A quick peek into the report

Automotive 48V Systems Market Overview

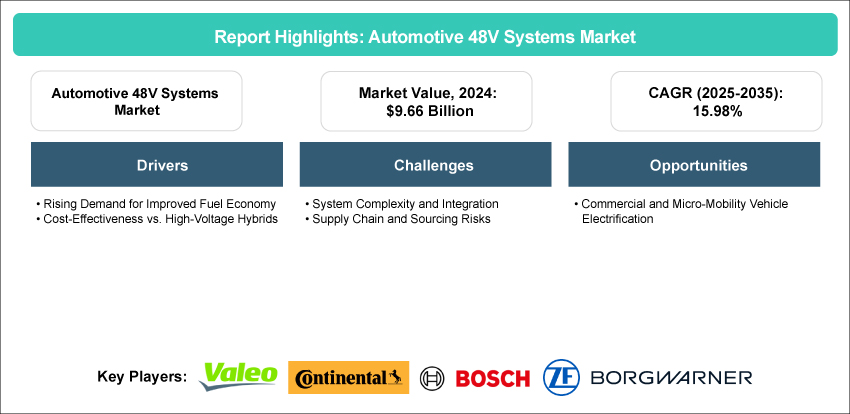

The automotive 48V systems market was valued at $9.66 billion in 2024 and is projected to grow at a CAGR of 15.98%, reaching $49.64 billion by 2035. The rising demand for hybrid and electric vehicles (EVs), which require efficient powertrains and energy management systems, is a critical driver for 48V technology. Automakers are increasingly turning to 48V systems to enhance fuel efficiency, reduce emissions, and improve vehicle performance. As manufacturers focus on achieving stricter emission regulations, the hybridization of vehicles using 48V systems for features like mild hybrid powertrains, energy recuperation, and electric assist is likely to become more widespread. Advances in battery technology and energy storage systems will further facilitate the adoption of 48V architectures, making them more efficient and cost-effective over time.

Introduction of Automotive 48V Systems

The study conducted by BIS Research highlights automotive 48V systems as a significant leap in vehicle electrical architectures, providing a higher power capacity compared to conventional 12V systems. These systems support various electrified vehicle components, including mild-hybrid powertrains, electric power steering, and regenerative braking, all of which contribute to improved fuel efficiency and reduced emissions. The 48V architecture allows for more efficient power distribution, enabling the integration of advanced features such as active suspension systems and enhanced lighting solutions. By improving energy transfer and reducing weight, automotive 48V systems offer an effective and cost-efficient solution for automakers seeking to incorporate electrification into their vehicle designs without the complexity and expense of transitioning to high-voltage electric systems. This makes them a key technology in modern vehicles, enhancing performance while supporting environmental sustainability. As the automotive industry continues to focus on reducing its carbon footprint, the adoption of 48V systems is expected to play a crucial role in meeting regulatory standards, increasing energy recovery, and optimizing overall vehicle performance. With their ability to deliver significant efficiency improvements, these systems are positioned to drive the next wave of automotive innovation.

Market Introduction

The global market for automotive 48V systems is experiencing significant growth as the automotive industry increasingly focuses on electrification and sustainability. These systems, which offer a higher power capacity than traditional 12V architectures, are essential in supporting the integration of electrified components such as mild-hybrid powertrains, electric power steering, and regenerative braking. As vehicle manufacturers aim to improve fuel efficiency, reduce emissions, and enhance overall performance, the demand for 48V systems is expected to rise sharply. Additionally, 48V systems facilitate the integration of advanced vehicle features such as active suspension systems and sophisticated lighting, further driving their adoption. The market is particularly poised for expansion as automakers seek cost-effective solutions to meet stricter emissions regulations without fully transitioning to high-voltage electric systems. This growth is being fueled by technological advancements, increased consumer demand for fuel-efficient vehicles, and the push toward electrification in both mainstream and luxury segments. Furthermore, regions like Asia-Pacific, North America, and Europe are leading the way in the adoption of 48V technology, with Asia-Pacific showing the largest market share due to its dominance in electric vehicle production and strong regulatory frameworks promoting eco-friendly automotive solutions. As the industry moves toward electrified powertrains, automotive 48V systems are set to play a pivotal role in shaping the future of vehicle design, offering a balance of performance, efficiency, and cost-effectiveness.

