Published Year: 2026

AI-Enabled Medical Imaging Solutions Market - A Global and Regional Analysis: Focus on Modality, Pro

The global AI-enabled medical imaging solutions market is projected to reach $18,041.3 million...

Focus on Modality, Application, and Regional Analysis - Analysis and Forecast Year, 2026-2036

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Introduction of the AI-Enabled Imaging Modalities Market

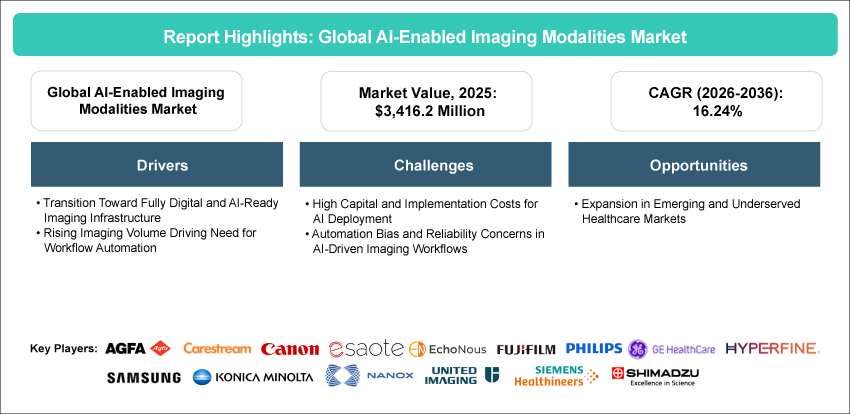

The global AI-enabled imaging modalities market, initially valued at $3,416.2 million in 2025, is projected to grow substantially, reaching $17,847.6 million by 2036, with a remarkable compound annual growth rate (CAGR) of 16.24% from 2026 to 2036.

The global AI-enabled imaging modalities market has been experiencing significant growth, driven by the increasing demand for accurate, faster, and workflow-efficient diagnostic imaging across healthcare systems. The rising volume of imaging procedures is creating strong demand for advanced imaging modalities that can improve diagnostic confidence, reduce turnaround times, and support higher patient throughput. AI-enabled imaging modalities, including X-ray, Magnetic Resonance Imaging (MRI) Systems, Computed Tomography, ultrasound, and other imaging modalities, are being increasingly used to support image acquisition, reconstruction, enhancement, detection, quantification, triage, reporting, and clinical decision-making. These systems help radiologists and clinicians manage growing diagnostic workloads by improving image quality, automating repetitive workflow steps, and enabling more consistent interpretation across clinical applications. Key innovations in AI-enabled reconstruction, image enhancement, automated detection, and workflow-integrated imaging platforms are accelerating the development of more efficient and scalable diagnostic imaging solutions.

Technological advancements are reshaping the AI-enabled imaging modalities landscape, with innovations such as deep learning-based reconstruction, AI-assisted image analysis, automated segmentation, and integrated workflow intelligence playing a pivotal role in improving the accuracy and efficiency of imaging procedures. Despite the market’s growth prospects, challenges such as high implementation costs, integration complexity, regulatory requirements, and concerns around clinical validation and reliability remain significant. However, ongoing investments in AI-ready imaging infrastructure, along with increasing collaborations between imaging original equipment manufacturers, healthcare providers, technology companies, and research institutions, are expected to drive further progress in the market.

Market Introduction

The global AI-enabled imaging modalities market has transformed, spurred by the convergence of imaging hardware, artificial intelligence, and connected healthcare IT infrastructure. Companies are increasingly integrating AI capabilities directly into imaging systems and enterprise platforms to enhance scanner performance, support clinical workflow intelligence, and enable more standardized diagnostic processes. Noteworthy advancements, such as embedded AI algorithms, automated protocol selection, intelligent image optimization, and interoperability with PACS, RIS, and EMR environments, underscore the industry’s focus on moving beyond standalone software tools toward integrated imaging ecosystems. As healthcare providers prioritize productivity, scalability, and consistency in diagnostic services, innovations in AI-enabled imaging modalities are expected to shape the market’s trajectory, positioning these technologies as central to next-generation imaging infrastructure and data-driven radiology operations.

