Battlefield Technology Market Research Methodology

11.1 Related Reports

Table 1: Market Snapshot: Global Next Generation Battlefield Technology Market, Value, 2018 and 2024

Table 1.1: Advantages and Challenges of 3D Printing

Table 2.1: Partnerships, Collaborations, Contracts, and Agreements in Next Generation Battlefield Technology Market

Table 2.2: Mergers and Acquisitions

Table 2.3: Product Launches

Table 2.4: Other Developments

Table 3.1: Ongoing Defense Programs

Table 3.2: Significant Patents Granted for Artificial Intelligence, 2016-2019

Table 3.3: Significant Patents Granted for Internet of Things, 2016-2019

Table 3.4: Significant Patents Granted for Wearable Device, 2016-2019

Table 7.1: Hardware Next Generation Battlefield Technology Market (by Technology), Value ($Million), 2018-2024

Table 7.2: Software Next Generation Battlefield Technology Market (by Technology), Value ($Million), 2018-2024

Table 8.1: Global Next Generation Battlefield Technology Market (by Region), $Million, 2018-2024

Table 8.2: North America Next Generation Battlefield Technology Market (Platform), Value ($Million), 2018-2024

Table 8.3: Europe Next Generation Battlefield Technology Market (by Technology), Value ($Million), 2018-2024

Table 8.4: Asia-Pacific Next Generation Battlefield Technology Market (by Technology), Value ($Million), 2018-2024

Table 8.5: Rest-of-the-World Next Generation Battlefield Technology Market (by Technology), Value ($Million) 2018-2024

Figure 1: Global Defense Expenditure (2017, 2018)

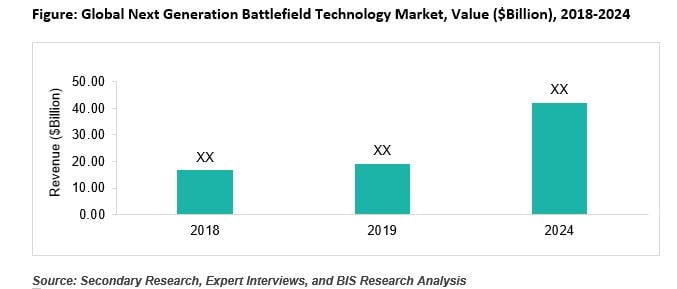

Figure 2: Global Next Generation Battlefield Technology Market, Value ($Billion), 2018-2024

Figure 3: Global Next Generation Battlefield Technology Market (by Application), Revenue ($Million), 2018 and 2024

Figure 4: Global Next Generation Battlefield Technology Market (by Platform), Revenue ($Million), 2018 and 2024

Figure 5: Global Next Generation Battlefield Technology Market (by Component), Revenue ($Million), 2018 and 2024

Figure 6: Global Next Generation Battlefield Technology Market (by Region), Value ($Million), 2018

Figure 1.1: Market Dynamics Snapshot

Figure 1.2: Global Defense Expenditure (2017, 2018)

Figure 1.3: Application of Cloud Services in Military

Figure 1.4: Role of Cyber Security

Figure 2.1: Key Strategies Adopted by Market Players

Figure 2.2: Percentage Share of Strategies Adopted by Market Players, January 2017-November 2019

Figure 2.3: Competitive Benchmarking, 2018

Figure 3.1: Industry Insights

Figure 3.2: Scenario of IoBT in Combat

Figure 3.3: Global Next Generation Battlefield Technology Market, Number of Patents Granted (Artificial Intelligence), 2016-2019

Figure 3.4: Global Next Generation Battlefield Technology Market, Patent Analysis (Artificial Intelligence) by Major Companies, 2016-2019

Figure 3.5: Global Next Generation Battlefield Technology Market, Key Patent Analysis (Artificial Intelligence) by Country, 2016-2019

Figure 3.6: Global Next Generation Battlefield Technology Market, Number of Patents Granted (Internet of Things), 2016-2019

Figure 3.7: Global Next Generation Battlefield Technology Market, Patent Analysis (Internet of Things) by Major Companies, 2016-2019

Figure 3.8: Global Next Generation Battlefield Technology Market, Key Patent Analysis (Internet of Things) by Country, 2016-2019

Figure 3.9: Global Next Generation Battlefield Technology Market, Number of Patents Granted (Wearables), 2016-2019

Figure 3.10: Global Next Generation Battlefield Technology Market, Patent Analysis (Wearable) by Major Companies, 2016-2019

