Published Year: 2020

Global Memory Market for Connected and Autonomous Vehicle: Focus on Memory Type, Level of Autonomy,

The Memory for Connected and Autonomous Vehicle Industry Analysis by BIS Research projects the...

Focus on Application, Vehicle Type, Network Type, Sales Channel, Form, Transponder, Hardware, and Country-Level Analysis - Analysis and Forecast, 2024-2034

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

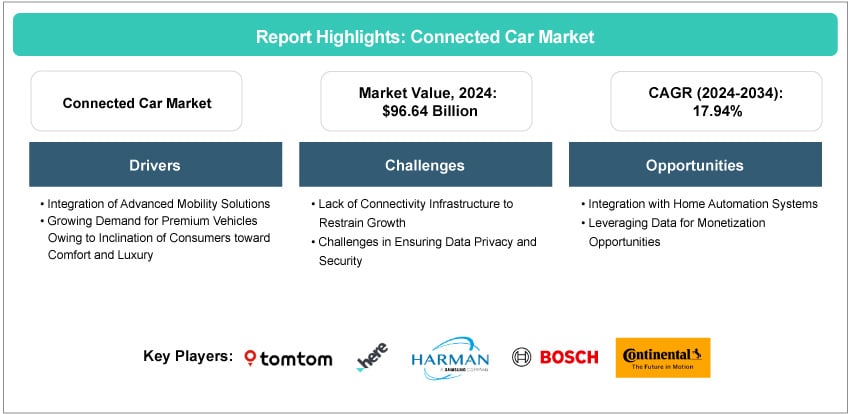

The global connected car market is set to witness significant growth, with its market size projected to expand from $96.64 billion in 2024 to approximately $503.13 billion by 2034, reflecting a 17.94% CAGR in a realistic scenario. Driven by rising consumer demand for advanced safety, infotainment, and telematics solutions, the market is witnessing rapid integration of vehicle-to-everything (V2X) communication, AI-driven mobility services, and 5G connectivity. The Asia-Pacific region is expected to dominate due to strong government support, growing urbanization, and technological advancements in countries such as China, Japan, and South Korea. The North America and Europe markets are also expanding, fueled by stringent regulations on vehicle safety and emissions, alongside increasing adoption of autonomous and electric vehicles. Key players such as Tesla, Ford, Continental AG, and Qualcomm are investing heavily in connected mobility innovations, smart telematics, and software-defined vehicles, further enhancing market competitiveness.

Introduction of Connected Car

The study conducted by BIS Research highlights connected cars as a significant evolution in automotive technology, integrating advanced communication systems to enable real-time data exchange between vehicles, infrastructure, and external networks. These vehicles leverage technologies such as telematics, vehicle-to-everything (V2X) communication, and IoT-based solutions to enhance safety, convenience, and overall driving experience. The increasing adoption of 5G, AI, and cloud-based platforms has further strengthened connectivity, allowing for features such as remote diagnostics, predictive maintenance, infotainment, and autonomous driving support. With stringent regulatory requirements emphasizing road safety, emissions reduction, and cybersecurity, automakers and technology providers are investing in smart mobility solutions to improve efficiency and user experience. The connected car market is rapidly growing, driven by consumer demand for enhanced vehicle intelligence, real-time navigation, and advanced driver-assistance systems (ADAS), positioning it as a key pillar in the future of intelligent transportation.

Market Introduction

The connected car market has evolved significantly over the years, transitioning from basic in-car connectivity features to a sophisticated ecosystem of real-time vehicle communication, automation, and advanced mobility solutions. The market is expected to witness exponential growth, with projections reaching over $500 billion by 2034. The increasing demand for smart mobility, real-time data insights, and enhanced vehicle security will continue to fuel innovation. The Asia-Pacific region is set to dominate the market, driven by strong 5G infrastructure, rapid urbanization, and government-backed smart transportation initiatives. Moreover, the integration of cloud-based platforms, AI-powered driving assistance, and connected vehicle monetization models will redefine automotive experiences. While challenges such as cybersecurity risks and infrastructure gaps remain, the future of connected cars is geared toward an autonomous, sustainable, and fully integrated digital mobility ecosystem.

