A quick peek into the report

Transportation Testing, Inspection, and Certification Services Market Overview

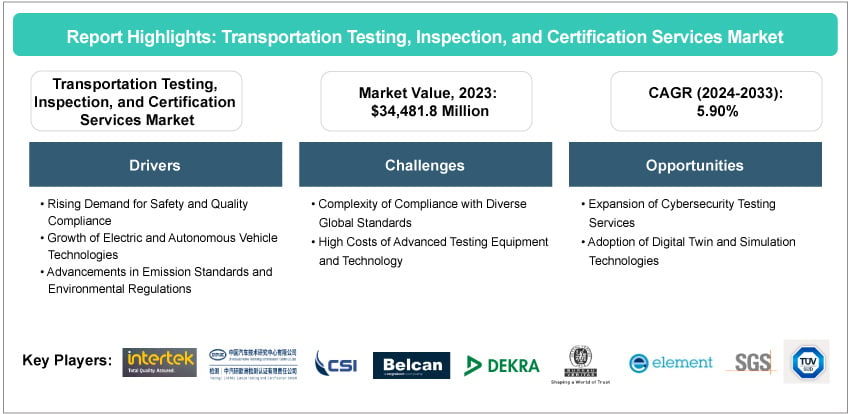

The transportation testing, inspection, and certification services market was valued at $34.48 billion in 2023 and is expected to grow at a CAGR of 5.90% and reach $61.74 billion by 2033. The transportation testing, inspection, and certification services market has been witnessing substantial growth, driven by the rising need for safety, regulatory compliance, and quality assurance across various transportation sectors. These services play a crucial role in ensuring that vehicles, infrastructure, and components meet stringent safety and performance standards, supporting smoother and more reliable operations. As transportation systems evolve to incorporate advanced technologies such as electric and autonomous vehicles, demand for specialized testing and certification services has been increasing. Advancements in testing methodologies and automated inspection tools have also enhanced accuracy and efficiency, further driving market adoption across automotive, rail, maritime, and aviation industries.

Introduction to Transportation Testing, Inspection, and Certification Services

Transportation testing, inspection, and certification services encompass a range of specialized processes designed to ensure the safety, performance, and regulatory compliance of vehicles, infrastructure, and components across the transportation sector. These services involve rigorous testing and evaluation of various parameters such as durability, emissions, fuel efficiency, and structural integrity to verify that transportation assets meet national and international standards. Utilizing advanced testing equipment and inspection technologies, such as non-destructive testing (NDT) methods, automated inspection systems, and real-time monitoring tools, these services provide critical assurance for manufacturers, regulatory bodies, and consumers alike. By identifying potential risks and ensuring operational safety, transportation testing, inspection, and certification services are fundamental to the reliability, efficiency, and sustainability of modern transportation systems across automotive, rail, maritime, and aviation industries.

Market Introduction

The transportation testing, inspection, and certification services market has rapidly expanded as industries adopt rigorous standards to ensure safety, compliance, and quality across various transportation modes. These services, including vehicle testing, infrastructure inspection, and component certification, have become essential as advancements in autonomous, electric, and connected vehicle technologies accelerate. With the increasing regulatory requirements and consumer expectations for safety, the demand for reliable testing and certification services has been growing globally. The market is set to experience significant growth, driven by innovations in testing methods, automation, and real-time monitoring tools, as well as the need to support sustainable transportation solutions and minimize operational risks across automotive, rail, maritime, and aviation sectors.

Industrial Impact

The industrial impact of the transportation testing, inspection, and certification services market extends across the transportation sector alongside advancements in vehicle technology and infrastructure. These services drive innovation in safety standards and compliance, promoting the development of more reliable, efficient, and sustainable transportation systems. As the market grows, it enhances collaboration between technology providers, regulatory bodies, and transportation companies, raising industry standards and fueling advancements in quality and safety. It promotes safer, more efficient transport systems and aligns with global safety and sustainability goals, influencing practices across automotive, rail, maritime, and aviation industries and supporting a more resilient and environmentally responsible transportation ecosystem.