Industrial Impact

The adoption of automotive 48V systems is having a profound impact on the automotive industry, reshaping vehicle design and driving advancements in electrification. These systems enable automakers to integrate energy-efficient solutions into their vehicles, enhancing fuel economy, reducing emissions, and improving overall performance without the complexity of high-voltage systems. By supporting key electrified components such as mild-hybrid powertrains, electric power steering, and regenerative braking, 48V systems help manufacturers meet stringent environmental regulations while addressing consumer demand for more sustainable, cost-effective vehicles. Moreover, the increased efficiency of power distribution provided by these systems allows for the incorporation of innovative features such as active suspension systems and advanced lighting technologies, further elevating the driving experience. The industrial impact extends beyond automotive manufacturers to suppliers of electronic components, batteries, and power management systems, creating new opportunities for innovation and collaboration within the supply chain. As the demand for electric and hybrid vehicles continues to grow, the market for 48V systems is expected to expand, driving technological developments in energy storage, power electronics, and vehicle integration. The widespread adoption of 48V technology also positions automakers to transition smoothly into fully electric powertrains by providing a scalable, cost-efficient stepping stone toward more complex high-voltage systems. In essence, automotive 48V systems are facilitating a transformation in the industry, promoting sustainability, enhancing vehicle performance, and opening up new avenues for technological innovation across the value chain.

Market Segmentation:

Segmentation 1: by Component Type

• Batteries

• DC/DC Converters

• Starter?Generators

• Inverters

• Others

Batteries to Dominate the Automotive 48V Systems Market (by Component Type)

Batteries are expected to dominate the automotive 48V systems market by component type, playing a critical role in powering the various electrified components within vehicles. As the primary energy source in 48V systems, batteries enable the efficient operation of mild-hybrid powertrains, regenerative braking, and electric steering, ensuring optimal performance and energy recovery. With the growing emphasis on fuel efficiency and reducing emissions, the demand for advanced, high-capacity batteries is rising. These batteries offer a cost-effective solution for automakers to implement electrification without fully transitioning to high-voltage electric systems. Additionally, improvements in battery technology, such as enhanced energy density and longer life cycles, are driving greater adoption of 48V systems. As automakers increasingly prioritize sustainability and energy efficiency, the battery segment will continue to lead the market, facilitating the integration of electrified systems in both passenger and commercial vehicles.

Segmentation 2: by Vehicle Type

• Passenger Vehicles

• Commercial Vehicles

Passenger Vehicles to Dominate the Automotive 48V Systems Market (by Vehicle Type)

Passenger vehicles are set to dominate the automotive 48V systems market, driven by the growing demand for fuel-efficient and environmentally friendly transportation solutions. As consumers increasingly prioritize sustainability, automakers are turning to 48V systems to enhance the performance of mild-hybrid powertrains, improve fuel efficiency, and reduce emissions in passenger vehicles. The adoption of 48V technology in this segment allows for the integration of advanced features such as regenerative braking, electric power steering, and active suspension systems, all of which contribute to a better driving experience and greater energy recovery. Additionally, passenger vehicles benefit from 48V systems as a cost-effective solution for achieving higher efficiency without the complexity of full hybrid or electric systems. As the market for electric and hybrid passenger vehicles continues to expand, 48V systems will play a key role in shaping the future of personal mobility, making this segment the dominant force in the overall market.