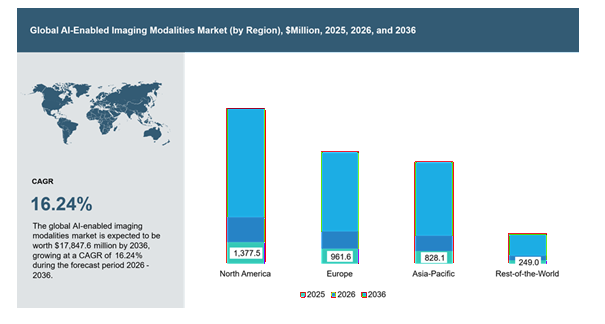

Global AI-Enabled Imaging Modalities Market (by Region), $Million, 2025, 2026, and 2036

Industrial Impact

The global AI-enabled imaging modalities market has witnessed significant growth, driven by the increasing demand for efficient diagnostic imaging systems and the rising emphasis on workflow optimization across radiology departments. Key players such as GE, Siemens Healthineers AG, Koninklijke Philips N.V., Canon Inc., FUJIFILM Holdings Corporation, and Samsung Healthcare play a central role in advancing AI-integrated imaging technologies, facilitating the development of more efficient, automated, and interoperable imaging solutions. These innovations are crucial across modalities such as CT, MRI, ultrasound, X-ray, and other systems, enabling healthcare providers to improve imaging throughput, enhance image quality, and support more consistent clinical interpretation. By reducing manual workload, streamlining scan and reporting processes, improving resource utilization, and enabling greater access to intelligent imaging capabilities, AI-enabled imaging modalities are contributing to a more efficient and scalable diagnostic imaging ecosystem. The market’s impact has been further amplified by its alignment with the growing global demand for digital health transformation, positioning AI-integrated imaging systems as a cornerstone of next-generation radiology infrastructure.

Market Segmentation

Segmentation 1: By Modality

• X-Ray

• Ultrasound

• Magnetic Resonance Imaging

• Computed Tomography

• Other Modalities

Computed Tomography Segment to Dominate the AI-Enabled Imaging Modalities Market (by Modality)

In terms of modality, the computed tomography segment is poised to lead the market during the forecast period, 2026-2036, accounting for a significant share due to the growing adoption of AI-enabled CT systems across high-volume diagnostic and emergency care settings. CT imaging is widely used across oncology, cardiovascular, neurology, trauma, and pulmonary applications, where faster image acquisition, improved image quality, and timely clinical interpretation are critical. AI-enabled CT systems support advanced capabilities such as image reconstruction, dose optimization, automated detection, organ and lesion quantification, workflow prioritization, and reporting assistance, which help improve diagnostic efficiency and patient throughput. As healthcare providers increasingly seek solutions that can address rising imaging volumes and radiology workflow pressures, AI integration within CT systems is becoming increasingly essential in clinical settings.

Segmentation 2: By Application

• General Imaging

• Specialty Imaging

Specialty Imaging to Dominate the AI-Enabled Imaging Modalities Market (by Application)

Regarding application, specialty imaging is expected to remain the most widely adopted application area for AI-enabled imaging modalities due to its strong linkage with high-value imaging systems and complex diagnostic workflows. Specialty imaging includes advanced applications across oncology, neurology, cardiology, musculoskeletal imaging, and molecular imaging, where accurate image reconstruction, lesion detection, quantification, workflow optimization, and clinical decision support are critical. AI-enabled imaging modalities are increasingly embedded into CT, MRI, and molecular imaging systems to support improved image quality, faster interpretation, structured assessment, and more consistent clinical decision-making.