Figure 3.11: Global Next Generation Battlefield Technology Market, Key Patent Analysis (Wearables) by Country, 2016-2019

Figure 3.12: Wearable Devices Supply Chain Analysis

Figure 3.13: Internet of Things (IoT) Supply Chain Analysis

Figure 4.1: Global Next Generation Battlefield Technology Market, Revenue ($Billion), 2018-2024

Figure 5.1: Classification of the Global Next Generation Battlefield Technology Market (by Artificial Intelligence)

Figure 5.2: Global Next Generation Battlefield Technology Market (by Artificial Intelligence), Value ($Million), 2018-2024

Figure 5.3: Global Next Generation Battlefield Technology Market (by Land), $Million, 2018-2024

Figure 5.4: Global Next Generation Battlefield Technology (Armored Fighting Vehicle), $Million, 2018-2024

Figure 5.5: Global Next Generation Battlefield Technology Market (Command and Control System), $Million, 2018-2024

Figure 5.6: Global Next Generation Battlefield Technology Market (Unmanned Ground Vehicle), $Million, 2018-2024

Figure 5.7: Global Next Generation Battlefield Technology Market (Others), $Million, 2018-2024

Figure 5.8: Global Next Generation Battlefield Technology Market (by Naval), $Million, 2018-2024

Figure 5.9: Global Next Generation Battlefield Technology Market (Submarine), $Million, 2018-2024

Figure 5.10: Global Next Generation Battlefield Technology Market (Unmanned Marine Vehicle), $Million, 2018-2024

Figure 5.11: Global Next Generation Battlefield Technology Market (Ship), $Million, 2018-2024

Figure 5.12: Global Next Generation Battlefield Technology Market (by Air), $Million, 2018-2024

Figure 5.13: Global Next Generation Battlefield Technology Market (Unmanned Aerial Vehicle), $Million, 2018-2024

Figure 5.14: Global Next Generation Battlefield Technology Market (Fighter Jet and Aircraft), $Million, 2018-2024

Figure 5.15: Global Next Generation Battlefield Technology Market (by Space), $Million, 2018-2024

Figure 5.16: Global Next Generation Battlefield Technology Market (Satellite), $Million, 2018-2024

Figure 5.17: Global Next Generation Battlefield Technology Market (Space Launch Vehicle), $Million, 2018-2024

Figure 5.18: Classification of the Global Next Generation Battlefield Technology Market (by 3D Printing)

Figure 5.19: Global Next Generation Battlefield Technology Market (by 3D Printing), Value ($Million), 2018-2024

Figure 5.20: Global Next Generation Battlefield Technology Market (by Land), $Million, 2018-2024

Figure 5.21: Global Next Generation Battlefield Technology Market (by Military Vehicle), $Million, 2018-2024

Figure 5.22: Global Next Generation Battlefield Technology (Engine), $Million, 2018-2024

Figure 5.23: Global Next Generation Battlefield Technology (Structure), $Million, 2018-2024

Figure 5.24: Global Next Generation Battlefield Technology Market (Soldier Equipment), $Million, 2018-2024

Figure 5.25: Global Next Generation Battlefield Technology Market (Helmet), $Million, 2018-2024

Figure 5.26: Global Next Generation Battlefield Technology Market (Vest), $Million, 2018-2024

Figure 5.27: Global Next Generation Battlefield Technology Market (Communication Device), $Million, 2018-2024

Figure 5.28: Global Next Generation Battlefield Technology Market (by Air), $Million, 2018-2024

Figure 5.29: Global Next Generation Battlefield Technology Market (Unmanned Aerial Vehicle), $Million, 2018-2024

Figure 5.30: Global Next Generation Battlefield Technology Market (UAV engine), $Million, 2018-2024

Figure 5.31: Global Next Generation Battlefield Technology Market (UAV aerostructure), $Million, 2018-2024

Figure 5.32: Global Next Generation Battlefield Technology Market (Aircraft and Missile), $Million, 2018-2024

Figure 5.33: Global Next Generation Battlefield Technology Market (Engine), $Million, 2018-2024

Figure 5.34: Global Next Generation Battlefield Technology Market (Aerostructure), $Million, 2018-2024

Figure 5.35: Global Next Generation Battlefield Technology Market (Cockpit Control), $Million, 2018-2024

Figure 5.36: Global Next Generation Battlefield Technology Market (Guidance System), $Million, 2018-2024

