A quick peek into the report

Introduction of Soil Health and Regenerative Agriculture Market

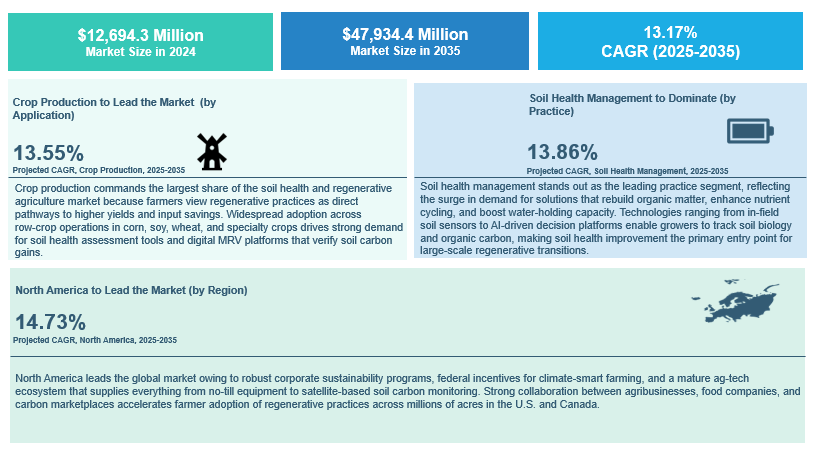

The soil health and regenerative agriculture market encompasses a broad range of soil health management solutions and regenerative agriculture practices aimed at restoring soil fertility, biodiversity, and farm resilience. Around the world, farmers and agribusinesses are adopting methods like cover cropping, crop rotation, conservation tillage techniques (including no-till farming advantages), and agroforestry to rebuild soil structure and sequester carbon. These changes are driven by the proven cover cropping benefits (improved soil cover, nutrient retention) and the yield stability gained from crop rotation for soil health. In addition, emerging soil carbon sequestration strategies, from planting deep-rooted perennials to applying biochar, are enabling farmers to capture value through carbon farming credits. According to BIS Research analysis, this market is set for robust growth, with global sustainability initiatives and corporate net-zero commitments fueling investment. The market was valued at approximately $12,694.3 million in 2024 and is projected to reach over $47,934.4 million by 2035 reflecting strong double-digit expansion. As a result, the soil health and regenerative agriculture sector is rapidly evolving from niche experiments into a mainstream paradigm for low-carbon agriculture practices and climate-resilient food production.

Market Introduction

The soil health and regenerative agriculture market encompasses a wide spectrum of soil health management solutions, ranging from cover cropping programs and no-till equipment to AI-powered soil carbon monitoring platforms. Farmers, agribusinesses, and food companies adopt these regenerative agriculture practices to rebuild soil organic matter, boost biodiversity, and secure soil carbon sequestration credits that strengthen sustainability portfolios. Market growth is fueled by rising corporate net-zero targets, government incentives for low-carbon agriculture practices, and investor interest in agricultural carbon credit markets. Leading players, such as Bayer, Indigo?Ag, Nutrien, and Agreena, are advancing innovative products, including microbial biofertilizers, satellite-based digital MRV for agriculture, and integrated regenerative ag tech platforms. With global demand for climate-smart food production mounting, the soil health and regenerative agriculture market is evolving quickly to meet productivity, resilience, and emission reduction goals across worldwide crop and livestock systems.

Industrial Impact

Regenerative agriculture is transforming conventional farming by emphasizing ecological and climate-smart approaches. Widespread adoption of low-carbon agriculture practices, such as integrating legumes for natural nitrogen fixation and using water-efficient agriculture practices (e.g., drip irrigation coupled with healthy soils), has a significant industrial impact. Food and beverage corporations are increasingly supporting these practices to achieve scope-3 emission reduction in agriculture supply chains, effectively turning farms into carbon sinks. Likewise, governments worldwide are introducing climate-smart agriculture policies and incentive programs to promote soil regeneration, given its benefits for long-term agricultural productivity and environmental health. The ripple effects span across the agritech and sustainability sectors; agribusiness giants are developing sustainable farming business models that reward regenerative outcomes (e.g., paying growers for soil carbon gains), and new markets are forming around soil carbon trading. The push for healthier soils is also sparking innovation in farm management; for example, advanced equipment and input suppliers now tailor products for nutrient management in regenerative farming, such as biofertilizers and no-till seeders. Overall, regenerative agriculture is not only enhancing farm profitability and biodiversity enhancement farming (by creating more diverse and resilient agro-ecosystems) but also shaping a new value chain where agricultural carbon-credit market mechanisms turn sustainable practices into financial opportunities.