The key players operating in the transportation testing, inspection, and certification services market include Intertek Group plc, CATARC Europe Testing and Certification GmbH, CSI S.p.A., Belcan, DEKRA SE, Bureau Veritas, Applus+, Element Materials Technology, HORIBA MIRA, UL LLC, Eurofins Scientific, Kiwa, SGS Société Générale de Surveillance SA., TÜV SÜD, UTAC, FEV Group GmbH, AVL, Reinova S.p.a. and Smithers MISTRAS Group. These companies have been focusing on strategic partnerships, collaborations, and acquisitions to enhance their product offerings and expand their market presence.

Market Segmentation

Segmentation 1: by Application

• Automotive

o Design Validation and Prototyping

o Performance Testing

o Lifecycle Assessment

o Environmental and Compliance Assessment

o Material Testing

o Others

• Rail Transportation

o Rolling Stock Maintenance Inspection and Testing

o Power Supply Testing and Certification Services

o Safety Inspection and Testing

o Others

• Marine Transportation

o Welding Inspection and Testing

o Non-Destructive Testing

o Fire Resistance Testing

o Others

• Air Transportation

o Structural Testing

o Material and Chemicals Testing

o Others

Automotive Application to Lead the Market (by Application)

In the transportation testing, inspection, and certification services market, the automotive sector is led by application and driven by the industry's stringent safety and quality standards. Automotive manufacturers increasingly rely on transportation testing, inspection, and certification services to ensure vehicles meet regulatory requirements across safety, emissions, and performance criteria. The shift toward electric and autonomous vehicles has intensified this demand, as these vehicles require specialized testing for battery safety, software integrity, and sensor reliability. Furthermore, the rising focus on sustainability and environmental compliance has amplified the need for emissions testing and certification as automotive companies strive to align with global carbon reduction targets.

Furthermore, the growth in the automotive sector has also been driven by emerging regulations mandating advanced safety features and eco-friendly technologies in vehicles, particularly in regions such as Europe and North America. As vehicle technologies evolve, including advancements in connectivity and automation, the role of transportation testing, inspection, and certification services becomes even more critical, supporting manufacturers in navigating complex compliance landscapes and enhancing product reliability. With the global automotive sector continuing its transformation toward smarter and greener mobility solutions, the demand for transportation testing, inspection, and certification services within this application segment is expected to remain strong, driving market expansion in the coming years.

Segmentation 2: by Service Type

• Lab Testing

• Inspection

• Homologation and Certification

Lab Testing to Lead the Market (by Service Type)

In the transportation testing, inspection, and certification services market, lab testing is led by service type and is driven by its essential role in ensuring the quality, safety, and compliance of transportation products. Lab testing is highly valued for its precision and ability to simulate extreme conditions, providing critical insights into material performance, durability, and safety standards. This service type is especially important in the automotive and aerospace sectors, where rigorous testing is required to meet regulatory and safety requirements before products reach the market.

Moreover, as manufacturers across the transportation industry have been increasingly prioritizing product reliability and regulatory compliance, the reliance on lab testing as a foundational service type in the market is expected to strengthen. The growing complexity of modern transportation technologies further strengthens its leadership, ensuring quality assurance in evolving transportation ecosystems.

Segmentation 3: by Stage

• Pre-Production

• Maintenance and Lifecycle

Pre-Production Stage to Lead the Market (by Stage)

In the transportation testing, inspection, and certification services market, the pre-production stage has emerged as the leading phase, driven by the growing emphasis on early-stage quality assurance, risk mitigation, and regulatory compliance. Pre-production testing is highly valued as it allows manufacturers to identify potential flaws, ensure regulatory alignment, and optimize product designs before mass production begins. This stage is particularly critical in the automotive, aerospace, and rail industries, where stringent safety standards and complex engineering requirements necessitate thorough, upfront evaluation.