Figure 5.37: Global Next Generation Battlefield Technology Market (by Naval), $Million, 2018-2024

Figure 5.38: Global Next Generation Battlefield Technology Market (Unmanned Marine Vehicle), $Million, 2018-2024

Figure 5.39: Global Next Generation Battlefield Technology Market (Ship), $Million, 2018-2024

Figure 5.40: Global Next Generation Battlefield Technology Market (by Space), $Million, 2018-2024

Figure 5.41: Classification of the Global Next Generation Battlefield Technology Market (by IoT)

Figure 5.42: Global Next Generation Battlefield Technology Market (by IoT), Value ($Million), 2018-2024

Figure 5.43: Global Next Generation Battlefield Technology Market (Wi-Fi), $Million, 2018-2024

Figure 5.44: Global Next Generation Battlefield Technology Market (RFID), $Million, 2018-2024

Figure 5.45: Global Next Generation Battlefield Technology Market (Communication Devices), $Million, 2018-2024

Figure 5.46: Global Next Generation Battlefield Technology Market (Others), $Million, 2018-2024

Figure 5.47: Classification of the Global Next Generation Battlefield Technology Market (by Wearable Devices)

Figure 5.48: Global Next Generation Battlefield Technology Market (by Wearable Devices), Value ($Million), 2018-2024

Figure 5.49: Global Next Generation Battlefield Technology Market (Smart Clothing), $Million, 2018-2024

Figure 5.50: Global Next Generation Battlefield Technology Market (Exoskeleton), $Million, 2018-2024

Figure 5.51: Global Next Generation Battlefield Technology Market (Passive), $Million, 2018-2024

Figure 5.52: Global Next Generation Battlefield Technology Market (Powered), $Million, 2018-2024

Figure 5.53: Global Next Generation Battlefield Technology Market (Vision and Surveillance), $Million, 2018-2024

Figure 5.54: Global Next Generation Battlefield Technology Market (Augmented Reality/Virtual Reality), $Million, 2018-2024

Figure 5.55: Global Next Generation Battlefield Technology Market (Head-Up Display), $Million, 2018-2024

Figure 5.56: Global Next Generation Battlefield Technology Market (Smart Helmets and Imaging), $Million, 2018-2024

Figure 5.57: Global Next Generation Battlefield Technology Market (Monitoring, Smart Textiles, and Communication and Computing), $Million, 2018-2024

Figure 6.1: Global Next Generation Battlefield Technology Market (by Application)

Figure 6.2: Global Next Generation Battlefield Technology Market (by Application), $Million, 2018-2024

Figure 6.3: Global Next Generation Battlefield Technology Market (Cybersecurity), $Million, 2018-2024

Figure 6.4: Global Next Generation Battlefield Technology Market (Surveillance), $Million, 2018-2024

Figure 6.5: Global Next Generation Battlefield Technology Market (Data Warfare), $Million, 2018-2024

Figure 6.6: Global Next Generation Battlefield Technology Market (Logistics and Transportation Market), $Million, 2018-2024

Figure 6.7: Global Next Generation Battlefield Technology Market (Explosive Ordinance Disposal Market), $Million, 2018-2024

Figure 6.8: Global Next Generation Battlefield Technology Market (Health Monitoring), $Million, 2018-2024

Figure 6.9: Global Next Generation Battlefield Technology Market (Combat Simulation and Training), $Million, 2018-2024

Figure 6.10: Global Next Generation Battlefield Technology Market (Others), $Million, 2018-2024

Figure 7.1: Classification of the Global Next Generation Battlefield Technology Market (by Component)

Figure 7.2: Global Next Generation Battlefield Technology Market (by Component), Value ($Million), 2018-2024

Figure 7.3: Global Next Generation Battlefield Technology Market (Hardware), $Million, 2018-2024

Figure 7.4: Global Next Generation Battlefield Technology Market (Software), $Million, 2018-2024

Figure 8.1: Classification of Global Next Generation Battlefield Technology Market (by Region)

Figure 8.2: North America Next Generation Battlefield Technology Market Value (by Country), $Million, 2018 and 2024

Figure 8.3: U.S. Defense Budget, 2017-2019

Figure 8.4: U.S. Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.5: Canada Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.6: Europe Next Generation Battlefield Technology Market Value (by Country), $Million, 2018 and 2024

Figure 8.7: U.K. Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.8: Germany Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.9: France Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.10: Russia Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.11: Italy Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.12: Rest-of-Europe Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.13: Asia-Pacific Next Generation Battlefield Technology Market (by Country), 2018 and 2024