Market Segmentation:

Segmentation 1: by Application

• Crop Production

• Livestock Grazing

• Forestry

Segmentation 2: by Practice Type

• Soil Health Management

• Water Management

• Biodiversity Enhancement

• Nutrient Management

• Livestock Grazing Management

Segmentation 3: by Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

Recent Developments in the soil health and regenerative agriculture market

• Bayer’s ForwardFarm Initiative (Sep 2024): Global agrochemical leader Bayer introduced a regenerative agriculture program in India focusing on soil carbon capture and vermicomposting. This initiative applied cover cropping and organic amendments to enhance soil health and climate resilience for smallholder farmers, signaling increased corporate investment in regenerative methods.

• Soil Capital Funding (Sep 2024): Belgium-based startup Soil Capital secured $16.2 million in Series B funding to scale its regenerative agriculture platform. This investment will help over a thousand European farms adopt practices like agroforestry and no-till, improving sustainability metrics (e.g., GHG emissions reduction and soil health scores) while connecting farmers to carbon farming credits.

• Emerging MRV Technologies (2025): Agri-tech companies are launching satellite monitoring soil carbon services and digital MRV for agriculture tools that use remote sensing and AI to measure soil carbon changes across large land areas. For instance, new platforms combine satellite imagery with on-ground soil sampling to verify carbon sequestration, making participation in the agricultural carbon-credit market more accessible and credible for farmers.

• Policy Incentives: Governments in regions such as the EU, Australia, and the U.S. have rolled out incentives and pilot programs encouraging regenerative practices. From payments for water-efficient agriculture practices (to conserve groundwater) to tax credits for carbon sequestration on farms, these climate-smart agriculture policies are creating a more favorable economic environment for regenerative agriculture. Notably, in 2025, the U.S. Farm Bill introduced provisions supporting soil health initiatives and climate-smart farming, likely accelerating market growth in North America.

Analyst’s Thoughts

According to Debraj Chakraborty, Principal Analyst at BIS Research, “the soil health and regenerative agriculture market is experiencing robust growth, driven by global sustainability goals and evolving climate-smart agriculture policies. There is a surging demand for carbon farming credits as companies and governments incentivize farmers to adopt regenerative agriculture practices for both environmental and supply chain benefits. Innovations such as precision agriculture for soil health and AI-powered regenerative farming platforms are significantly improving how farmers implement and monitor these practices, from tracking soil health index metrics in real time to optimizing soil carbon sequestration strategies across diverse landscapes. As these technologies mature and awareness grows, regenerative agriculture is set to move firmly into the mainstream, revolutionizing how we think about farm productivity and climate resilience.”

Soil Health and Regenerative Agriculture Market - A Global and Regional Analysis

Focus on Market Opportunities, Business Strategies, Application, Product, and Regional Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

The soil health and regenerative agriculture market refers to the industry focused on farming methods and products that restore soil quality and ecosystem function. It encompasses a range of sustainable agricultural practices designed to improve soil health, such as cover cropping, reduced or no-till farming, diverse crop rotations, agroforestry (integrating trees), use of organic compost/fertilizers, and managed grazing of livestock. These practices rebuild soil organic matter, enhance biodiversity, and increase water retention, making agriculture more sustainable and climate-resilient. Businesses in this market provide the inputs, technologies, and services that enable farmers to adopt these regenerative techniques at scale.