Industrial Impact

The connected car market is driving significant industrial transformation, impacting multiple automotive, telecommunications, insurance, and technology sectors. Automakers are increasingly integrating vehicle-to-everything (V2X) communication, advanced telematics, and artificial intelligence (AI) to enhance safety, efficiency, and user experience. The telecommunications industry benefits from rising demand for 5G connectivity, enabling seamless real-time data exchange. Additionally, the insurance sector is adapting to usage-based insurance (UBI) models, leveraging telematics to offer personalized premium pricing. The market is also fostering sensor technology, cybersecurity, and cloud computing growth as real-time monitoring and predictive analytics become industry standards. Government regulations focused on safety, emissions, and data security are further shaping the ecosystem, driving innovation and strategic partnerships. Overall, the connected car market is accelerating digital transformation across industries, enhancing mobility solutions, smart city integration, and autonomous driving advancements.

Market Segmentation:

Segmentation 1: by Application

• Mobility Management

• Telematics

• Infotainment

• Driver Assistance

• Navigation

• Others (eCall, Autopilot, Remote Diagnostics, Home Integration)

Driver Assistance Segment to Dominate the Connected Car Market (by Application)

The driver assistance segment is leading in the connected car market due to the increasing adoption of advanced driver assistance systems (ADAS), which enhance vehicle safety and driving efficiency. Features such as adaptive cruise control, lane departure warning, automated emergency braking, and blind-spot monitoring are becoming standard in modern vehicles, driven by stringent government safety regulations and consumer demand for enhanced security. As autonomous driving technology advances, the integration of AI and real-time vehicle-to-everything (V2X) communication will further propel the adoption of driver assistance systems, reinforcing their dominance in the market.

Segmentation 2: by Vehicle Type

• Internal Combustion Engine (ICE) Vehicle

• Battery Electric Vehicle (BEV)

• Hybrid Electric Vehicle (HEV)

• Plug-in Hybrid Electric Vehicle (PHEV)

Internal Combustion Engine (ICE) Vehicles to Dominate the Connected Car Market (by Vehicle Type)

Despite the growing push toward electrification, internal combustion engine (ICE) vehicles still dominate the connected car market due to their large existing consumer base and well-established infrastructure. The presence of connected features such as real-time diagnostics, telematics, and infotainment systems in ICE vehicles is expanding as automakers aim to improve fuel efficiency and vehicle longevity. However, while electric and hybrid vehicles (EVs and HEVs) are rapidly growing, ICE vehicles hold a significant market share due to their affordability and widespread availability across developed and developing markets.

Segmentation 3: by Network Type

• Operational Data

• Dedicated Short-Range Communication (DSRC)

• Cellular

• Satellite

Cellular to Dominate the Connected Car Market (by Network Type)

Cellular connectivity is the dominant network type in the connected car market, primarily driven by the expansion of 4G and 5G networks globally. Cellular-based V2X communication enables real-time vehicle monitoring, remote diagnostics, software updates, and navigation services, making it the preferred choice for automakers and service providers. The rollout of 5G technology is expected to enhance low-latency communication further, support advanced autonomous driving applications, and enable seamless over-the-air (OTA) software updates, ensuring cellular remains the leading connectivity type.

Segmentation 4: by Sales Channel

• Original Equipment Manufacturer (OEM)

• Aftermarket

Original Equipment Manufacturers (OEMs) to Dominate the Connected Car Market (by Sales Channel)

OEMs dominate the sales channel segment as they integrate connected technologies directly into vehicles at the manufacturing stage, ensuring seamless hardware and software integration. Automakers collaborate with technology providers, telecom companies, and software developers to enhance connectivity, infotainment, and safety features. As the demand for factory-installed telematics, AI-based driver assistance, and cloud-based services increases, OEMs maintain a competitive advantage by offering pre-installed, high-performance connected solutions compared to aftermarket alternatives.

