A quick peek into the report

Global Proteomics Market: Industry Overview

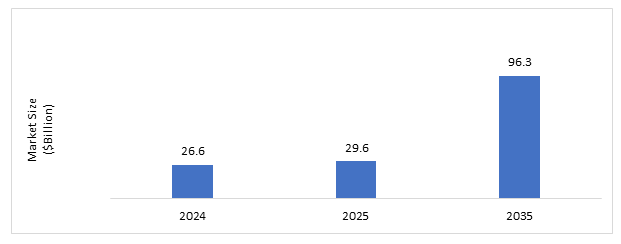

The global proteomics market was valued at approximately $29.60 billion in 2025 and is projected to grow $96.28 billion by 2035, at a CAGR of around 12.52%. The global proteomics market is witnessing accelerated growth driven by the rising prevalence of chronic and neurodegenerative diseases, continuous technological advancements, and the increasing demand for personalized medicine. Proteomics has emerged as a transformative field, enabling in-depth analysis of protein structures, functions, and interactions, which are critical for understanding disease mechanisms and developing targeted therapies. The integration of artificial intelligence, machine learning, and multi-omics platforms is revolutionizing the proteomics workflow, from biomarker discovery to clinical translation, by enabling faster, more accurate, and cost-effective analyses. AI-enabled systems are streamlining data interpretation, uncovering complex protein interaction networks, and facilitating early disease detection through predictive modeling.

Moreover, autonomous discovery platforms and generative AI tools are empowering researchers to perform iterative design, test, and optimize cycles with minimal human intervention, accelerating drug discovery and diagnostics. Pharmaceutical, biotechnology, and contract research organizations are increasingly collaborating with AI-driven startups and technology providers to enhance scalability, improve data integration, and enable precision-driven insights. Strategic partnerships, funding initiatives, and mergers are strengthening the commercialization of advanced proteomic platforms, while cloud-based and on-premise solutions are expanding accessibility across research and clinical settings. Collectively, these factors are reshaping the global proteomics landscape, improving research productivity, and positioning the market for sustained long-term growth.

Global Proteomics Market Lifecycle Stage

The global proteomics market currently stands at the growth and acceleration stage of its lifecycle, transitioning from early adoption toward broader market maturity. Over the past decade, the field has evolved from academic and exploratory research into a strategically critical component of precision medicine, clinical diagnostics, and drug discovery. This shift has been fueled by rapid advancements in mass spectrometry, liquid chromatography, and affinity-based proteomic platforms, alongside the integration of artificial intelligence, machine learning, and multi-omics analytics.

The expansion of the global proteomics market is underpinned by a robust convergence of technological innovation and clinical utility. Continuous improvements in data-independent acquisition (DIA) methods, single-cell and spatial proteomics, and bioinformatics pipelines are enabling high-throughput, high-sensitivity protein profiling. At the same time, commercial players are scaling platform accessibility through automation, cloud-enabled analytics, and service-based delivery models. These trends indicate strong forward momentum as proteomics moves beyond research applications into clinical and translational domains.

While the market exhibits high innovation intensity, its penetration remains uneven across regions and end-user segments. Developed markets in North America and Europe demonstrate near-mainstream adoption within pharma, biotech, and academic research ecosystems. Conversely, adoption in emerging regions is still in its early growth phase, constrained by high capital costs, infrastructure gaps, and limited skilled personnel. This bifurcation positions the market globally within a mid-to-late growth phase, with significant opportunities for expansion through affordable instrumentation, service partnerships, and decentralized proteomic networks.

In summary, the global proteomics market is in a dynamic growth stage, characterized by technological disruption, capital inflows, and expanding end-user adoption. Over the next few years, the industry is expected to move toward early maturity, with broader clinical integration, standardization of workflows, and consolidation among technology providers.

Figure: Global Proteomics Market Snapshot

Market Segmentation:

Segmentation 1: By Offering

• Sample Preparation

• Proteomics Technologies

o Reagents and Consumables

o Instruments

o Software

• Proteomics Services

Proteomics technologies segment is expected to account for the largest share of the global proteomics market. This can be attributed to the widespread adoption of advanced analytical platforms, including mass spectrometry, chromatography systems, and specialized software, which are fundamental to conducting high-throughput and high-resolution proteomic analyses. The continuous innovation in instrumentation, growing demand for platform-specific reagents, and increasing integration of AI and cloud-based tools have further strengthened the dominance of this segment. Additionally, the high capital investment associated with proteomic technologies contributes significantly to overall market value.

Segmentation 2: By Technology

• Mass Spectrometry-Based Proteomics

• Chromatography-Based Proteomics

• Protein Microarrays

• Single-Cell Proteomics

• NGS-Based Proteomics

• Others

Based on technology, mass spectrometry-based proteomics is expected to dominate the global proteomics market in 2024. This is primarily due to its unmatched sensitivity, accuracy, and versatility in identifying and quantifying proteins across diverse biological samples. Mass spectrometry has become the gold standard in proteomic research owing to its ability to support both discovery and targeted workflows, detect post-translational modifications, and handle complex sample matrices. Its integration into clinical and translational research has further expanded its adoption across pharmaceutical, academic, and diagnostic settings.