Figure 8.14: China Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.15: India Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.16: South Korea Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.17: Japan Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.18: Australia Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.19: Rest-of-Asia-Pacific Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.20: Rest-of-the-World Next Generation Battlefield Technology Market (by Country), 2018 and 2024

Figure 8.21: Middle East and Africa Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 8.22: Latin America Next Generation Battlefield Technology Market Size, $Million, 2018-2024

Figure 9.1: BAE Systems – Product Offerings

Figure 9.2: BAE Systems - Financials, 2016-2018

Figure 9.3: BAE Systems - Business Revenue Mix, 2017-2018

Figure 9.4: BAE Systems - Region Revenue Mix, 2016-2018

Figure 9.5: BAE Systems – Research and Development Expenditure, 2016-2018

Figure 9.6: SWOT Analysis – BAE Systems

Figure 9.7: The Boeing Company – Product Offerings

Figure 9.8: The Boeing Company - Financials, 2016-2018

Figure 9.9: The Boeing Company - Business Revenue Mix, 2016-2018

Figure 9.10: The Boeing Company - Region Revenue Mix, 2016-2018

Figure 9.11: The Boeing Company – Research and Development Expenditure, 2016-2018

Figure 9.12: SWOT Analysis – The Boeing Company

Figure 9.13: Exone – Product Offerings

Figure 9.14: Exone - Financials, 2017-2018

Figure 9.15: Exone - Business Revenue Mix, 2017-2018

Figure 9.16: Exone - Region Revenue Mix, 2017-2018

Figure 9.17: Exone – Research and Development Expenditure, 2017-2018

Figure 9.18: SWOT Analysis – Exone Group

Figure 9.19: Elbit Systems – Product Offerings

Figure 9.20: Elbit Systems Ltd. - Financials, 2016-2018

Figure 9.21: Elbit Systems Ltd. - Business Revenue Mix, 2016-2018

Figure 9.22 Elbit Systems Ltd. - Region Revenue Mix, 2016-2018

Figure 9.23: Elbit Systems Ltd. - Research and Development Expenditure, 2016-2018

Figure 9.24: SWOT Analysis – Elbit Systems

Figure 9.25: Flir Systems – Product Offerings

Figure 9.26: Flir Systems Inc. - Financials, 2016-2018

Figure 9.27: Flir System Inc. - Business Revenue Mix, 2016-2018

Figure 9.28: Flir Systems Inc. - Region Revenue Mix, 2017-2018

Figure 9.29: Flir Systems Inc. - Research and Development Expenditure, 2016-2018

Figure 9.30: SWOT Analysis – Flir Systems Inc.

Figure 9.31: General Dynamics – Product Offerings

Figure 9.32: General Dynamics - Financials, 2016-2018

Figure 9.33: General Dynamics - Business Revenue Mix, 2016-2018

Figure 9.34: General Dynamics - Region Revenue Mix, 2016-2018

Figure 9.35: General Dynamics - Research and Development Expenditure, 2016-2018

Figure 9.36: SWOT Analysis – General Dynamics

Figure 9.37: HARRIS CORPORATION – Product Offerings

Figure 9.38: HARRIS CORPORATION - Financials, 2016-2018

Figure 9.39: HARRIS CORPORATION - Business Revenue Mix, 2017-2018

Figure 9.40: HARRIS CORPORATION - Region Revenue Mix, 2016-2018

Figure 9.41: HARRIS CORPORATION - Research and Development Expenditure, 2016-2018

Figure 9.42: SWOT Analysis – Harris Corporation

Figure 9.43: IBM – Product Offerings

Figure 9.44: IBM - Financials, 2016-2018

Figure 9.45: IBM - Business Revenue Mix, 2017-2018

Figure 9.46: IBM - Region Revenue Mix, 2017-2018

Figure 9.47: IBM - Research and Development Expenditure, 2016-2018

Figure 9.48: SWOT Analysis – IBM

Figure 9.49: Lockheed Martin Corporation – Product Offerings

Figure 9.50: Lockheed Martin Corporation - Financials, 2016-2018

Figure 9.51: Lockheed Martin Corporation - Business Revenue Mix, 2016-2018

Figure 9.52: Lockheed Martin Corporation - Region Revenue Mix, 2016-2018

Figure 9.53: Lockheed Martin Corporation - Research and Development Expenditure, 2016-2018