Segmentation 3: By Region

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Rest-of-Europe

• Asia-Pacific

o China

o Japan

o Australia and New Zealand

o South Korea

o Singapore

o Rest-of-Asia-Pacific

• Rest-of-the-World

North America to Dominate the AI-Enabled Imaging Modalities Market (by Region)

In terms of region, North America is expected to lead the AI-enabled imaging modalities market, accounting for a significant share due to the region’s advanced diagnostic imaging infrastructure, strong adoption of AI-integrated imaging platforms, and high purchasing capacity among hospitals and imaging networks. The region has a large installed base of CT, MRI, X-ray, ultrasound, and other systems, creating a strong foundation for AI-enabled upgrades and workflow-integrated deployment. In addition, early regulatory clearances, strong presence of leading imaging original equipment manufacturers, and increasing investments in radiology automation are supporting broader adoption across clinical settings.

Recent Developments in the AI-Enabled Imaging Modalities Market

• In April 2026, Hyperfine, Inc. received CE Mark and UKCA approvals for its next-generation Swoop portable MRI system and updated Optive AI software. The advancements include improved image quality, enhanced workflow, and a new diffusion-weighted imaging (DWI) capability for better stroke detection. These approvals enable commercialization across Europe and the U.K., expanding access to AI-powered portable brain imaging at the point of care.

• In January 2026, Fujifilm India introduced a new portfolio of CT, mammography, X-ray, and healthcare IT solutions integrated with AI-enabled medical imaging and workflow automation, enabling end-to-end diagnostic workflows, faster clinical decision-making, and improved radiology efficiency across India.

• In December 2025, Samsung Healthcare, through its subsidiary Samsung Medison, introduced the R20 Ultrasound System at RSNA 2025. The system integrates AI-powered tools for real-time exam guidance, automated measurements, diagnostic assistance, and workflow automation, alongside advanced imaging hardware and beamforming technologies. It also incorporates ergonomic innovations to improve clinician comfort and efficiency, addressing increasing complexity in ultrasound imaging due to rising chronic disease burden.

Demand – Drivers, Challenges, and Opportunities

Market Drivers

Transition toward Fully Digital and AI-Ready Imaging Infrastructure: The shift from legacy imaging systems to fully digital and AI-ready infrastructure remains a key factor driving the demand for AI-enabled imaging modalities. Many healthcare facilities are modernizing outdated or partially digitized imaging environments to support better connectivity, data standardization, interoperability, and integration with advanced AI workflows. As imaging departments increasingly rely on PACS, cloud-based data management, enterprise imaging platforms, and connected scanners, the demand for AI-compatible systems has become more urgent. These systems are essential for enabling automated acquisition, image reconstruction, workflow support, dose optimization, and real-time analytics within routine clinical practice. This transition toward digital and AI-ready imaging infrastructure is helping create a more scalable and integrated diagnostic ecosystem, with a focus on operational efficiency, workflow intelligence, and future-ready imaging capabilities. The continued replacement of legacy systems presents significant market opportunities for imaging OEMs, AI software developers, and healthcare providers seeking to improve diagnostic performance and long-term return on investment.

Market Challenges

High Capital and Implementation Costs for AI Deployment: While AI-enabled imaging modalities offer considerable promise in improving diagnostic efficiency and radiology workflow performance, their deployment across clinical settings faces several cost-related challenges. The implementation of AI-enabled imaging systems often requires investment beyond the purchase of advanced imaging equipment, as healthcare providers also need supporting IT infrastructure, PACS/RIS integration, secure data management, workflow redesign, and staff training. These requirements create a significant barrier to adoption, particularly for smaller hospitals, imaging centers, and resource-constrained healthcare facilities. Many providers also face operational hurdles related to system validation, interoperability, user onboarding, and continuous performance monitoring, which increase the total cost of ownership over time. Additionally, the financial impact of AI deployment can vary depending on imaging volume, pricing models, infrastructure readiness, and the extent of integration required within existing clinical workflows. The need for ongoing software updates, maintenance, post-market surveillance, and lifecycle management further adds to implementation complexity and cost. These factors have slowed broader adoption of AI-enabled imaging modalities in routine clinical practice, especially in settings where return on investment remains uncertain.