Segmentation 5: by Form

• Embedded

• Integrated

Integrated Connectivity to Dominate the Connected Car Market (by Form)

Integrated connectivity is the leading form in the connected car market due to its flexibility and enhanced user experience. Integrated systems allow seamless communication between mobile devices and vehicle infotainment systems, offering navigation, streaming services, real-time diagnostics, and remote-control features. Consumers prefer this model as it provides a hybrid approach, leveraging both embedded and tethered connectivity, ensuring continuous access to cloud-based applications and services while optimizing costs for manufacturers and users.

Segmentation 6: by Transponder

• Onboard Unit

• Roadside Unit

Onboard Unit to Dominate the Connected Car Market (by Transponder)

Onboard units (OBUs) are forecasted to be the dominant transponder type, as they are crucial for V2X communication and connected mobility solutions. OBUs facilitate toll collection, fleet management, automated emergency alerts, and real-time traffic updates, significantly improving vehicle efficiency and safety. With governments investing in smart city infrastructure and intelligent transport systems (ITS), OBUs are becoming essential in modern vehicles, ensuring their sustained dominance in the market.

Segmentation 7: by Hardware

• Head Unit

• Central Gateway

• Intelligent Antennas

• Electronic Control Unit (ECU)

• Telematics Control Unit

• Keyless Entry System

• Sensors

Telematics Control Unit (TCU) to Dominate the Connected Car Market (by Hardware)

The telematics control unit (TCU) leads the hardware segment as it acts as the central hub for connected vehicles, enabling cellular communication, GPS tracking, vehicle diagnostics, and over-the-air updates. As automakers prioritize remote monitoring, predictive maintenance, and AI-powered mobility solutions, TCUs have become indispensable in modern vehicle architectures. The rising adoption of fleet management services, connected insurance models, and real-time data analytics ensures TCUs remain the most critical hardware component in connected cars.

Segmentation 8: by Region

• North America (U.S., Canada, Mexico)

• Europe (Germany, France, U.K., Italy, Rest-of-Europe)

• Asia-Pacific (China, Japan, India, South Korea, Rest-of-Asia-Pacific)

• Rest-of-the-World (South America, Middle East and Africa)

Asia-Pacific to Dominate the Connected Car Market (by Region)

The Asia-Pacific region is the dominant market for connected cars, driven by rapid urbanization, strong government support for smart mobility initiatives, and extensive 5G deployment. Countries such as China, Japan, and South Korea lead the adoption of connected vehicle technologies, benefiting from a well-established automotive and electronics industry. The increasing demand for advanced driver assistance systems (ADAS), infotainment, and real-time vehicle diagnostics fuels market growth. Additionally, governments are implementing strict safety and emission regulations, encouraging automakers to integrate telematics and vehicle-to-everything (V2X) communication. The expansion of electric vehicle (EV) production and the rising number of partnerships between automakers and tech companies further strengthen Asia-Pacific’s dominance in the global connected car market.

Recent Developments in the Connected Car Market

• In 2023, Continental AG launched next-generation telematics and real-time data management platforms, equipping automakers with enhanced vehicle navigation, communication, and infotainment capabilities.

• In May 2023, Toyota Motor Corporation revealed a decade-long data breach caused by a cloud misconfiguration, exposing the location information of approximately 2.15 million connected car customers. The breach lasted from November 2013 to April 2023 and included sensitive data such as vehicle GPS terminal IDs and chassis numbers. Although the company reported no evidence of misuse, the incident highlights the critical data privacy and security risks within the connected car market.

