Published Year: 2026

Analog X-ray Market - A Global and Regional Analysis: Focus on Product Type, Application, End User,

The global analog X-ray market is projected to reach $686.5 million by 2036 from $602.1...

Focus on Portability, Technology, Product Type, Application, End User, and Region - Analysis and Forecast, 2026-2036

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Introduction of the Digital X-ray Market

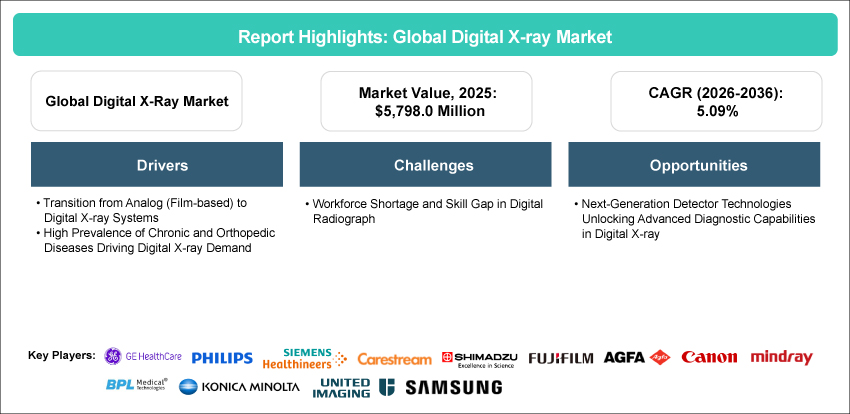

The global digital X-ray market, initially valued at $5,798.0 million in 2025, is projected to grow substantially, reaching $9,909.1 million by 2036, with a compound annual growth rate (CAGR) of 5.09% from 2026 to 2036.

The global digital X-ray market has been experiencing steady growth, driven by the ongoing transition from analog film-based and computed radiography workflows to fully digital radiography systems. Digital X-ray systems are widely used across hospitals, diagnostic imaging centers, orthopedic and specialty clinics, dental clinics, outpatient centers, emergency departments, and mobile diagnostic settings for chest imaging, orthopedic imaging, dental imaging, trauma assessment, emergency care, and general radiography applications. The market is supported by the increasing need for faster image acquisition, improved image quality, lower turnaround time, PACS/RIS connectivity, dose optimization, and more efficient clinical decision-making. Fixed digital X-ray systems continue to support high-volume radiology departments, while mobile digital X-ray systems are gaining relevance for bedside imaging, ICUs, emergency departments, operating rooms, inpatient wards, rural healthcare programs, and decentralized diagnostic services. In addition, retrofit digital X-ray solutions are enabling healthcare facilities to upgrade existing X-ray infrastructure with flat-panel detectors, acquisition software, and imaging consoles without replacing the entire system. Overall, the market is moving toward more connected, efficient, mobile, and accessible imaging solutions, supported by technological advancements, healthcare infrastructure investments, and growing imaging volumes.

Market Introduction

The global digital X-ray market represents a critical segment of the diagnostic imaging industry, covering digital radiography systems, computed radiography systems, fixed digital X-ray systems, mobile digital X-ray systems, digital general radiography systems, and retrofit digital X-ray solutions. These systems are used across hospitals, diagnostic imaging centers, orthopedic and specialty clinics, dental clinics, and other healthcare facilities for chest, orthopedic, dental, trauma, emergency, and general radiography applications.

The market has evolved significantly as healthcare providers continue to replace analog film-based systems and older computed radiography workflows with digital radiography platforms. Digital X-ray systems support immediate image availability, faster patient throughput, improved workflow efficiency, electronic image storage, PACS/RIS integration, and remote reporting. These advantages make them highly relevant in modern radiology departments, emergency care environments, outpatient imaging centers, and point-of-care settings.

The market is increasingly shaped by technological advancements such as flat-panel detector innovations, wireless detector platforms, improved image processing, dose-optimization tools, AI-enabled workflow support, and compact, mobile system designs. New digital X-ray systems are preferred in advanced hospitals and high-volume diagnostic centers due to their fully integrated architecture and ability to support connected imaging workflows. At the same time, retrofit digital X-ray systems are gaining traction in emerging markets and budget-sensitive facilities, as they provide a cost-effective route to digitize existing radiography infrastructure.