Segmentation 3: By Application

• Biomarker Discovery and Validation

• Proteome Profiling and Mapping

• Drug Discovery and Development

o Discovery

o Preclinical

o Clinical

• Companion Diagnostics

• Protein-Protein Interactions

In 2024, biomarker discovery and validation segment is projected to hold the largest share of the global proteomics market. This dominance is driven by its wide usage across multiple therapeutic areas, integral to precision medicine, and heavily funded for its role in early-stage research, diagnostics, and drug development. Its broad applicability and reliance on diverse proteomics technologies make it the most in-demand application

Segmentation 4: By End User

• Academic and Research Institutions

• Pharmaceutical and Biotechnology Companies

• Clinical Diagnostic Laboratory & Hospitals

• Contract Research Organizations

Based on end-user segmentation, academic and research institutions are expected to account for the largest share of the global proteomics market in 2024. This is primarily driven by the high volume of basic and translational research activities conducted in universities, government-funded laboratories, and public research centers. These institutions are at the forefront of exploring novel proteomic methodologies, biomarker discovery, and systems biology, often supported by significant public and private funding. Additionally, the availability of advanced infrastructure, collaborations with industry players, and a strong focus on innovation have positioned academic and research institutions as key drivers of proteomics adoption globally.

Segmentation 5: By Region

• North America

• Europe

• Asia-Pacific

• Latin America

• Middle East and Africa

Based on region, North America is expected to hold the largest share of the global proteomics market in 2024, accounting for 44.69%. This dominance is attributed to the region's well-established research infrastructure, strong presence of key market players, high investment in life sciences R&D, and widespread adoption of advanced proteomic technologies in both academic and clinical settings. Meanwhile, Asia-Pacific is projected to be the fastest-growing region during the forecast period (2025–2035), with a CAGR of 13.86%, driven by increasing government funding for biomedical research, rapid expansion of healthcare infrastructure, growing focus on precision medicine, and a rising number of collaborations between global companies and regional research institutions.

Demand – Drivers and Limitations

Demand Drivers for the Global Proteomics Market:

• Rising Prevalence of Chronic Diseases

• Continuous Technological Advancements

• Increasing Demand for Personalized Medicine

Limitations for the Global Proteomics Market:

• High Costs of Acquisition Hindering the Adoption of Proteomics Technologies

• Shortage of Skilled Professionals

Proteomics Market - A Global and Regional Analysis

Focus on Offering, Technology, Application, End User, and Regional Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Proteomics is the large-scale study of proteins, which are the functional building blocks of all biological processes. It involves identifying, quantifying, and analyzing the structure, function, and interactions of proteins within cells, tissues, or organisms. By mapping the entire protein complement of the genome, known as the proteome, scientists can better understand disease mechanisms, discover biomarkers, and develop targeted therapies. Modern proteomics relies heavily on advanced technologies such as mass spectrometry, liquid chromatography, and bioinformatics tools to achieve precise and high-throughput protein characterization.

The growth of the global proteomics market is primarily driven by the rising prevalence of chronic and neurodegenerative diseases, continuous technological advancements, and the increasing demand for personalized medicine. With non-communicable diseases accounting for 75% of global deaths, there is a growing need for early detection and precision diagnostics, where proteomics plays a critical role by identifying disease-specific biomarkers and monitoring disease progression. Technological innovations, including high-resolution mass spectrometry, single-cell and spatial proteomics, and AI-enabled bioinformatics platforms, are expanding analytical capabilities, improving throughput, and reducing costs. Additionally, proteomics supports the development of personalized treatment approaches by enabling detailed molecular profiling, target identification, and drug response prediction. As healthcare systems shift toward precision medicine and data-driven decision-making, proteomics continues to gain traction as a cornerstone technology in both research and clinical applications.

Despite its strong growth potential, the global proteomics market faces several key challenges. The high cost of advanced instrumentation, particularly mass spectrometry systems, remains a major barrier to adoption, especially among smaller academic and research institutions. These instruments can cost between $400,000 and $1.5 million, excluding recurring expenses for maintenance, consumables, and software. Furthermore, the rapid pace of technological innovation often leads to concerns about obsolescence, making it difficult for laboratories to keep up with new advancements. Another major challenge is the shortage of skilled professionals trained in complex proteomic techniques and data interpretation. The demand for expertise in mass spectrometry, bioinformatics, and computational biology is outpacing supply, leading to operational bottlenecks and higher labor costs. Together, these challenges limit the broader adoption of proteomics technologies, particularly in emerging economies, and highlight the need for cost-effective solutions, workforce training programs, and automation-driven workflows to sustain long-term market growth.

This report offers a comprehensive, end-to-end analysis of the global proteomics market, combining market sizing, growth forecasts, competitive intelligence, and technology insights. It emphasizes emerging innovations, including AI integration. In addition, the report includes extensive company profiling, benchmarking, funding analysis, partnership tracking, patent analysis, equipping stakeholders with actionable insights for strategic decision-making. Its value lies in integrating technological developments with commercial and competitive intelligence, supporting informed choices regarding R&D prioritization, market entry, and partnership strategies.

This report is intended for stakeholders across the life sciences, biotechnology, and healthcare sectors who seek to understand emerging opportunities, technological innovations, and competitive developments within the global proteomics market. It provides critical insights for pharmaceutical and biotechnology companies integrating proteomics into drug discovery, biomarker development, and personalized medicine initiatives. Manufacturers of life science tools and platforms, including those specializing in mass spectrometry, chromatography, and bioinformatics, will find valuable insights on market expansion, product innovation, and adoption trends. Contract research organizations and academic institutions can leverage the report to identify collaboration opportunities and optimize proteomics-based research strategies. Additionally, investors and venture capital firms will benefit from understanding high-growth segments, emerging startups, and commercialization potential across AI-driven and single-cell proteomics. Overall, the report serves as a comprehensive guide for organizations seeking to align R&D strategies, make informed investment decisions, and strengthen their competitive position in the evolving global proteomics landscape.