Segmentation 3: by Propulsion Type

• Mild-Hybrid Electric Vehicles (MHEVs)

• Battery Electric Vehicles (BEVs)

MHEVs to Dominate the Automotive 48V Systems Market (by Propulsion Type)

Mild Hybrid Electric Vehicles (MHEVs) are poised to dominate the automotive 48V systems market, driven by their cost-effectiveness and ability to deliver significant fuel efficiency improvements. MHEVs utilize 48V systems to support electrified components such as mild-hybrid powertrains, regenerative braking, and electric power steering, enabling automakers to meet increasingly stringent emissions regulations while maintaining vehicle performance. The demand for MHEVs is growing due to their affordability compared to full hybrids and electric vehicles, making them an attractive option for both manufacturers and consumers. With automakers seeking to balance performance, fuel efficiency, and cost, MHEVs equipped with 48V systems offer an optimal solution. As the automotive industry continues to prioritize sustainability and energy efficiency, MHEVs are expected to capture a significant share of the market, further driving the adoption of 48V technology in both passenger and commercial vehicle segments.

Segmentation 4: by Architecture Type

• Belt Driven (P0)

• Crankshaft Mounted (P1)

• Transmission-Mounted (P2/P3)

• Transmission Output/Rear Axle (P4)

Belt Driven (P0) to Dominate the Automotive 48V Systems Market (by Architecture Type)

Belt-driven (P0) architectures are expected to dominate the automotive 48V systems market by architecture type, owing to their cost-effectiveness and simplicity in integration. The P0 architecture, which connects the 48V motor directly to the engine via a belt, provides significant benefits in terms of fuel efficiency and power delivery while minimizing the complexity of system design. This architecture is commonly used in mild-hybrid applications, where it supports functions such as engine start-stop, regenerative braking, and power steering. Its widespread adoption is driven by automakers seeking to reduce emissions and improve fuel economy in a cost-efficient manner without the need for extensive modifications to the vehicle’s powertrain. The P0 architecture also facilitates easy integration into existing vehicle platforms, making it a preferred choice for manufacturers looking to offer electrified solutions with minimal cost and operational disruption. As demand for mild-hybrid vehicles grows, the P0 architecture is expected to maintain its dominant position in the market.

Segmentation 5: by Region

• North America: U.S., Canada, and Mexico

• Europe: Germany, France, U.K., Italy, and Rest-of-Europe

• Asia-Pacific: China, Japan, South Korea, India, and Rest-of-Asia-Pacific

• Rest-of-the-World: South America and Middle East and Africa

Asia-Pacific is expected to dominate the automotive 48V systems market, driven by the region’s leadership in electric vehicle production and the growing demand for energy-efficient transportation. Countries such as China, Japan, and South Korea are at the forefront of adopting 48V systems in both hybrid and electric vehicles, supported by strong government incentives and regulatory pressures to reduce emissions. Additionally, the region's automotive manufacturers are investing heavily in 48V technology to enhance fuel efficiency, meet stringent environmental standards, and stay competitive in the global market. The growing consumer preference for eco-friendly vehicles, combined with Asia-Pacific's dominance in manufacturing and supply chain capabilities, positions the region as the key driver of 48V system adoption. As the market for mild-hybrid and electric vehicles expands, Asia-Pacific is poised to maintain its leadership role, capturing a significant share of the automotive 48V systems market in the coming years.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Rising Demand for Improved Fuel Economy