Moreover, the importance of pre-production testing is amplified by the increasing complexity of modern transportation systems, which rely on advanced materials, electronics, and software. By addressing compliance and performance issues early, companies can reduce costly recalls and improve product reliability, enhancing their market competitiveness. As regulatory bodies and industry standards continue to push for higher safety and environmental standards, the demand for comprehensive pre-production transportation testing, inspection, and certification services is expected to grow, solidifying this stage's leadership within the market and driving continued expansion.

Segmentation 4: by Vehicle Type

• Passenger Vehicles

• Commercial Vehicles

Passenger Vehicles to Lead the Market (by Vehicle Type)

In the transportation testing, inspection, and certification services market, passenger vehicles are led by vehicle type and driven by the high demand for safety, quality, and regulatory compliance across global markets. Passenger vehicles require extensive testing due to the production volume and the diverse regulatory standards they must meet in different regions. This segment is especially prominent in the transportation testing, inspection, and certification services market as consumer expectations for vehicle safety and performance continue to rise, with manufacturers increasingly focusing on advanced features such as autonomous driving, enhanced connectivity, and electric propulsion systems.

Furthermore, the ongoing innovation in passenger vehicle technologies, combined with an emphasis on reducing environmental impact, strengthens the need for comprehensive services. This reliance strengthens passenger vehicles' leadership within the market, making transportation testing, inspection, and certification services a critical component in the lifecycle of vehicle development, from design through to production and market introduction.

Segmentation 5: by Propulsion Type

• Internal Combustion Engine Vehicles

• Electric Vehicles

Internal Combustion Engine Vehicles to Lead the Market (by Propulsion Type)

Internal combustion engine (ICE) vehicles, led by propulsion type, are driven by their widespread presence and established regulatory requirements. Despite the global shift toward electric mobility, ICE vehicles still dominate the automotive landscape, particularly in regions with developing infrastructure for alternative energy sources. The transportation testing, inspection, and certification services market for ICE vehicles has been driven by rigorous emissions testing, safety evaluations, and compliance with evolving environmental standards to reduce carbon footprints and pollutant levels.

Furthermore, as governments worldwide implement stricter emissions regulations, transportation testing, inspection, and certification services for ICE vehicles have been increasingly essential to ensure manufacturers meet compliance and avoid costly penalties. This continued focus on reducing emissions and improving fuel efficiency has solidified ICE vehicles' dominant role within the market, as they require ongoing testing and inspection to adapt to regulatory changes.

Segmentation 6: by Region

• North America: U.S. and Rest-of-North America

• Europe: Germany, France, Netherlands, Denmark, Sweden, U.K., Poland, Spain, Italy, and Rest-of-Europe

• Asia-Pacific: China, Japan, South Korea, Australia and Rest-of-Asia-Pacific

• Rest-of-the-World: U.A.E., Brazil and Others

Europe is set to lead the transportation testing, inspection, and certification services market, driven by strict regulatory frameworks, advanced infrastructure, and a strong emphasis on safety and sustainability in the transportation sector. Countries such as Germany, France, and the Netherlands have been driving growth in the market with increasing demand for transportation testing, inspection, and certification services across automotive, rail, and aerospace industries. Europe's automotive industry, particularly in electric and autonomous vehicles, has significantly increased the need for these services to ensure compliance with stringent safety and environmental standards. In aerospace, the growing focus on sustainable aviation and the implementation of next-generation technologies have been expanding the scope of testing and certification requirements. Overall, Europe’s strong regulatory approach and technology help the region to stay at the forefront of the market, driving innovation in transportation safety, sustainability, and compliance standards. This position is likely to strengthen as Europe’s industries continue to adapt to evolving transportation technologies and stringent environmental regulations, ensuring sustainable growth for the transportation testing, inspection, and certification services market.