Companies operating in the market are focusing on advanced digital radiography platforms, mobile and portable systems, detector performance, workflow automation, software integration, dose efficiency, and service support. As healthcare systems continue to invest in diagnostic infrastructure, decentralized care, and digital health integration, Digital X-ray systems are expected to remain a core first-line imaging modality across global healthcare settings.

Industrial Impact

The global digital X-ray market has witnessed steady adoption, driven by the growing need for faster, more accurate, and connected diagnostic imaging across hospitals, diagnostic imaging centers, specialty clinics, dental facilities, and decentralized care settings. Key players such as GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., FUJIFILM Corporation, Canon Inc., Shimadzu Corporation, Konica Minolta, Agfa-Gevaert Group, Carestream Health, Samsung, Mindray, BPL Medical Technologies, United Imaging, OXOS Medical, and Acteon play an important role in advancing digital radiography adoption through fixed, mobile, and retrofit digital X-ray platforms.

These systems are widely used across chest imaging, orthopedic imaging, dental imaging, trauma assessment, emergency care, and general radiography applications. By enabling immediate image viewing, PACS/RIS connectivity, improved image quality, faster workflow, and reduced dependence on film handling, Digital X-ray systems are improving radiology department efficiency and supporting faster clinical decision-making.

The market’s impact is most visible in high-volume hospitals, emergency departments, diagnostic imaging centers, and healthcare systems investing in digital modernization. Mobile and portable digital X-ray systems are also expanding imaging access in ICUs, operating rooms, inpatient wards, rural healthcare programs, and community diagnostic services. However, workforce shortages, radiographer skill gaps, system integration challenges, and capital investment requirements continue to influence adoption, particularly in resource-constrained settings.

Market Segmentation:

Segmentation 1: By Portability

• Fixed Digital X-ray

• Mobile Digital X-ray

Fixed Digital X-ray Segment to Dominate the Digital X-ray Market (by Portability)

In 2025, fixed digital X-ray systems accounted for the largest market share due to their extensive utilization across hospitals, radiology departments, diagnostic imaging centers, orthopedic clinics, and specialty care facilities. These systems are widely preferred for high-volume imaging procedures and are suitable for chest, orthopedic, trauma, abdominal, dental, and general radiography examinations. Their ability to deliver consistent image quality, faster acquisition, high patient throughput, and seamless PACS/RIS integration supports their dominance in modern imaging facilities. Mobile Digital X-ray systems are expected to register faster growth, supported by rising demand for bedside imaging, point-of-care diagnostics, emergency imaging, ICU imaging, and decentralized healthcare delivery.

Segmentation 2: By Technology

• Digital Radiography

• Computed Radiography

Digital Radiography Segment to Dominate the Digital X-ray Market (by Technology)

In 2025, the digital radiography segment is expected to lead the digital X-ray market, supported by faster image acquisition, immediate image availability, improved workflow efficiency, better image quality, and stronger compatibility with PACS, RIS, electronic health record (EHR), cloud platforms, and AI-enabled imaging workflows. Digital radiography systems are increasingly preferred in high-volume hospitals, advanced diagnostic centers, emergency departments, and outpatient imaging facilities due to their ability to reduce turnaround time and improve operational efficiency. Computed radiography remains relevant in selected cost-sensitive and infrastructure-limited healthcare settings, but its long-term share is expected to gradually decline as facilities transition to direct digital radiography.

Segmentation 3: By Product Type

• New Digital X-Ray System

• Retrofit Digital X-Ray System

New Digital X-Ray System Segment to Dominate the Digital X-ray Market (by Product Type)

In 2025, new digital X-ray systems accounted for the largest market share due to their fully integrated architecture, advanced flat-panel detector technology, improved image processing, automated workflow features, and seamless compatibility with hospital IT systems. These systems are widely adopted by hospitals and diagnostic imaging centers, replacing legacy analog or computed radiography infrastructure. Retrofit Digital X-ray systems are expected to grow steadily as they provide a cost-effective digitization pathway for mid-tier hospitals, diagnostic centers, and budget-sensitive healthcare facilities by upgrading existing X-ray rooms with flat-panel detectors, acquisition software, and imaging consoles.

Segmentation 4: By Application

• Orthopedic Imaging

• Chest Imaging

• Dental Imaging

• Others

Chest Imaging Segment to Dominate the Digital X-ray Market (by Application)

In 2025, the chest imaging segment is expected to lead the Digital X-ray market, accounting for a significant share due to the large number of chest X-ray procedures performed for respiratory disease diagnosis, tuberculosis screening, cardiopulmonary assessments, emergency evaluation, pre-operative assessment, and routine medical examinations. Chest X-rays remain among the most frequently performed diagnostic imaging procedures in hospitals, diagnostic centers, public health programs, and outpatient facilities.

