Published Year: 2025

Precision Agriculture Market - A Global and Regional Analysis: Focus on Application, Product, and Re

The global precision agriculture market is projected to reach $22.49 billion by 2034 from...

Focus on Market by Crop Type, Deployment Type, and Region - Analysis and Forecast, 2025-2035

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know MoreThe precision planting market is growing at a pace mainly due to the heightened demand for global food production and the sharp rise in seed costs, driving adoption. The rising global population, expected to be near 10 billion by 2050, intensifies the need for increased agricultural output without expanding farmland, making precision planting technologies essential. Precision and multi-hybrid planters optimize seed depth and spacing to improve germination and yield, while adapting seed varieties to soil variability enhances resilience in diverse fields. For instance, in October 2024, China launched a five-year action plan to digitize its agricultural industry, aiming to enhance domestic food production. The plan focuses on establishing a digital planting technology framework and a national agricultural big data platform by 2028.

However, even after increasing applications, the market growth has been hampered by certain factors such as the lack of awareness and infrastructure in developing regions and the high cost of implementing precision planting solutions. The lack of awareness and insufficient infrastructure in developing regions significantly challenge the adoption and deployment of precision planting technologies, thereby impeding market growth and technology penetration. The high cost of implementing precision planting solutions presents a significant market challenge that directly constrains adoption and growth across key deployment technologies.

Market Overview

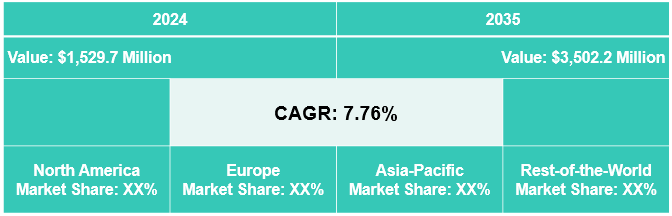

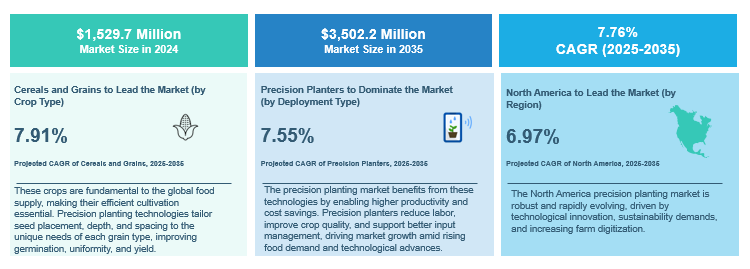

The precision planting market’s revenue was $1,529.7 million in 2024, and it is expected to reach $3,502.2 million by 2035, advancing at a CAGR of 7.76% during the forecast period (2025-2035). The market is growing because farmers are under increasing pressure to maximize yields, reduce input costs, and comply with sustainability targets. Rising seed and fertilizer prices make precise, row-by-row planting more economically attractive, while government policies in North America, Europe, and emerging markets are pushing for higher resource efficiency and lower carbon emissions. At the same time, rapid advances in sensors, GPS, telematics, and AI-driven agronomic analytics are making precision planting more reliable, user-friendly, and adaptable across farm sizes. This convergence of economic necessity, regulatory support, and technological maturity is driving adoption, especially in large-scale row crops such as corn, soybeans, and wheat.

Market Snapshot

Industrial Impact

The industrial impact on the precision planting market is significant because the technology is reshaping traditional farm machinery manufacturing and the ag equipment value chain. OEMs such as John Deere, CNH Industrial, and AGCO are investing heavily in integrating precision hardware and software into planters, creating new recurring revenue streams through retrofit kits, data subscriptions, and after-sales service. This shift is driving consolidation in the equipment industry, as larger players acquire specialized tech firms (e.g., AGCO’s Precision Planting) to stay competitive. It also pushes suppliers of sensors, hydraulics, and control systems to upgrade their offerings to meet the accuracy and reliability demands of precision planting.