Recent Developments in the Transportation Testing, Inspection, and Certification Services Market

• In August 2024, TÜV Rheinland opened its largest laboratory in China, following a significant investment of over $30.2 million. This facility focuses on testing services across critical sectors such as electronics, photovoltaics, e-mobility, and autonomous driving. Equipped with specialized laboratories, including automotive LiDAR, packaging, and intelligent driving sensing, the hub provides streamlined testing solutions for local industries.

• In August 2023, DEKRA, one of the global leaders in testing, inspection, and certification, partnered with AIShield, a Bosch startup specializing in AI application security, to enhance the security of AI models and systems. This collaboration focuses on developing advanced training, assessment, and protection measures to secure AI systems across industries such as automotive. The partnership addresses the requirements of standards such as the EU AI Act, NIST AI RMF, and MITRE ATLAS, aiming to strengthen AI cyber-resilience and ensure regulatory compliance.

• In July 2023, TÜV SÜD America Inc. inaugurated its advanced environmental laboratory in the U.S., strengthening its role in electric vehicle (EV) safety and performance testing. This state-of-the-art facility, a $47.5 million investment, is the company's largest laboratory site globally and is equipped for comprehensive EV battery testing, including high-voltage systems, electro-dynamic vibration, and abuse testing. The facility, which supports the country's growing EV ecosystem, is designed with sustainable features, such as the use of clean energy, LED lighting, and locally sourced materials, showcasing TÜV SÜD's commitment to sustainability.

• In July 2022, DEKRA announced a strategic collaboration with Microsoft to develop digital inspection solutions using the Microsoft Azure Cloud, primarily aimed at enhancing safety in the transport and workplace sectors. This partnership marks a significant advancement for the testing, inspection, and certification industry, allowing DEKRA to incorporate digital tools such as IoT, AI, analytics, and digital twins into its inspection services, thereby improving efficiency and data integrity in safety assessments.

Demand - Drivers, Limitations, and Opportunities

Market Drivers: Rising Demand for Safety and Quality Compliance

The transportation testing, inspection, and certification services market has been witnessing a surge in demand due to increased global emphasis on safety and quality compliance. As transportation technologies evolve with the rise of electric, autonomous, and connected vehicles, there has been a growing need to ensure that these systems meet stringent safety and quality standards. Regulatory bodies implement comprehensive frameworks to address the risks associated with new technologies, driving companies to seek transportation testing, inspection, and certification services to demonstrate compliance and avoid penalties.

Additionally, major companies in the transportation testing, inspection, and certification services market have been emphasizing the increasing importance and benefits of rigorous compliance and quality assurance to meet evolving safety and regulatory standards. For instance, in August 2024, TÜV Rheinland opened its largest laboratory in China, following a significant investment of over $30.2 million. This facility focuses on testing services across critical sectors such as electronics, photovoltaics, e-mobility, and autonomous driving. Equipped with specialized laboratories, including automotive LiDAR, packaging, and intelligent driving sensing, the hub provides streamlined testing solutions for local industries. Highlighting TÜV Rheinland’s commitment to supporting China’s technological advancement, this expansion aims to enhance safety, quality, and compliance for various industries.

Market Challenges: Complexity of Compliance with Diverse Global Standards

The complexity of compliance with diverse global standards presents a formidable challenge in the transportation testing, inspection, and certification services market. As countries implement distinct regulations and compliance requirements for transportation safety, emissions, and environmental sustainability, TIC providers face mounting pressure to keep pace with evolving standards. This challenge is heightened by variations in regional safety and environmental norms, particularly as the industry moves toward greater automation and electric transportation solutions. The need to understand, interpret, and apply numerous regulations to various vehicles and equipment strains resources and calls for constant adaptation, making it difficult for TIC providers to maintain efficient and standardized processes across global markets.

In response to the challenge, companies in the sector have been developing solutions to enhance their ability to comply with multiple regulatory frameworks. For instance, TÜV SÜD expanded its digital compliance capabilities by introducing the universal customer interface (UCI), a centralized platform that empowers clients to manage workflows, track project progress, and submit regulatory application forms online. This platform simplifies the management of complex regulatory data and automates the tracking of changes in legislation, assisting clients in achieving compliance across diverse markets.