• In 2023, General Motors (GM) faced a lawsuit from the Texas Attorney General for allegedly collecting and selling driver data without proper authorization. The complaint accused GM of gathering data from 1.8 million vehicle owners in Texas and selling it to companies such as LexisNexis Risk Solutions and Verisk Analytics without clear communication to consumers. This incident underscores the complexities and potential pitfalls automakers encounter in data monetization, highlighting the necessity for transparent data practices and robust privacy protections.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Integration of Advanced Mobility Solutions

The integration of advanced mobility solutions is a key driver for the connected car market, enabling seamless access to ridesharing, car-sharing, and mobility-as-a-service (MaaS) platforms. These solutions enhance convenience, reduce ownership costs, and provide efficient transportation options for consumers. Additionally, connected cars equipped with advanced mobility features enable real-time route optimization, traffic management, and vehicle diagnostics, improving the overall travel experience. As urbanization and demand for smart transportation grow, the adoption of connected cars integrated with advanced mobility solutions continues to rise, shaping the future of mobility.

Companies such as ZF Aftermarket have been providing solutions to support the integration and maintenance of ADAS systems, particularly in the commercial vehicle sector. With mandates for driver assistance systems becoming more stringent, in February 2024, ZF Aftermarket introduced original equipment (OE)-quality sensors under its WABCO brand, with comprehensive support to ensure compliance and maximize safety. By providing essential components and repair kits, the company facilitates efficient and high-quality repairs, demonstrating its commitment to meeting the evolving needs of the automotive market while enhancing safety and reliability.

Market Challenges: Lack of Connectivity Infrastructure to Restrain Growth

The lack of robust connectivity infrastructure is a significant restraint for the connected car market. Many regions, especially in developing countries, face challenges such as limited 5G network coverage, inadequate roadside units for vehicle-to-infrastructure (V2I) communication, and inconsistent internet availability. These limitations hinder the seamless functionality of connected car features, such as real-time navigation, autonomous driving, and over-the-air updates. Addressing these gaps requires substantial investments in network expansion and the development of smart transportation infrastructure to support the growing demands of connected vehicles.

In 2022, the discontinuation of AT&T's 3G services left drivers of certain Volkswagen models without access to connected features such as remote start and emergency assistance. This incident highlights how the lack of updated connectivity infrastructure can disrupt connected car functionalities, underscoring the necessity for continuous network upgrades to support these services.

Market Opportunities: Integration with Home Automation Systems

Integration with home automation systems presents a significant opportunity for the connected car market as it enhances user convenience and lifestyle connectivity. Connected cars can seamlessly interact with smart home devices, allowing features such as pre-setting home temperature, controlling lighting, and managing security systems directly from the vehicle. This integration appeals to tech-savvy consumers, driving adoption and creating new avenues for partnerships between automakers and smart home technology providers.

In 2021, Alarm.com introduced a connected car solution that integrates vehicle monitoring with smart home automation. This system allows users to receive real-time vehicle diagnostics and control home devices, such as lights and thermostats, based on the car's location, enhancing convenience and security.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, the connected car market has been undergoing rapid transformation, driven by technological advancements, regulatory mandates, and changing consumer preferences. The increasing adoption of 5G, AI-powered telematics, and vehicle-to-everything (V2X) communication is enhancing safety, navigation, and autonomous driving capabilities. OEMs and technology providers are forging strategic partnerships to expand connectivity solutions, improve data security, and enable seamless over-the-air (OTA) updates. While Asia-Pacific leads the market due to strong government support and 5G expansion, North America and Europe remain key players, benefiting from strict safety regulations and innovation-driven automakers. Despite challenges such as data privacy concerns and high infrastructure costs, the market is set to witness substantial growth, with AI-driven telematics, smart mobility, and cloud-based services shaping the future. Automakers and telecom companies that embrace software-defined vehicle architectures and intelligent fleet management solutions will emerge as key players in this evolving ecosystem.