At the same time, the rise of precision planting is stimulating broader industrial innovation and ecosystem integration. Ag-tech startups and drone-based seeding firms are finding industrial partners to commercialize niche technologies, while big equipment makers are collaborating with satellite and data analytics companies to build full-stack planting solutions. The industry-wide push toward digitalization and electrification is also aligning with precision planting systems, since data-driven planting supports automation and eventually autonomous machinery. Collectively, these industrial dynamics are making precision planting not just a farming practice but a strategic growth driver for the entire agricultural machinery and ag-tech industries.

Market Segmentation

Segmentation 1: by Crop Type

• Cereals and Grains

• Oilseeds and Pulses

• Fruits and Vegetables

• Others

Cereals and Grains to Lead the Market (by Crop Type)

The cereals and grains segment dominates the market. These crops are fundamental to the global food supply, making their efficient cultivation essential. Precision planting technologies tailor seed placement, depth, and spacing to the unique needs of each grain type, improving germination, uniformity, and yield.

The precision planting market benefits from this segment’s growth, driven by rising food demand, sustainability goals, and economic significance. Accurate planting reduces seed waste and enhances crop performance, positioning cereals and grains as key drivers for precision agriculture adoption and innovation.

Segmentation 2: by Deployment Type

• Precision Planters

• Planting Retrofit Kits

• Autonomous Planting Systems

• Drone-Based Seeding Systems

Precision Planters to Dominate the Market (by Deployment Type)

Precision planters are advanced machines designed to optimize seed placement, depth, and spacing, ensuring uniform crop emergence and maximizing yield. Equipped with GPS, sensors, and automation, they adapt to soil and crop conditions, enhancing planting accuracy and reducing seed waste. This improves resource efficiency and promotes sustainable farming.

The precision planting market benefits from these technologies by enabling higher productivity and cost savings. Precision planters reduce labor, improve crop quality, and support better input management, driving market growth amid rising food demand and technological advances.

Segmentation 3: by Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

North America to Lead the Market (by Region)

North America is the leader in the market. This is because the rising adoption of GPS technology and data analytics facilitates improved crop management and resource efficiency, enabling farmers to make informed decisions, as seen in widespread GPS use in regions such as Ontario. Also, AGCO’s acquisition of Trimble’s agricultural assets (September 2023) creates a robust mixed-fleet precision ag platform, expanding technology accessibility across multiple equipment brands and driving market growth.

The North America precision planting market is robust and rapidly evolving, driven by technological innovation, sustainability demands, and increasing farm digitization. For instance, leading companies such as AGCO, John Deere, and Trimble have been developing integrated solutions that enhance crop productivity and resource efficiency across a range of farm sizes. The region benefits from strong agritech ecosystems, significant investments in AI, autonomous machinery, and data analytics, while facing challenges such as infrastructure disparities and regulatory complexities. These dynamics position North America as a global leader in precision agriculture, fostering sustainable and efficient farming practices.

Recent Developments in the Precision Planting Market

• In 2023, AGCO’s strategic joint venture with Trimble significantly expanded North America’s mixed-fleet precision ag capabilities, aiming to surpass $2 billion in revenue by 2028. Additionally, innovations such as Väderstad’s introduction of high-speed Tempo planters in June 2024 and Precision AI’s autonomous herbicide application drones highlight ongoing efforts to improve efficiency and reduce chemical usage.

• In 2023, Canadian startup Precision AI developed autonomous drones capable of plant-level herbicide application, significantly reducing chemical overspend and labor dependency. This breakthrough reflects Canada’s growing emphasis on leveraging cutting-edge technology to address challenges such as labor shortages and environmental impact in agriculture.

• In 2023, a German study identified the Robotti LR and Robotti 150 D field robots as highly effective for potato cultivation, offering autonomous driving, spraying, and mechanical weed control capabilities that enhance efficiency and reduce chemical use by up to 25%.

• In 2024, BoomGrow partnered with CelcomDigi to leverage 5G and AI for real-time monitoring and precision control in Malaysian farms. Similarly, Indonesia’s Elevarm secured $4.25 million in March 2025 to expand AI-powered farming solutions targeting smallholder farmers.

