A quick peek into the report

Autonomous Emergency Steering Systems Market: Industry Overview

The autonomous emergency steering systems market is a crucial component within the broader Advanced Driver-Assistance Systems (ADAS) and autonomous vehicle technology landscape. As vehicle automation continues to evolve, safety systems such as AESS are becoming vital to ensuring the smooth transition from driver-controlled to fully autonomous driving. AESS is designed to intervene during emergency situations, autonomously steering the vehicle to avoid collisions or mitigate their impact, significantly enhancing road safety.

The industry is characterized by rapid technological innovation and growing investments in automation and safety technologies. AESS systems use a combination of advanced sensors (such as LiDAR, radar, and cameras) and sophisticated AI algorithms to detect imminent hazards and autonomously steer the vehicle away from danger. These technologies are now being integrated into semi-autonomous vehicles, with further advancements being made for fully autonomous systems.

Autonomous Emergency Steering Systems Market Lifecycle Stage

The autonomous emergency steering systems market is in the late-stage R&D and early commercialization phase, with technologies at Technology Readiness Levels (TRLs) 4–7. The focus is on refining prototypes, integrating advanced sensors, and developing AI algorithms for reliable emergency steering performance. Companies are transitioning from concept development to engineering pilots, with real-world testing and validation a priority.

Collaborations between automotive manufacturers, technology providers, and tier-1 suppliers are key as AESS technologies are integrated into vehicles with advanced driver-assistance systems (ADAS). Regulatory frameworks and safety standards are also being refined to support broader deployment.

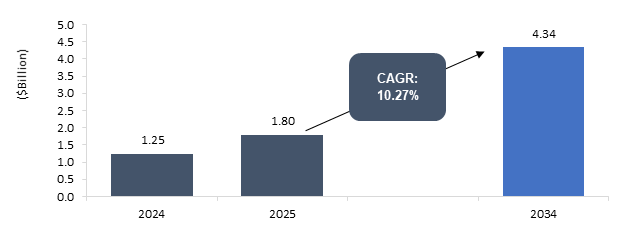

Commercial AESS deployment is expected in the mid-2020s, as manufacturers scale production to meet rising demand for enhanced safety in semi-autonomous and autonomous vehicles. Significant capital is flowing into R&D, with partnerships critical for the success of AESS technologies. As the market matures, AESS will become a standard feature in autonomous and semi-autonomous vehicles, revolutionizing automotive safety.

Autonomous Emergency Steering Systems Market Segmentation:

Segmentation 1: by Technology

• Lidar-Based AESS

• Camera-Based AESS

• Radar-Based AESS

• Sensor Fusion-Based AESS

Segmentation 2: by Level of Automation

• Semi-Autonomous (Level 1 to Level 3)

• Fully Autonomous (Level 4 and 5)

Segmentation 3: by Vehicle Type

• Passenger Cars

• Commercial Vehicles

Segmentation 4: by Application

• Sensors

• Control Units

• Steering Mechanism

• Software

• Communication Systems

Segmentation 5: by Region

• North America - U.S., Canada, and Mexico

• Europe - Germany, France, Italy, Spain, U.K., and Rest-of-Europe

• Asia-Pacific - China, Japan, South Korea, India, and Rest-of-Asia-Pacific

• Rest-of-the-World - South America and Middle East and Africa

In the autonomous emergency steering systems market, Asia-Pacific is anticipated to gain traction in terms of production, with increasing infrastructure demand and government initiatives.

Demand – Drivers and Limitations

The following are the demand drivers for the autonomous emergency steering systems market:

• Increasing demand for advanced vehicle safety features

• Growing adoption of semi-autonomous and autonomous vehicles

• Advancements in sensor technology and AI algorithms

The autonomous emergency steering systems market is expected to face some limitations as well due to the following challenges:

• High development and production costs limit affordability

• Regulatory variability across regions complicates global deployment

Analyst Thoughts

According to Debraj Chakraborty, Principal Analyst, BIS Research, “The autonomous emergency steering systems market is at a critical growth stage, with significant R&D investments and pilot programs validating key technologies like sensor fusion and AI-driven steering. As partnerships with automotive manufacturers and regulators evolve, AESS will soon be integrated into semi-autonomous and autonomous vehicles, driving safer driving and reducing accidents. With economies of scale, standardized components, and mass production, AESS will transition from a niche feature to a standard in global vehicle safety, reshaping the automotive landscape and paving the way for autonomous driving technologies.”

Autonomous Emergency Steering Systems Market - A Global and Regional Analysis

Focus on Technology, Level of Automation, Vehicle Type, Components, and Country Analysis - Analysis and Forecast, 2025-2034

Frequently Asked Questions

BIS Research has considered autonomous emergency steering as an advanced safety system that automatically steers a vehicle to avoid or mitigate the effects of an imminent collision, using real-time data from various sensors and AI-powered algorithms.

The autonomous emergency steering systems market is evolving rapidly, driven by key trends such as the integration of autonomous emergency steering systems into broader advanced driver assistance systems (ADAS), enhancing vehicle safety during emergency situations. the adoption of steer-by-wire technology is enabling more precise and flexible steering responses, crucial for autonomous driving. stricter regulatory standards are pushing automakers to enhance autonomous emergency steering systems capabilities to meet safety requirements, while increasing consumer awareness and trust in autonomous driving technologies is fostering demand for transparent communication about autonomous emergency steering systems features. these trends are shaping the market and positioning autonomous emergency steering systems as a critical component in the future of automotive safety systems.

To strengthen their position in the autonomous emergency steering systems market, players are investing in R&D to improve AI, sensors, and system integration. They are forming strategic partnerships, expanding into emerging markets, and developing cost-effective, scalable solutions. Companies are also focusing on real-world testing, enhancing V2X connectivity, reducing production costs, and pursuing mergers and acquisitions to acquire specialized technologies. These strategies aim to accelerate the adoption of autonomous emergency steering systems in autonomous vehicles and ADAS.

A new company entering the autonomous emergency steering systems market should focus on developing innovative sensor technologies, advanced AI-driven algorithms, and modular, scalable solutions to differentiate itself from competitors. Offering cost-effective systems that are easily integrated into various vehicle types, while emphasizing V2X connectivity, real-world testing, and regulatory compliance, will help attract OEMs and consumers. Forming strategic partnerships with automotive manufacturers and technology providers will accelerate market entry, while customer education on the safety benefits of autonomous emergency steering systems will foster trust and adoption. These strategies will enable the company to stay ahead in the competitive autonomous emergency steering systems landscape.

The following can be termed as some of the USPs of the report:

• Extensive competitive benchmarking of 15 key players to offer a holistic view of the global autonomous emergency steering market landscape

• Market segregation based on technology, level of automation, vehicle type, application and end-user.

• Investment landscape, including product adoption scenario, funding, and patent analysis

Ans: The companies that produce and commercialize autonomous emergency steering systems, end-user sectors, research institutions, and regulatory bodies involved in the autonomous emergency steering systems market should buy this report.