Segmentation 5: By End User

• Hospitals

• Orthopedic and Specialty Clinics

• Diagnostic Imaging Centers

• Other End Users

Hospitals to Dominate the Digital X-ray Market (by End User)

In terms of end user, the hospitals segment is expected to lead the digital X-ray market, supported by the high volume of routine, emergency, inpatient, outpatient, trauma, orthopedic, chest, and pre-surgical imaging procedures performed across multiple hospital departments. Hospitals rely on both fixed and mobile digital X-ray systems to support radiology departments, emergency departments, ICUs, operating rooms, inpatient wards, and outpatient diagnostic services.

Segmentation 6: By Region

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Rest-of-Europe

• Asia-Pacific

o China

o Japan

o India

o Australia

o South Korea

o Rest-of-Asia-Pacific

• Latin America

o Brazil

o Mexico

o Rest-of-Latin America

• Middle East and Africa

o K.S.A.

o U.A.E.

o South Africa

o Rest-of-Middle East and Africa

North America to Dominate the Digital X-ray Market (by Region)

In terms of region, North America is expected to lead the digital X-ray market, accounting for a significant share due to the region’s advanced healthcare infrastructure, high imaging procedure volumes, strong installed base of digital radiography systems, and continued replacement of legacy imaging platforms. The U.S. represents the largest country-level market, supported by high healthcare spending, broad adoption of PACS/RIS-enabled imaging workflows, strong reimbursement frameworks, and demand for advanced fixed and mobile digital radiography systems across hospitals, diagnostic imaging centers, emergency departments, and specialty clinics.

The region’s growth has also been supported by continued investments in hospital modernization, outpatient imaging expansion, emergency care capacity, and digital health integration. Digital X-ray systems in North America are increasingly being adopted for faster diagnosis, improved workflow efficiency, bedside imaging, dose management, and connected radiology operations. While the market is relatively mature, growth is expected to continue through replacement demand, adoption of mobile imaging, detector upgrades, AI-enabled workflow integration, and demand for high-throughput digital radiography systems.

Recent Developments in the Digital X-ray Market

• In February 2026, Fujifilm India announced the launch of the FDR Smart X Essential series, a compact digital radiography system designed to strengthen its X-ray portfolio in India. The system incorporates imaging technologies such as Irradiated Side Sampling, Dynamic Visualization, Virtual Grid, and optional AI-enabled image optimization and workflow tools.

• In July 2025, GE HealthCare announced commercial availability of Definium Pace Select ET, a floor-mounted digital X-ray system positioned for high-throughput, affordability-focused environments.

• In November 2025, Canon Inc. launched the Mobirex i9/Smart Edition, a high-end mobile X-ray system featuring workflow support tools such as a secondary tube-head monitor, 3D camera-based positioning, laser navigation, and dose optimization using CXDI-Elite BiAA technology.

• In February 2024, Koninklijke Philips N.V. received Canada FDA 510(k) clearance for its Radiography 7000 M, a mobile digital X-ray system. The system integrates a mobile base unit, wireless SkyPlate detectors, and Eleva WorkSpot software and is designed for diagnostic imaging across multiple anatomical regions in adult and pediatric patients, particularly in bedside settings where patients cannot be moved to fixed systems.

Demand – Drivers, Challenges, and Opportunities

Market Drivers:

Transition from Analog and Computed Radiography to Digital X-ray Systems: The transition from analog film-based and computed radiography workflows to digital X-ray systems remains a key driver for the market. Digital X-ray systems offer faster image acquisition, immediate image availability, improved image quality, electronic image storage, PACS/RIS connectivity, remote reporting, and better workflow efficiency. These advantages make them suitable for high-volume hospitals, emergency departments, diagnostic imaging centers, orthopedic clinics, and outpatient facilities. Digital systems also reduce dependence on film processing, chemical handling, cassette management, and manual archiving, which improves operational efficiency. As healthcare providers increasingly prioritize faster diagnosis, connected imaging workflows, and improved patient throughput, investment is shifting toward fully digital radiography platforms and retrofit digital upgrades.

