A quick peek into the report

Vehicle Computer Tomography Market Industry and Technology Overview

The vehicle computer tomography market represents a vital segment within the broader industrial CT and non-destructive testing ecosystem. CT technology continues to evolve with advancements in multi-slice imaging, detector sensitivity, and AI-based image processing algorithms. Vehicle computer tomography systems are essential for internal inspection of automotive components such as engines, transmissions, battery packs, and castings without disassembly. Recent innovations including cone-beam CT and nano-CT have significantly enhanced image resolution and scan speed, expanding their applicability in vehicle manufacturing and R&D. Artificial intelligence and machine learning integration enable automated defect recognition, increasing throughput and reducing human error. Investment in R&D focuses on developing high-speed, cost-efficient CT systems tailored for automotive quality control and electric vehicle battery diagnostics. The vehicle computer tomography market benefits from increasing adoption of non-destructive testing to improve manufacturing yield and safety compliance.

Global Vehicle Computer Tomography Market Lifecycle Stage

Currently, the vehicle computer tomography market is experiencing robust growth, supported by rising automotive production volumes and stringent safety and quality regulations worldwide. The market has reached advanced technology readiness levels, with growing adoption in North America, Europe, and Asia-Pacific regions. The U.S. automotive sector notably drives demand due to its focus on innovation and quality assurance. Strategic partnerships among CT scanner manufacturers, automotive OEMs, and research institutions foster accelerated development of customized scanning solutions. Regulatory frameworks related to vehicle safety and environmental standards shape market dynamics. Continued advancements in automation, digital analytics, and AI are reducing operational barriers and enabling in-line integration of CT systems in vehicle manufacturing processes. The vehicle computer tomography market is projected to sustain strong growth through the next decade, driven by increasing electric vehicle production and demand for lightweight, defect-free components.

Vehicle Computer Tomography Market Segmentation:

Segmentation 1: by Scanner Type

• Industrial CT Scanners

• Mobile CT Scanners

• Automated CT Scanners

• CT with AI Analysis

Segmentation 2: by Application

• Quality Control

• Prototype Development

• Material Analysis

• Non-Destructive Testing

• Structural Integrity

Segmentation 3: by End User

• Original Equipment Manufacturers

• Automotive Aftermarket and Maintenance Service Providers

• Research and Development Institutions

• Tier 1 and Tier 2 Automotive Suppliers

Segmentation 4: by Region

• North America - U.S., Canada, and Mexico

• Europe - Germany, France, Italy, Spain, U.K., and Rest-of-Europe

• Asia-Pacific - China, Japan, South Korea, India, and Rest-of-Asia-Pacific

• Rest-of-the-World - South America and Middle East and Africa

Demand – Drivers and Limitations

The following are the demand drivers for the vehicle computer tomography market:

• Increasing automotive industry focus on non-destructive testing and quality assurance

• Growing demand for electric vehicles (EVs)

• Regulatory mandates for vehicle safety and component traceability

• Technological advancements in AI integration and faster scanning capabilities

The vehicle computer tomography market is expected to face some limitations as well due to the following challenges:

• High initial investment and operational costs associated with CT systems

• Requirement for specialized technical expertise in data interpretation

• Integration complexities with existing automotive manufacturing lines

Analyst Thoughts

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The vehicle computer tomography market is positioned for significant growth as automotive manufacturers worldwide prioritize enhanced product quality, safety, and innovation. Advances in CT technology, combined with AI-driven analytics, are revolutionizing defect detection and manufacturing process optimization. Companies focusing on scalable, automated CT solutions with reduced costs and increased throughput will lead the market. Strategic partnerships with OEMs and investment in application-specific innovations, particularly in electric vehicle battery analysis, will be critical for sustained competitiveness in the vehicle computer tomography market.”

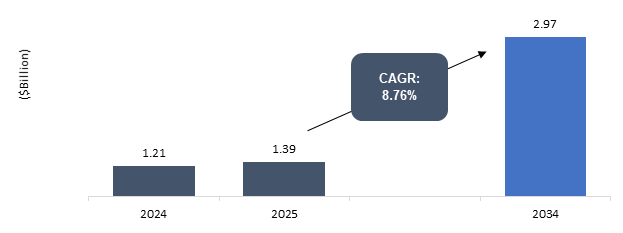

Vehicle Computer Tomography Market - A Global and Regional Analysis

Focus on Scanner Type, Application, End User, and Regional Analysis - Analysis and Forecast, 2025-2034

Frequently Asked Questions

Ans: Vehicle computer tomography is an advanced non-destructive imaging technique that uses X-ray computed tomography to produce detailed three-dimensional internal images of vehicle components. This technology facilitates precise defect detection, structural analysis, and quality assurance in automotive manufacturing and maintenance.

Ans: The vehicle computer tomography market is advancing rapidly, driven by several key trends. The integration of artificial intelligence (AI) and machine learning enables automated defect recognition and enhanced image analysis, improving efficiency and accuracy. Increasing demand for electric vehicle battery inspection has expanded CT applications, necessitating high-resolution, high-speed scanning systems. Portable and automated CT scanners are gaining traction for use in aftermarket diagnostics and in-line manufacturing inspection. Additionally, advances in multi-slice and cone-beam CT technologies contribute to improved imaging capabilities and reduced scan times.

Ans: Leading companies are investing heavily in research and development to innovate CT scanning technologies with higher resolution, faster throughput, and AI-driven analytics. Strategic partnerships with automotive OEMs and suppliers enhance product customization and integration capabilities. Firms are broadening their geographic footprint to capture emerging markets and developing comprehensive software solutions to simplify data interpretation and improve operational workflows. Emphasis on modular and scalable CT systems facilitates adoption across various automotive applications, from component manufacturing to electric vehicle battery analysis.

Ans: New entrants should prioritize innovation in AI-enabled imaging and automated defect detection, develop portable and cost-efficient CT scanning solutions, and focus on electric vehicle battery inspection technologies. Building strong collaborations with automotive manufacturers and research institutions will support tailored product development and faster market acceptance. Offering robust training and after-sales support will also enhance customer satisfaction and retention.

Ans: This report provides detailed competitive benchmarking of leading global players, comprehensive segmentation by scanner type, application, end user, and region, along with in-depth analysis of emerging trends, technological advancements, and market dynamics. It delivers a thorough understanding of the vehicle computer tomography market landscape, enabling stakeholders to make informed strategic decisions.

Ans: This report is essential for automotive manufacturers, CT scanner producers, quality assurance and testing service providers, research organizations, and investors focused on the automotive inspection, non-destructive testing, and imaging technology sectors.