Market Opportunities

Expansion of AI-Enabled Imaging in Emerging and Underserved Markets: The expansion of AI-enabled imaging modalities in emerging and underserved healthcare markets represents a significant growth opportunity in the global market. Many low- and middle-income regions continue to face limited access to diagnostic imaging services due to gaps in imaging infrastructure, radiologist availability, and specialized healthcare delivery capacity. AI-enabled imaging modalities can help address these limitations by supporting standardized image acquisition, automated image enhancement, workflow prioritization, and remote interpretation, particularly in settings where specialist expertise is scarce. The integration of AI into imaging workflows can improve diagnostic reach, support earlier disease detection, and enable more scalable delivery of imaging services beyond large tertiary hospitals. Moreover, advancements in portable imaging systems, cloud connectivity, and AI-compatible platforms are making it more feasible to deploy imaging solutions in decentralized and resource-constrained environments.

Analyst’s Thoughts

According to Swati Sood, Principal Analyst - BIS Research, “The AI-enabled imaging modalities market is poised for significant growth, driven by the rising demand for efficient diagnostic imaging systems, increasing imaging procedure volumes, and the transition toward fully digital and AI-ready healthcare infrastructure. As healthcare systems face growing pressure to improve radiology productivity, diagnostic accuracy, and turnaround times, AI-enabled imaging modalities are becoming increasingly important in supporting workflow automation, image quality enhancement, clinical decision-making, and standardized imaging delivery. The integration of artificial intelligence into CT, MRI, ultrasound, X-ray, and other modalities is expected to reshape diagnostic imaging by enabling faster acquisition, improved reconstruction, automated detection, and more efficient reporting workflows. With ongoing investments in imaging innovation, enterprise integration, regulatory validation, and digital health infrastructure, the AI-enabled imaging modalities market presents significant opportunities for technology advancement and global market expansion, particularly across emerging and underserved healthcare markets.”

Focus on Modality, Application, and Regional Analysis - Analysis and Forecast Year, 2026-2036

Ans: AI-enabled imaging modalities refer to diagnostic imaging systems either integrated with artificial intelligence capabilities or compatible with artificial intelligence across modalities such as computed tomography (CT), magnetic resonance imaging (MRI), ultrasound, X-ray, and other modalities. These systems use AI to support image acquisition, reconstruction, enhancement, detection, quantification, workflow prioritization, reporting assistance, and clinical decision-making, helping healthcare providers improve imaging efficiency, diagnostic consistency, and patient throughput.

Ans: To strengthen their market position, companies are focusing on embedding AI capabilities directly into imaging systems and enterprise imaging platforms. Many players are investing in AI-enabled reconstruction, automated detection, workflow automation, dose optimization, and cloud-connected imaging solutions to improve clinical and operational performance. Strategic collaborations between imaging OEMs, AI software developers, healthcare providers, and research institutions are also becoming important for clinical validation, regulatory approvals, product development, and broader market adoption.

The following are the USPs of this report:

• Market regulations and key trends in the AI-enabled imaging modalities market

• Market dynamic analysis of the opportunities, trends, and challenges in the market

Ans: This report is valuable for imaging original equipment manufacturers, AI solution providers, healthcare IT companies, hospitals, diagnostic imaging centers, research institutions, and investors involved in the development, deployment, or adoption of AI-enabled imaging systems. It will also benefit policymakers, procurement teams, and strategic decision-makers interested in understanding market trends, regulatory developments, competitive positioning, and opportunities for digital imaging infrastructure expansion.

The global AI-enabled medical imaging solutions market is projected to reach $18,041.3 million...

The global AI-enabled X-ray imaging systems market is projected to reach $4,761.3 million by...