The demand for improved fuel economy is a significant driver in the automotive 48V systems market, as regulatory bodies across the globe push for stricter fuel consumption and emission standards. The Global Fuel Economy Initiative (GFEI) aims to halve the fuel consumption of new light-duty vehicles by 2030 compared to 2005 levels, requiring an annual reduction of about 4.3% from 2019 to 2030. To meet these targets, automakers are increasingly turning to 48V mild-hybrid technology, which plays a crucial role in fulfilling the stringent regulations set by countries worldwide. In the U.S., the National Highway Traffic Safety Administration (NHTSA) has established Corporate Average Fuel Economy (CAFE) standards, which mandate a fleet average of 50.4 miles per gallon for passenger cars and light trucks by 2031. Non-compliance with these standards results in significant penalties, making 48V systems a key technology to avoid such penalties. Additionally, in the European Union, the Euro 7 standards, effective in 2024, impose even stricter limits on pollutant emissions, with 48V systems playing an important role in meeting these limits through features such as electrically heated catalysts. In China, aggressive Phase V fuel consumption standards are set to reduce fleet average consumption to 4.0 liters per 100 kilometers by 2025, with a target of 3.2 liters per 100 kilometers by 2030, further increasing the demand for 48V systems to comply with these ambitious goals. Research has shown that 48V mild-hybrid systems, particularly configurations such as belt-alternator starter (P0) and P2 systems, contribute significantly to reducing CO2 emissions, with potential reductions of up to 7.8% on the New European Driving Cycle (NEDC). Beyond regulatory compliance, 48V systems offer a cost-effective solution for automakers, providing fuel economy improvements through features such as torque assist, regenerative braking, and start-stop functionality, without the high costs and complexities of full electrification. As the push for fuel economy advancements intensifies, 48V systems are becoming an essential technology for automakers to meet evolving regulations while balancing cost and performance.

Market Challenges: System Complexity and Integration

The integration of 48V systems into modern automotive designs presents notable challenges due to the increased system complexity. One of the primary hurdles is the need to harmonize both 12V and 48V architectures within a single vehicle. Many existing vehicle systems, such as lighting and sensors, still rely on 12V power, requiring sophisticated engineering solutions to ensure that both power sources function seamlessly together. Additionally, the transition to 48V systems demands significant modifications to traditional power delivery networks (PDNs), which have been predominantly 12V for decades. The complexity has been compounded by the lack of established standards, making the design and testing of new systems more difficult and time-consuming. Despite these challenges, the integration of 48V systems is a driver for the automotive industry as it enables higher performance and greater fuel efficiency, addressing stringent emissions regulations while supporting the adoption of advanced technologies such as ADAS and energy recovery systems. Consequently, overcoming system complexity is crucial for automakers to leverage the full benefits of 48V electrification in their vehicles.

Market Opportunities: Commercial and Micro-Mobility Vehicle Electrification

The electrification of commercial and micro-mobility vehicles through 48V systems presents OEMs with key opportunities to enhance vehicle efficiency and sustainability. These systems deliver instant torque, improving acceleration and providing near-silent operation, which enhances driver comfort and reduces urban noise pollution. Regenerative braking boosts fuel efficiency by up to 15%, reduces brake wear, and lowers maintenance costs, making it an attractive option for commercial fleets. Additionally, the ability to capture and store energy during braking further optimizes overall vehicle performance and reduces operational costs.

The modular, passive-cooled 48V battery packs allow for cost-effective integration into light commercial vans and e-cargo bikes without the need for extensive reengineering, accelerating market entry. By supporting electrified steering and HVAC, 48V systems reduce the complexities of high-voltage safety, making them well-suited for smaller vehicles. The ability to integrate these systems with advanced software platforms also facilitates the development of software-defined vehicles, allowing for greater flexibility and vehicle customization. While vehicle-to-grid potential exists, it requires further infrastructure development, presenting an opportunity for future market growth.

Early adoption of 48V systems strengthens OEM sustainability efforts, ensures compliance with Euro 7 and EPA standards, and positions companies as leaders in cost-effective electrification. Moreover, the scalability of 48V solutions enhances fleet management and extends the lifecycle of commercial vehicles, further driving the market's expansion. These advantages position OEMs adopting 48V systems as key players in both the present and future of electrified transportation.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “The automotive 48V systems market is positioned for robust growth, largely driven by the increasing shift toward electrification and the adoption of hybrid technologies. MHEVs will dominate the market, offering a balance of performance, fuel efficiency, and cost-effectiveness. As automakers face stricter emissions regulations, the integration of 48V systems in passenger vehicles is accelerating, with these systems enhancing overall vehicle efficiency without the complexity of high-voltage alternatives. The Asia-Pacific region is expected to lead market growth due to its strong automotive manufacturing base and rising demand for hybrid and electric vehicles. Belt-driven (P0) architectures will continue to be the preferred choice, offering a straightforward and affordable solution for automakers to incorporate 48V technology into their vehicles.”