Figure 9.54: SWOT Analysis – Lockheed Martin

Figure 9.55: Leidos – Product Offerings

Figure 9.56: Leidos - Financials, 2016-2018

Figure 9.57: Leidos - Business Revenue Mix, 2016-2018

Figure 9.58: Leidos - Region Revenue Mix, 2016-2018

Figure 9.59: Leidos - Research and Development Expenditure, 2016-2018

Figure 9.60: SWOT Analysis – Leidos

Figure 9.61: Northrop Grumman Corporation: Product Offerings

Figure 9.62: Northrop Grumman Corporation - Financials, 2016-2018

Figure 9.63: Northrop Grumman Corporation - Business Revenue Mix, 2016-2018

Figure 9.64: Northrop Grumman Corporation - Region Revenue Mix, 2016-2018

Figure 9.65: Northrop Grumman Corporation – Research and Development Expenditure, 2016-2018

Figure 9.66: SWOT Analysis – Northrop Grumman Corporation

Figure 9.67: Raytheon Company – Product Offerings

Figure 9.68: Raytheon Company - Financials, 2016-2018

Figure 9.69: Raytheon Company - Business Revenue Mix, 2016-2018

Figure 9.70: Raytheon Company - Region Revenue Mix, 2016-2018

Figure 9.71: Raytheon Company – Research and Development Expenditure, 2016-2018

Figure 9.72: SWOT Analysis – Raytheon Company

Figure 9.73: Rheinmetall Group – Product Offerings

Figure 9.74: Rheinmetall Group - Financials, 2016-2018

Figure 9.75: Rheinmetall Group - Business Revenue Mix, 2016-2018

Figure 9.76: Rheinmetall Group: R&D Expenditure, 2016-2018

Figure 9.77: SWOT Analysis – Rheinmetall Group

Figure 9.78: SparkCognition – Product Offerings

Figure 9.79: SWOT Analysis – Spark Cognition

Figure 9.80: Thales Group – Product Offerings

Figure 9.81: Thales Group - Financials, 2016-2018

Figure 9.82: Thales Group - Business Revenue Mix, 2016-2018

Figure 9.83: Thales Group - Region Revenue Mix, 2016-2018

Figure 9.84: Thales Group – Research and Development Expenditure, 2016-2018

Figure 9.85: SWOT Analysis – Thales Group

Figure 10.1: Global Next Generation Battlefield Technology Market Segmentation

Figure 10.2: Next Generation Battlefield Technology Market Research Methodology

Figure 10.3: Data Triangulation

Figure 10.4: Top-Down and Bottom-up Approach

Figure 10.5: Global Next Generation Battlefield Technology Market Influencing Factors

Figure 10.6: Assumptions and Limitations

Market Overview and Estimation

In order to protect the nation from external threats, developing countries have made considerable efforts to strengthen their defense capabilities. Most of the key players are focusing on developing AI, IoT, and 3D printing equipment to enhance the military operational capability. Internet of things is considered the most valuable asset in the global next-generation battlefield technology market. The rising demand for advancement of defense forces using next generation technologies such as Internet of Things, artificial intelligence, 3D printing and wearable devices on land, sea, air, and space platforms is responsible for the growth of next generation battlefield technology market.

3D printing technology is put into application for military purposes around the world for printing prototypes, developing aircraft and other vehicles in military fablabs. In the recent past, the defense forces have deployed new learning action frameworks which use next generation technology to imitate human perception of learning, memory, and judgment. AI and Internet of Things are used by major countries, namely the U.S., Russia, and China to tackle with unknown threats during combat.

With recent developments in AI, IoT, 3D printing, and wearable devices, various equipment namely unmanned ground vehicle, unmanned marine vehicle, unmanned aerial vehicle, armored fighting vehicle, submarine, fighter jets and ships are available at a reliable cost in manufacturing industries. As the complexity of automating tasks increases, the performance of the industries is likely to decline. Hence, the manufacturing industries are likely to continue as well as increase their deployment. Thus, the impact of next generation technology is expected to grow along with improved levels of new automation technologies.

|

Growth Drivers

|

• Increasing expenditure and modernization of defense industry for developing military equipment • Rapid technological advancement in artificial intelligence and robotics |

||

|

Market Challenges

|

• Expensive development and maintenance of AI, IoT, and 3D printing-based systems • Rising cyber threat for military data |

||

|

Market Opportunities

|

• Rising adoption of AI and internet of things for military operation • Increasing demand for next-generation battlefield technologies • Manufacturing of engine and structure of military vehicles through 3d printing

|

||

Growth Factors

Modernization of Defense Industry: The increase in defense budget of various countries such as the U.S., India, Russia, China, Saudi Arabia, South Korea, and South Africa plays a major role in the defense modernization program for strengthening their defense forces. The demand for modernizing military equipment using AI, IOT and 3D printing technology is backed by the requirement for precision in the battlefield for various applications. The increased demand by the defense and security applications such as ISR, combat support, explosive ordinance disposal, and mine clearance, would impact the market for next generation battlefield technology.