Market Challenges:

Workforce Shortage and Skill Gap in Digital Radiography: Workforce shortage and skill gaps in radiography remain key challenges for the digital X-ray market. Digital radiography systems require trained radiographers, radiology technologists, IT support teams, and clinical users who can operate advanced imaging platforms, manage detector workflows, ensure appropriate positioning, apply dose optimization protocols, and maintain image quality standards. In many healthcare systems, shortages of radiology professionals and limited training capacity can restrict the effective adoption of advanced digital imaging systems. The challenge remains particularly relevant in rural facilities, emerging markets, public-sector hospitals, and smaller diagnostic centers where staffing levels and technical expertise may be limited. As digital X-ray platforms become more software-driven and connected to hospital IT infrastructure, the need for training, workflow standardization, and technical support is expected to increase.

Market Opportunities:

Next-Generation Detector Technologies Unlocking Advanced Diagnostic Capabilities in Digital X-Ray: Next-generation detector technologies present a major opportunity for the digital X-ray market. Advances in flat-panel detectors, wireless detectors, improved detector sensitivity, higher detective quantum efficiency, dose-efficient imaging, lightweight detector design, and AI-enabled image optimization are improving the performance and usability of Digital X-ray systems. These technologies support better image quality, lower radiation exposure, faster acquisition, and smoother workflows across fixed, mobile, and point-of-care imaging settings. Detector innovation is also strengthening the value of retrofit digital X-ray systems by allowing existing radiography rooms to be upgraded without complete replacement. As healthcare providers continue to seek better imaging performance, improved workflow efficiency, and lower radiation exposure, vendors offering advanced detector technologies and integrated software capabilities are expected to benefit.

Analyst’s Thoughts

According to Priyanshi Upadhyay, Research Analyst - BIS Research, “The digital X-ray market is expected to witness steady growth, supported by the continued transition from analog and computed radiography workflows toward fully digital radiography systems. Digital X-ray has become a core first-line imaging modality across hospitals, diagnostic imaging centers, orthopedic and specialty clinics, dental facilities, emergency departments, and decentralized care settings due to its ability to provide faster image acquisition, improved image quality, PACS/RIS connectivity, and more efficient clinical workflows. While fixed digital X-ray systems continue to dominate high-volume radiology departments, mobile and portable systems are gaining traction in bedside imaging, ICUs, emergency care, operating rooms, rural healthcare programs, and mobile diagnostic units. Going forward, market opportunities are expected to be shaped by detector innovation, dose optimization, workflow automation, AI-enabled image processing, retrofit upgrades, and healthcare infrastructure expansion across both mature and emerging markets.”

Focus on Portability, Technology, Product Type, Application, End User, and Region - Analysis and Forecast, 2026-2036

Digital X-ray is a diagnostic imaging technology that uses digital detectors, computed radiography plates, or integrated digital radiography systems to capture X-ray images electronically for applications such as chest imaging, orthopedic imaging, trauma assessment, dental imaging, emergency care, and general radiography. These systems support faster image acquisition, immediate image availability, improved image quality, electronic storage, PACS/RIS connectivity, and more efficient clinical decision-making compared to analog film-based X-ray systems.

To strengthen their market position, companies are focusing on advanced fixed and mobile digital X-ray systems, flat-panel detector innovation, retrofit digital upgrade solutions, improved image processing software, dose optimization tools, AI-enabled workflow support, PACS/RIS integration, compact system design, and service-friendly platforms. Many players are targeting hospitals, diagnostic imaging centers, orthopedic and specialty clinics, dental facilities, emergency departments, rural healthcare programs, and mobile diagnostic units where faster imaging, connected workflows, and reliable diagnostic performance remain key purchasing priorities. Product reliability, detector performance, local distribution, service support, and cost-effective upgrade pathways are also becoming important competitive strategies.

The following are the USPs of this report:

• Market regulations and key trends in the digital X-ray market

• Market dynamic analysis of the opportunities, trends, and challenges in the market

This report is valuable for digital X-ray system manufacturers, detector suppliers, medical imaging equipment companies, healthcare technology providers, distributors, hospitals, diagnostic imaging centers, orthopedic and specialty clinics, dental facilities, public-sector healthcare providers, mobile diagnostic service providers, service providers, and investors involved in radiography infrastructure, digital imaging modernization, and diagnostic imaging solutions.

The global analog X-ray market is projected to reach $686.5 million by 2036 from $602.1...