Analyst’s Thoughts

According to Dhrubajyoti, Principal Analyst at BIS Research, “From an analyst perspective, the precision planting market is moving from an early adoption phase into mainstream deployment, particularly in developed agricultural economies. The market is underpinned by structural drivers such as rising input costs, shrinking arable land, and the pressure to improve farm productivity with fewer resources. Leading OEMs and technology providers are leveraging their scale to lock farmers into integrated ecosystems that combine hardware (planters, meters, sensors) with digital platforms for data analytics and prescriptive recommendations. This creates a dual revenue model, equipment sales plus recurring digital services, which strengthens margins and deepens customer dependence. Analysts view this as a clear competitive advantage for early movers such as John Deere, AGCO, and CNH Industrial, which are likely to consolidate even greater market share over the medium term.”

Focus on Market by Crop Type, Deployment Type, and Region - Analysis and Forecast, 2025-2035

Precision planting systems refers to the specialized machinery and attachments, such as high-speed planters, seed meters, seed tubes, downforce control systems, variable-rate drives, and row-by-row monitoring units, designed to ensure accurate seed placement, depth, and spacing while optimizing fertilizer and input application during planting. The types of precision planting systems available in the market are precision planters, planting retrofit kits, autonomous planting systems, and drone-based seeding systems.

Companies in the precision planting market have been focusing on offering advanced solutions and investing in their development. Companies operating in the precision planting market are employing a combination of product launches, technology innovation, ecosystem integration, and strategic partnerships to strengthen their competitive position.

A new company entering the precision planting market should focus on niche innovation and differentiation rather than competing directly with large OEMs. The most promising areas include developing retrofit kits that can upgrade existing planters, building AI-driven analytics platforms for real-time seeding decisions, designing low-cost and rugged solutions for smallholder farms in emerging markets, and ensuring interoperability across multiple brands and digital platforms to avoid vendor lock-in. Additionally, integrating sustainability features such as reduced seed wastage, optimized fertilizer use, and carbon-smart planting practices can align with regulatory incentives and farmer demand. By targeting these areas, a new entrant can capture market share through affordability, flexibility, and sustainability-led innovation.

The precision planting market was valued at $1,529.7 million in 2024 and is expected to grow at a CAGR of 7.76%, reaching $3,502.2 million by 2035.

Major trends in the precision planting market include the increased need for workforce mechanization for better crop yield and the rapid adoption of smart sensor technology in the precision agriculture landscape. Drivers include the growth of heightened demand for global food production and the sharp rise in seed costs, driving adoption.

Despite its promise, the precision planting market faces several challenges. These include the lack of awareness and infrastructure in developing regions and the high cost of implementing precision planting solutions.

The precision planting market presents strong growth opportunities, particularly in regions seeking affordable and scalable agritech solutions. Major opportunities in the market include the adoption of precision planting in specialty and high-value crops and the gaining traction of drone technology.

The report’s unique selling propositions (USPs) lie in its comprehensive segmentation of the precision planting market by crop type and deployment type. It offers a thorough analysis of key trends, market drivers, and challenges across major countries, including the U.S., China, India, Germany, France, and the U.K., along with country-level forecasts and policy insights. The study also features detailed profiles of leading precision planting systems companies and emerging startups, supported by expert analysis highlighting innovation hubs and untapped revenue opportunities. Additionally, it provides strategic guidance to help organizations enhance their competitive positioning and navigate the evolving market landscape.

Agricultural equipment manufacturers, agribusinesses and farmers, precision Ag technology providers, government entities and policymakers, financial institutions and investors, agricultural consultants and advisory services, and R&D institutions should consider this report. It is particularly valuable for stakeholders seeking to understand the evolving landscape of the precision planting market and identify growth opportunities, strategic partnerships, and areas for technology investment.

The global precision agriculture market is projected to reach $22.49 billion by 2034 from...