A mix of established agribusinesses and innovative startups is driving this market. On the corporate side, many leading food and agriculture companies have set ambitious regenerative targets; for example, PepsiCo, Nestlé, Danone, General Mills, Cargill, and Unilever are all investing in programs to expand regenerative practices across their supply chains. Traditional input providers like Bayer and Syngenta are developing bio-based soil amendments and farmer advisory services to support soil health. At the same time, ag-tech startups and platforms play a crucial role. Companies such as Indigo Ag, Agreena, Boomitra, and Nori have built platforms to measure soil carbon and connect farmers to carbon credit buyers. Other tech innovators like Pivot Bio and Locus Agricultural Solutions offer regenerative inputs (e.g., microbial fertilizers) to reduce reliance on chemicals. This ecosystem of players, from global corporations to niche tech firms, is collectively pushing the adoption of regenerative agriculture worldwide.

Several powerful drivers are fueling growth in this market. First, there is increasing support from governments and international organizations to promote regenrative farming – new policies, grants, and pilot programs incentivize practices that improve soil health and lower agriculture’s carbon footprint For example, conservation initiatives (like USDA programs or India’s BPKP) encourage cover cropping, organic inputs, and other regenerative methods. Second, the urgency of climate change is prompting companies and farmers to seek solutions that sequester carbon and reduce emissions. Major food corporations have made public commitments to source ingredients from regenerative systems and are investing billions accordingly. This corporate sustainability push, along with rising consumer demand for eco-friendly products, is driving the adoption of regenerative practices as a way to meet ESG goals. Finally, the on-the-ground benefits to farmers act as a driver; many producers report improved yields and profitability over time due to healthier soils (for instance, saving on fertilizer costs and buffering against drought), which encourages more farms to transition once success stories spread. These combined factors, i.e., policy support, climate and consumer pressure, and positive farm economics, are propelling the regenerative agriculture market forward.

Despite the momentum, the regenerative agriculture market faces a number of challenges and barriers to wider adoption. One major challenge is the knowledge and risk gap for farmers; many growers are unfamiliar with regenerative techniques or worry about potential short-term yield impacts, and learning new practices requires time and support. Changing decades-old farming habits can be difficult without clear evidence of success and technical guidance, so a lack of awareness and training remains a hurdle. Economic and market challenges also play a role. During the transition period, farmers may incur additional costs (for new equipment or cover crop seeds), and it can take a few years to see full soil improvements, which strains those with tight margins. Moreover, the broader food supply chain is not yet fully geared to reward regenerative practices; there are limited price premiums for regen-grown products, and insufficient infrastructure to segregate, process, and market crops from regenerative farms. This means farmers often don’t get paid more for sustainable methods, reducing the financial incentive. Finally, measuring and verifying soil health outcomes (like soil carbon gains) can be complex, leading to skepticism in carbon credit markets and among some stakeholders. Overcoming these challenges will require increased education, robust demonstration of long-term benefits, improved financing (e.g., transitional loans or subsidies), and better market mechanisms to reward regenerative outcomes.

New technologies are playing a pivotal role in scaling up regenerative agriculture by making it easier to monitor and manage soil health improvements. Remote sensing and AI are game-changers; satellites and drones equipped with advanced sensors can now detect cover crops from space, monitor field vegetation off-season, and even distinguish tillage practices by analyzing spectral images. This digital MRV capability allows for cost-effective verification of farmers’ practices across large areas, which is crucial for carbon credit programs and supply chain reporting. On the farm level, precision agriculture tools and IoT sensors help farmers implement regenerative techniques more effectively. For example, soil moisture sensors and smart irrigation systems ensure efficient water use (supporting cover crops in dry periods), while drone-based crop imaging can guide targeted cover crop planting or track grazing patterns. Data analytics platforms (often smartphone or cloud-based) aggregate field data and provide decision support, from recommending the optimal cover crop mix for a given soil to modeling the carbon sequestration from switching to no-till. Additionally, biotechnologies are enabling regenerative inputs; companies now offer microbial seed coatings and biofertilizers that naturally enhance soil nutrient cycling, reducing the need for synthetic fertilizers. These technologies, spanning big data, AI, biotech, and farm automation, reduce the uncertainty and labor of regenerative farming, thereby accelerating its adoption.