Market Opportunities: Expansion of Cybersecurity Testing Services

Cybersecurity testing services present a pivotal opportunity in the transportation testing, inspection, and certification (TIC) services market as connected and automated systems become integral to transportation. Autonomous vehicles, smart rail systems, and digital aviation technologies rely heavily on secure communication and control systems to prevent unauthorized access and ensure data integrity. To meet these security needs and align with regulatory standards, TIC providers have increasingly developed specialized cybersecurity solutions that address risks specific to connected transportation technologies. This expansion positions cybersecurity as a crucial element in the evolution of safe and reliable transportation.

In a strategic move to enhance its cybersecurity capabilities, Bureau Veritas acquired Security Innovation Inc., a U.S.-based firm specializing in software security, in July 2024. This acquisition aligns with Bureau Veritas’s LEAP 28 strategy to grow in the cybersecurity sector and strengthen its presence in North America. Security Innovation Inc. provides software security consulting, secure software development lifecycle (SDLC) advisory, and training. This adds significant expertise in cybersecurity testing and AI capabilities to Bureau Veritas’s global offerings. Additionally, this acquisition is expected to benefit both Bureau Veritas's customers and Security Innovation’s clients, expanding services in software security across private and public sectors and reinforcing Bureau Veritas’s role in cybersecurity innovation within the testing, inspection, and certification services market. The transaction is anticipated to establish a new cybersecurity hub in the U.S. with potential global scalability.

Analyst View

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The global transportation testing, inspection, and certification services market is anticipated to experience significant growth in the coming years, driven by the rise of electric and autonomous vehicles and the need for enhanced safety and regulatory compliance. Growing investments in advanced testing technologies and stricter government regulations across automotive, rail, maritime, and aviation sectors are expected to propel market expansion further. Key industry players are likely to prioritize strategic partnerships, innovation in testing methodologies, and the integration of automated and data-driven inspection systems to strengthen their market presence. Additionally, advancements in non-destructive testing, real-time monitoring, and digital inspection tools will be critical in enhancing the precision and efficiency of testing services, supporting more reliable and sustainable transportation solutions globally.”

Transportation Testing, Inspection, and Certification Services Market

Focus on Applications, Products, and EPA 1065 Regulations in the U.S. - Analysis and Forecast, 2024-2033

Frequently Asked Questions

Ans: Transportation testing, inspection, and certification services encompass a range of specialized processes designed to ensure the safety, performance, and regulatory compliance of vehicles, infrastructure, and components across the transportation sector. These services involve rigorous testing and evaluation of various parameters such as durability, emissions, fuel efficiency, and structural integrity to verify that transportation assets meet national and international standards.

Ans: The key business opportunities in the transportation testing, inspection, and certification services market are stringent regulations by government bodies related to environmental sustainability and gaining a competitive edge through innovation.

Ans: The transportation testing, inspection, and certification services market is expected to grow over time, and companies will come up with collaborative strategies to sustain themselves in the intensely competitive market. Companies with an identical product portfolio and a need for additional resources often partner and come together for joint venture programs, which help the companies gain access to one another’s resources and facilitate them to achieve their objectives faster.

Ans: A new entrant can focus on partnering with existing transportation testing, inspection, and certification service providers. Also, start-ups can focus on funding, launching new innovative products, and expanding their sales and distribution networks.

Ans: The following are some of the USPs of this report:

• A dedicated section focusing on the trends adopted by the key players operating in the transportation testing, inspection, and certification services market

• Competitive landscape of the companies operating in the ecosystem offering a holistic view of the transportation testing, inspection, and certification services market landscape

• Qualitative and quantitative analysis of the transportation testing, inspection, and certification services market at the region and country level and granularity by application and product segments

• Supply chain and value chain analysis

Ans: Automotive manufacturers, testing and inspection companies, logistics companies, and fleet operators can buy this report.