Automotive 48V Systems Market - A Global and Regional Analysis

Focus on Application, Product, and Regional Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Automotive 48V systems are advanced electrical architectures that provide higher power capacity than traditional 12V systems. They support electrified vehicle components such as mild-hybrid powertrains, electric power steering, and regenerative braking. These systems improve fuel efficiency, reduce emissions, and enable energy recovery. Automotive 48V systems also allow for more efficient power distribution, enabling features like active suspension systems and advanced lighting. By reducing weight and improving energy transfer, they offer a cost-effective solution for integrating electrification without fully transitioning to high-voltage electric systems.

Key business opportunities in the automotive 48V systems market include the growing demand for mild-hybrid and hybrid vehicles, which utilize 48V systems to improve fuel efficiency and reduce emissions. Manufacturers can capitalize on this trend by developing advanced 48V architectures and components, such as batteries, power electronics, and regenerative braking systems. Additionally, there is significant potential in the Asia-Pacific region, driven by strong demand for electric vehicles and government incentives. Companies that innovate in energy storage, power management, and lightweight materials can further enhance the performance of 48V systems, unlocking new growth opportunities in both passenger and commercial vehicle segments.

To strengthen their market position in the automotive 48V systems industry, existing players have been adopting several strategic initiatives:

• Strategic Partnerships and Collaborations: Companies have been forming alliances with technology providers, research institutions, and other industry stakeholders to accelerate innovation and expand their product portfolios.

• Investment in Research and Development: Significant resources are being allocated to develop advanced battery storage technologies, aiming to enhance the efficiency and scalability of battery production.

• Geographical Expansion: Firms are entering new markets to capitalize on regional demand for energy storage solutions, thereby broadening their global footprint.

• Product Development: Emphasis is placed on creating technologically advanced and flexible energy storage solutions that enhance efficiency.

• Mergers and Acquisitions: Companies have been engaging in M&A activities to acquire complementary technologies and expertise, facilitating rapid market penetration and diversification.

A new company entering the automotive 48V systems market should focus on several key areas to stay ahead of the competition. First, innovation in energy storage solutions, such as advanced batteries with higher energy density and longer lifespans, will be critical. Developing lightweight, efficient power management systems and enhancing the performance of regenerative braking and electric power steering can also differentiate the company. Additionally, forming strategic partnerships with OEMs and component suppliers to integrate 48V systems seamlessly into vehicle platforms will help drive adoption. Focusing on sustainability, cost-effective solutions, and rapid scalability will also be essential in attracting both automakers and consumers.

The USP of this report lies in its comprehensive coverage of the automotive 48V systems market, offering a detailed analysis of cutting-edge technologies, analysis of architecture type, component type, vehicle type, and propulsion type. It provides actionable insights into market dynamics, including drivers, challenges, and opportunities, supported by real-world case studies and competitive benchmarking. The report uniquely highlights regulatory frameworks, sustainability goals, and technological advancements shaping the market, empowering stakeholders to make informed strategic decisions. With a forward-looking approach, it identifies untapped revenue opportunities and key growth strategies, making it an indispensable resource for navigating this rapidly evolving industry.

This report is ideal for industry stakeholders such as automotive 48V systems providers, component suppliers, distributors, and new market entrants seeking to explore opportunities in the automotive 48V systems market. Investors and venture capitalists aiming to identify high-growth areas in grid storage systems will find valuable insights. Government bodies and regulatory authorities can use it to understand market trends and align policies with sustainability goals. Additionally, research institutions and consulting firms focused on advancing energy storage technologies will benefit from its in-depth analysis of market dynamics, innovations, and competitive strategies.