A quick peek into the report

Global White Biotechnology Market: Industry Overview

White biotechnology—also known as industrial biotechnology—leverages living cells, enzymes and fermentation processes to produce bio-based chemicals, materials and energy carriers. Core application areas include biofuels (e.g., advanced biodiesel and bioethanol), biochemicals (organic acids, solvents), industrial enzymes (for detergents, textiles, food processing), biomaterials (biopolymers, bioplastics) and emerging fields such as bioremediation and renewable feedstock valorization. Technological advances in synthetic biology, metabolic engineering and protein engineering are enabling more efficient strain development, higher yields and reduced process costs. Concurrently, digital tools—machine learning for bioprocess optimization, high-throughput screening and scalable continuous-flow fermentation—are accelerating time-to-market for new bioproducts. This convergence of biology and digitalization is driving white biotechnology market’s transformation from niche specialty applications toward large-scale industrial adoption.

White Biotechnology Market Lifecycle Stage

The white biotechnology market is firmly in its growth phase, characterized by robust R&D investment, rapid technology commercialization and an expanding base of both established chemical-industry incumbents and agile biotech startups. Market concentration remains moderate, with innovation dispersed across diverse segments—from enzyme producers like Novozymes and DuPont to bio-based materials pioneers—indicating ample room for new entrants. As process efficiencies improve and regulatory frameworks for bio-based products mature, the industry is poised to transition toward consolidation and maturation over the next decade, with large strategic partnerships and mergers likely to shape the competitive landscape.

White Biotechnology Market Segmentation:

Segmentation 1: by Application

• Bioenergy

• Food and Feed Additives

• Pharmaceutical Ingredients

• Personal Care and Household Products

• Others

Bioenergy is one of the prominent application segments in the global white biotechnology market.

Segmentation 2: by Product Type

• Biochemical

• Biofuel

• Biomaterial

• Bioproduct

The global white biotechnology market is estimated to be led by the biochemical segment in terms of product type.

Segmentation 3: by Region

• North America - U.S., Canada, and Mexico

• Europe - Germany, France, Italy, Spain, U.K., and Rest-of-Europe

• Asia-Pacific - China, Japan, South Korea, India, and Rest-of-Asia-Pacific

• Rest-of-the-World - South America and Middle East and Africa

In the white biotechnology market, North America is anticipated to gain traction in terms of production, with increasing demand towards renewable resources and govement initiatives.

Demand – Drivers and Limitations

The following are the demand drivers for the global white biotechnology market:

• Increasing Demand Towards Renewable Resources

The global white biotechnology market is expected to face some limitations as well due to the following challenges:

• High Initial Investment Costs

Analyst Thoughts

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The global white biotechnology market is currently at an inflection point, driven by rapid advances in synthetic biology, enzyme engineering and AI-enabled bioprocess optimization that are enabling cost-effective production of bio-based chemicals, materials and fuels. Today’s market is characterized by strategic partnerships between incumbent chemical manufacturers and biotech innovators, the emergence of decentralized “biofoundries” for on-demand molecule synthesis and growing policy support for circular bioeconomy initiatives. Looking ahead, continued integration of digital twins, machine-learning-driven strain design and continuous-flow fermentation is expected to accelerate scale-up timelines, reduce capital intensity and broaden the range of commercially viable products—from advanced bioplastics and specialty enzymes to next-generation biofuels. As industry incumbents increasingly retrofit existing assets for bioprocessing and new entrants leverage modular biomanufacturing platforms, white biotechnology will reshape global supply chains, displace conventional petrochemical pathways and establish the foundational technologies of a sustainable, bio-based economy.”

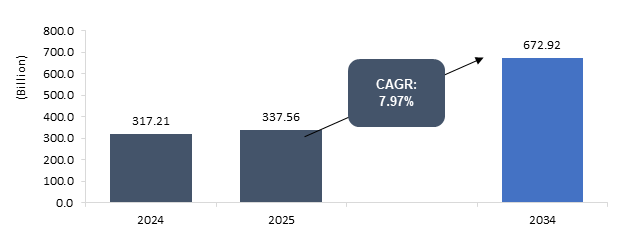

White Biotechnology Market - A Global and Regional Analysis

Focus on Application, Product, and Country Analysis - Analysis and Forecast, 2025-2034

Frequently Asked Questions

BIS Research has considered the definition of white biotechnology for railway as “as industrial biotechnology, harnesses living cells, enzymes and microorganisms to produce chemicals, materials and energy through environmentally sustainable processes. By replacing traditional petrochemical-based routes with bio-based fermentation and catalysis, white biotechnology enables the manufacture of bioplastics, specialty enzymes, biofuels and high?value biochemicals with reduced carbon footprints and resource consumption. The sector spans applications in the chemicals, pharmaceutical, food and agriculture industries, and is underpinned by advances in metabolic engineering, high-throughput screening and bioprocess intensification that drive both economic viability and circular-economy objectives.

The global white biotechnology market is experiencing significant growth, driven by several key trends:

• Synthetic Biology and Metabolic Engineering

• Circular Bioeconomy and Feedstock Diversification

Leading white biotechnology companies are pursuing a combination of strategic partnerships, facility modularization and digital acceleration to consolidate market leadership. Major chemical and enzyme producers are entering joint ventures with synthetic-biology innovators to secure proprietary strains and enzyme libraries, while simultaneously retrofitting legacy petrochemical plants into flexible biofoundries. On the digital front, incumbents are integrating machine-learning-driven strain?design platforms and digital-twin bioprocess simulation into their R&D pipelines, enabling rapid scale-up and predictive yield optimization. Concurrently, government?backed incentive schemes in key regions—most notably China’s bioeconomy subsidies and India’s biotechnology innovation corridors—are being leveraged through public–private collaborations to co-fund next-generation biomanufacturing facilities, further entrenching established players’ competitive moats.

New entrants should concentrate on niche, high-value segments that demand specialized biocatalysts and tailored bioprocesses—such as advanced biopolymers for medical devices, designer enzymes for carbon-capture applications and low-pH microbial platforms for waste?to?value conversions. By adopting a modular, “factory-in-a-container” manufacturing model, newcomers can minimize capital risk and rapidly deploy pilot-scale facilities close to feedstock sources. Leveraging AI-native strain-engineering tools to accelerate host optimization, along with cloud-based process analytics to ensure real-time quality control, will enable agile product development and lean scale-up. Finally, forging early alliances with strategic end-users in sectors under regulatory pressure to decarbonize—such as specialty chemicals, agrochemicals and sustainable packaging—can secure offtake agreements that de-risk commercialization and catalyze rapid market entry.

The following can be termed as some of the USPs of the report:

• Extensive competitive benchmarking of 15 key players to offer a holistic view of the global white biotechnology market landscape

• Market segregation based on application and product.

• Investment landscape, including product adoption scenario, funding, and patent analysis

The companies that produce and commercialize white biotechnology for biotechnology, application sectors, research institutions, and regulatory bodies involved in the global white biotechnology market should buy this report.