Published Year: 2022

Space Situational Awareness (SSA) Services Market - An Analysis of Debris Mitigation, Domain Awarene

The global space situational awareness services market was valued at $125.2 million in 2021,...

Focus on Application, End User, Capability, and Country - Analysis and Forecast, 2022-2032

Delivery Time: 1-5 Working Days

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know MoreSpace In-Orbit Refueling Market Overview

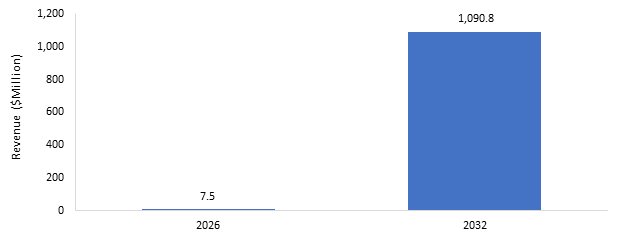

The global space in-orbit refueling market is estimated to reach $1,090.8 million by 2032 at a compound annual growth rate (CAGR) of 103.85% during the forecast period 2022-2032 (CAGR:2026-2032). The major factor driving the market growth is expected to be the increase in demand for sustainable and reusable space systems.

With the increasing number of satellites going into space, the demand for satellite servicing has been rising. In the future years, refueling capabilities are expected to become a need rather than an option for satellite operators. Several market players have already started demonstrations and some have been successful. Commercial players are expected to extract the maximum benefit of the space in-orbit refueling technologies.

Market Lifecycle Stage

Space in-orbit refueling has been on the wishlist of satellite operators for decades, however, even though the concepts existed, no company was able to materialize the technology. However, in the past 5 years, multiple established players and startups have entered the market and are now full-fledged working on the refueling capabilities. Massive amounts of investments are pouring into the industry and multiple collaborations are happening in order to co-develop new technologies.

Over 15 years of research and development on satellite refueling technologies have bought us to a stage where key players are performing successful demonstrations of in-orbit refueling and services in-orbit. Additionally, commercial players with large constellation sizes or heavy communication satellites are expected to adopt the market first. Following this, government agencies like NASA and ESA are also stepping forward to develop technologies and fund startups in the in-orbit refueling industry.

Figure: Global Space In-orbit Refueling Market, Value ($Million), 2026 and 2032

Source: Expert Interviews and BIS Research Analysis

Note: CAGR% (2026-2032)

Applications, such as site earth observation, communication, and navigation, are some of the areas where satellites are expected to be refueled in the coming years. Moreover, newer technologies, such as advanced docking systems, fueling ports, and artificial intelligence software are expected to support the growth of the space in-orbit refueling market over the 2022-2032 forecast period.

Market Segmentation:

Segmentation 1: by Application

• Earth Observation

• Communication

• Navigation

Based on application, the space in-orbit refueling market is expected to be dominated by the communication segment owing to its technological and economic feasibility. Communication and Earth observation applications are expected to see the first initial missions for refueling.

Segmentation 2: by End-User

• Commercial

• Other End Users

Based on end-user, the space in-orbit refueling market is expected to be dominated by commercial end-users. Commercial end-users are expected to garner significant share and growth due to their priority requirement and economic feasibility. Commercial satellite operators with large satellite constellations and heavy communication satellites are expected to adopt the technologies faster compared to any other segment.

Segmentation 3: by Region

• North America

• Europe

• Asia-Pacific

During the forecast period, North America is expected to dominate the space in-orbit refueling market (by region). The significant presence of key companies engaged in developing space in-orbit refueling services is a major factor responsible for the region's growth. A higher number of collaborations between various service providers, satellite operators, and enabling technology providers is another factor driving the market growth. An increasing number of start-ups and emerging players and successful demonstrations and increasing investments by key players in the market are also contributing to the market growth.

Recent Developments in the Space In-Orbit Refueling Market

• In January 2022, Astroscale Holdings Inc. and Orbit Fab, Inc signed a commercial agreement for refueling LEXI in the GEO orbit. LEXI is the first satellite that is designed to be refueled. As per the agreement, Orbit Fab, Inc will refuel Astroscale’s fleet of LEXI Servicers with up to 1000 kgs of Xenon Propellant.

• To develop technologies for cryogenic propellant storage and transfer, with these awards, NASA is investing in technologies for the storage and transfer of cryogenic propellants in space. Four awards worth more than $250 million went to companies working on cryogenic fluid management.

• To demonstrate refueling a GEO satellite, Northrop Grumman’s Mission Extension Vehicle-1 (MEV-1) docked with Intelsat 901 on 25th February 2020 and pushed the satellite back to its normal orbit. Northrop Grumman’s MEVs are expected to give more than 15 years of life extension to these satellites along with providing spacecraft inspections, inclination changes, and orbit repair.

• In April 2022, Washington’s Defense Innovation Unit (DIU) is planning to provide commercial refilling services in near the prime space real estate of Geosynchronous Orbit, commonly referred to as GEO. It’s also planning on creating a “bulk fuel depot” in the orbits. DIU is looking for companies with the capability for bulk liquid and gas propellant storage (>5,000 kg) in orbit. Two of the propellants include hydrazine and liquid oxygen.

• In April 2022, Orbit Fab, Inc and Neutron Star Systems have announced a partnership for the co-development of sustainable propulsion capability and satellite refueling technologies. The agreement will help to increase the range of refuellable propellants by combining NSS propellant-agnostic electric propulsion technology with Orbit Fab's refueling interfaces and tankers.

Demand - Drivers and Limitations

Following are the drivers for the Space In-Orbit Refueling market:

• Increase in Demand for Sustainable and Reusable Space Systems

• Life Extension Services to Enable Other In-Orbit Services in Future

Following are the challenges for the Space In-Orbit Refueling market:

• High Operational Cost of Refueling

• Interface and Docking

• Regulatory Challenges

• Spacecraft Design Compatibility for Refueling Operations

• Storage and Transfer of Cryogenic Propellants in Space

Following are the opportunities for the Space In-Orbit Refueling market:

• Increase in Investments for Startups

• Rise in Demand for In-Space Services

• Advancement of New Space Technologies for Storage, Refueling, and Receiving Propellants

Analyst’s Perspective

According to Arun Kumar Sampathkumar, Principal Analyst, BIS Research, “The in-orbit servicing segment of the space industry has just got started with a few life-extension missions successfully achieving their objectives. While, the de-orbiting service segment is expected to be the largest in terms of quantum of demand, the refuelling and life-extension segments will remain prominent in the short term. Since the deployment of refueling-compatible hardware is yet to be deployed across missions, moving forward, with such hardware being included as part of satellite platforms, the refuelling segment will migrate from non-cooperative life-extension format to co-operative refueling format post which the market will enter a steady growth phase. The in-orbit refueling market will also be driven by the startups who are focused on establishing unique use cases to support a range of operators covering earth-orbit to deep space missions.”

Focus on Application, End User, Capability, and Country - Analysis and Forecast, 2022-2032

The global space situational awareness services market was valued at $125.2 million in 2021,...

The global space-qualified propellant tank market is expected to reach $3,069.5 million by...