Technological Advancement in Artificial Intelligence: Due to the increase in the usability of robotic devices, the demand for robotics technology across wide-ranging industry verticals has increased manifold at an exceptional growth rate. Huge technological advancements in AI, IoT and machine automation for over a decade act as the foundation for wearable devices, such as exoskeleton suits.

Cloud Services in Defense: Next-generation battlefield technology formulates new ways of efficiently accomplishing various military operations such as patrolling, defending, reconnaissance, and surveillance with high precision and low mortality. Cloud can disconnect from the global internet and run autonomously on closed transfer segment. Cloud connectivity results in quick processing and analysis of information, which might enhance the functioning of military.

Market Report Coverage - Next-Generation Battlefield Technology Market

|

|||

|

Base Year

|

2018 |

Market Size by 2019

|

$16.66 billion |

|

Forecast Period

|

2019-2024 |

Value Estimation by 2025

|

$42.12 billion |

|

CAGR During Forecast Period

|

17.02% |

Number of Tables

|

17 |

|

Number of Pages

|

300 |

|

|

|

Market Segmentation

|

• Technology - artificial intelligence, 3d printing, internet of things, and wearable devices • Application – cybersecurity, surveillance, data warfare, logistics and transportation, explosive ordinance disposal (EOD), health monitoring, combat simulation and training, and others • Component – hardware and software |

||

|

Regional Segmentation

|

North America - U.S. and Canada Europe - U.K., Germany, France, Russia, Italy, and Rest-of-Europe Asia-Pacific – China, India, South Korea, Japan, Australia, and Rest-of-Asia-Pacific Rest-of-the-World - Middle East and Africa and Latin America |

||

|

Key Companies Profiled

|

BAE Systems, The Boeing Company, Exone, Elbit Systems, FLIR Systems Inc., General Dynamics, Harris Corporation, IBM, Lockheed Martin Corporation, Leidos, Northrop Grumman Corporation, Raytheon Company, Rheinmetall Group, SparkCognition, Thales Group, Other Key Players |

||

Market Segmentation

Market Outlook by Technology

By Application

The next generation battlefield technology market (by application) includes, cybersecurity, data warfare, surveillance, logistics & transportation, explosive ordinance disposal, healthcare monitoring, and combat stimulation. Explosive ordinance disposal segment dominated the global next generation battlefield technology market with a market share of approximately 28.00% in 2018. However, the cybersecurity segment is anticipated to emerge as a second dominant segment in application by 2024 growing at a significant double digit CAGR during the forecast period.

By Component

The global next generation battlefield technology, by component includes hardware and software segment. The software segment dominated the global next generation battlefield technology market in 2018. The market is expected to grow significantly during the forecast period. Software services hold major market share in 2018 and are expected to drive the growth of the global next generation battlefield technology market from 2019 to 2024. The growth of the software segment is attributed to the high adoption of technically advanced software for military purposes.

By Region

The next generation battlefield technology market has witnessed different market dynamics across various regions of the globe. Moreover, the next generation battlefield technology manufacturing companies have witnessed rising demand from countries such as China, the U.K. and the U.S. The growth of the region is mainly driven by the increasing focus of nations such as the U.S. and Canada on adopting next generation technology such as artificial intelligence, IoT, 3D printing and wearable device to cope with the shrinking workforce due to the increasing ratio of aged population.

Focus on Technology, Application, and Component

The Global Military Artificial Intelligence Market report by BIS Research projects the market...

The global satellite M2M and IoT network market generated $617.3 million in 2017 and is...

1. Please contact us to discuss customization options, and we can confirm the time and cost (if any). For minor customization requirements that would take 3-5 days, we do not charge any additional amount.

2. All BIS Research reports are delivered to clients via our InsightMonk platform. This allows the customers to extract the data in Excel for their use. Excel is provided for all License types and is not limited to just enterprise users.

3. Additionally, all customers also get access to the following complimentary value-added services from BIS Research.

*Expert Consultation Charges applicable