Focus on Application, Vehicle Type, Network Type, Sales Channel, Form, Transponder, Hardware, and Country-Level Analysis - Analysis and Forecast, 2024-2034

Ans: The connected car market offers vehicles equipped with advanced communication technologies that enable seamless connectivity between vehicles, infrastructure, cloud platforms, and external devices. These cars leverage IoT, AI, 5G, telematics, and vehicle-to-everything (V2X) communication to enhance safety, navigation, infotainment, and remote diagnostics. The market plays a crucial role in autonomous driving advancements, smart mobility solutions, and real-time data analytics, transforming the future of transportation.

Ans: The connected car market presents multiple business opportunities, including:

• 5G and IoT Solutions: Development of 5G-enabled telematics and IoT-based vehicle monitoring systems

• AI and Data Analytics: Offering real-time predictive analytics for driver behavior, fleet management, and maintenance

• Autonomous Vehicle Technologies: Manufacturing advanced driver assistance systems (ADAS) and AI-driven navigation solutions

• Cloud-Based Platforms: Providing software for over-the-air (OTA) updates, infotainment, and remote diagnostics

• Cybersecurity Solutions: Developing end-to-end encryption and data protection measures for connected vehicles

• Smart Mobility Services: Offering vehicle-to-infrastructure (V2I) solutions and connected fleet management platforms

Ans: Companies in the connected car market are implementing various strategic initiatives to maintain a competitive edge:

• Mergers and Acquisitions: Automotive and tech companies are acquiring telematics and AI firms to enhance their vehicle connectivity solutions. For example, Qualcomm made an acquisition with Veoneer’s Arriver business to improve autonomous driving capabilities.

• Strategic Partnerships and Collaborations: Automakers are partnering with telecom providers and AI firms to integrate next-gen connectivity solutions. For example, Ford and Google formed a partnership to bring AI-powered infotainment and cloud computing into their vehicles.

• Product Innovation and Development: Continuous investment in R&D is enabling companies to launch V2X communication, ADAS, and 5G-based vehicle connectivity solutions.

• Expansion into Emerging Markets: Recognizing the demand for connected vehicles, companies are targeting regions such as Asia-Pacific and the Middle East for growth.

• Digital Transformation Initiatives: Companies are adopting cloud computing, AI-powered diagnostics, and remote vehicle monitoring solutions to enhance vehicle performance.

Ans: A new company entering the connected car market should focus on:

• 5G-enabled V2X solutions for seamless vehicle communication and traffic optimization

• AI-powered predictive analytics for driver behavior monitoring and maintenance alerts

• Cloud-based software solutions for infotainment, navigation, and remote vehicle updates

• Cybersecurity frameworks to protect vehicle networks from cyber threats

• Autonomous vehicle technologies, including ADAS and automated driving systems

• Localization strategies for offering customized connected mobility solutions in emerging markets

Ans: The unique selling proposition (USP) of this report lies in its comprehensive analysis of the connected car market, offering in-depth insights into:

• Emerging technologies such as 5G, AI-driven telematics, and vehicle automation

• Market trends and key growth drivers, helping businesses identify strategic opportunities

• Detailed segmentation by application, vehicle type, network type, and region, aiding in targeted market entry

• Competitive benchmarking and key player analysis, providing actionable intelligence on market positioning

• Regulatory landscape insights, ensuring compliance with data security, cybersecurity, and vehicle safety standards

Ans: This report is essential for a wide range of stakeholders in the connected car market, including:

• Automotive Companies: To explore connected mobility trends, partnerships, and product innovations

• Technology Providers: To develop 5G, AI, and IoT solutions for enhanced vehicle connectivity

• Telecommunication Firms: To leverage opportunities in V2X communication and cloud-based vehicle platforms

• Government and Policy Makers: To understand cybersecurity regulations, safety standards, and smart city integrations

• Investors and Venture Capitalists: To identify high-growth sectors and make informed investment decisions

• Consulting and Research Firms: To provide market intelligence and strategic guidance to clients.

The Memory for Connected and Autonomous Vehicle Industry Analysis by BIS Research projects the...