Carbon credits have become an integral part of the regenerative agriculture landscape by financially rewarding farmers for improving their soil. When farmers adopt practices like planting cover crops, reducing tillage, or diversifying rotations, they not only boost soil health but also sequester carbon in soil and reduce greenhouse gas emissions. These environmental benefits can be quantified and verified to generate carbon credits under standards such as Verra or the Climate Action Reserve. In practice, a number of programs and startups help translate regenerative practices into marketable credits. For example, Indigo Ag’s carbon farming program has enrolled about 1,000 farms (over 7?million acres) and issued credits for nearly 1?million tons of CO? removed; notably, tech giants like Microsoft have purchased tens of thousands of these soil carbon credits to offset their emissions. Similarly, platforms like AgreenaCarbon and Nori enable farmers to earn revenue through verified carbon offsets, using remote sensing and AI to measure soil carbon changes with high accuracy. The integration works as a cycle; farmers implement regenerative practices, digital MRV tools monitor the carbon outcome, credits are issued and sold to companies seeking offsets, and farmers receive payments. This not only provides an extra income stream for farmers (incentivizing regenerative methods) but also ties regenerative agriculture into corporate climate strategies by supplying credible nature-based carbon removals.

Regenerative agriculture is a cornerstone of climate-smart agriculture because it delivers both mitigation of climate change and adaptation benefits on the farm. On the mitigation side, regenerative practices actively reduce net greenhouse gas emissions. They increase the carbon sequestration in soils; for instance, restoring soil organic matter through cover crops and no-till can draw down significant CO? from the atmosphere and store it underground. They also cut emissions by lowering dependence on synthetic fertilizers (thereby reducing nitrous oxide release) and fossil-fuel-intensive farming. A recent analysis estimated that adopting regenerative methods like diverse rotations, cover cropping, and low tillage across the U.S. Corn Belt could cut nitrous oxide emissions by the equivalent of 4?million tons of CO? per year, akin to removing ~1?million cars from the road. In addition to mitigation, regenerative agriculture greatly improves climate resilience, helping farms adapt to a changing climate. Healthier soils have higher water-holding capacity and better structure, which means crops are more resilient to droughts and floods. In fact, studies have found that during drought years, fields managed regeneratively (with rich soil organic matter and cover crops) can outperform neighboring conventional fields in yield. By protecting against erosion, enhancing biodiversity, and creating more robust agro-ecosystems, regenerative practices buffer farmers against extreme weather and shifting climate patterns. In summary, regenerative agriculture aligns perfectly with climate-smart goals by reducing emissions, sequestering carbon, and building adaptive capacity in farming systems, all while sustaining productivity.

The market outlook for soil health and regenerative agriculture is extremely promising. Industry analysts project robust growth in the coming decade as regenerative practices move from niche to mainstream. Globally, the regenerative agriculture market was valued at around $XX in 2024 and is forecasted to reach $47 billion by 2035, reflecting a strong CAGR on the order of 13.17%. This growth trajectory is driven by expanding corporate sustainability initiatives, continued government support (including potential climate-smart subsidies), and the proven long-term benefits to farm profitability. We expect to see regenerative methods scaling rapidly, new entrants offering innovative solutions, and more capital (private and public) flowing into this space. Who should use this report? Given this outlook, a wide range of stakeholders will find value in the report’s insights. Agribusiness companies (e.g., fertilizer and seed producers, farm equipment firms) can use it to identify opportunities for regenerative product lines and services. Ag-tech startups and digital platform providers will benefit from market trends and the competitive landscape to refine their strategies. Food and beverage companies and retailers aiming for sustainable sourcing can leverage the report to understand supply chain impacts and potential partners. Carbon market participants and investors will gain perspective on the monetization of soil carbon and emerging business models in regenerative agriculture. Additionally, policymakers, NGOs, and research institutions focused on climate-smart agriculture can use the report to inform programs and identify gaps. In essence, anyone vested in the future of sustainable farming, from corporate strategists and product managers to sustainability consultants and agricultural financiers, should use this report to navigate the evolving regenerative agriculture market with confidence.