Published Year: 2021

Global Radiation Therapy in the Oncology Market: Focus on Radiation Therapy Systems, Product Regulat

The radiation therapy in oncology report highlights that the market was valued at $5,481.8...

Focus on Product Type, End User, Region, COVID-19 Impact, Competitive Landscape, and 22 Countries Data - Analysis and Forecast, 2021-2031

Delivery Time: 1-5 Working Days

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know MoreGlobal Electrocardiographs Overview

An electrocardiograph (ECG) machine records the electrical activity of your heart. The ECG machine detects the electrical signals that make the heart pump blood around body. Conventional devices and emerging devices are two types of electrocardiographs based on product type. Conventional devices can be categorized into resting ECG machines and stress ECG machines. Electrocardiographs are currently dominated by conventional devices. ECG monitoring systems have been created and widely used in the healthcare business for past decades, and as smart supporting technologies have emerged, they have evolved substantially. ECG monitoring devices are now often employed in hospitals, home care settings, outpatient ambulatory settings, and remote settings. Under conventional devices segment, resting ECG machines and stress ECG machines are included, whereas, under the emerging devices segment, implantable loop recorders, mobile cardiac telemetry, Holter monitors, and cardiac event monitors are included in the report.

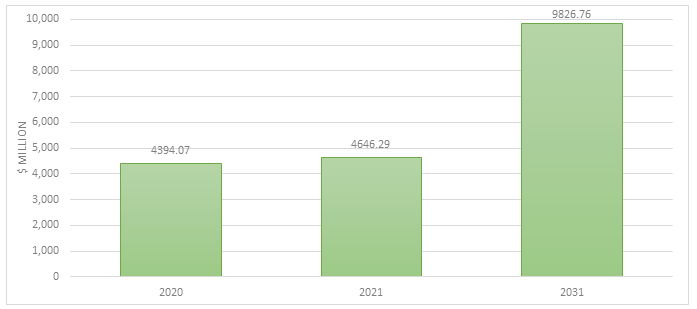

The global electrocardiographs market report highlights that the market was valued at $4,394.1 million in 2020 and is expected to reach $9,826.8 million by the end of 2031. The market is expected to grow at a CAGR of 7.8% during the forecast period 2021-2031.

Figure: Global Electrocardiographs Market, $Million, 2020-2031

Source: Expert Interviews and BIS Research Analysis

Global Electrocardiographs Market Dynamics

In the global electrocardiographs market, advancements have already occurred and are currently conquering the industry. There is significant potential for these developing and new technologies to promote the total growth of the market with the advent of advanced technologies that can be easily used in ambulatory and home care settings.

Some of the ongoing diseases are cardiovascular diseases, ischemic heart disease, strokes, hypertensive heart disease, congenital heart disease, rheumatic heart disease, cardiomyopathy, myocarditis, and aortic aneurysms. Many ailments are largely avoidable, treatable, and manageable with early detection and treatment. In addition, chronic illnesses are the leading cause of disability and death in the world. The prevalence of cardiovascular and related diseases propels market growth. The point-of-care (POC) market is growing exponentially, as POC devices assist in promptly ruling out suspected cardiac, vascular, and other disorders. Also, rising end-user preference for non-invasive diagnostic technologies over invasive technologies drives the market.

Accuracy, precision, timeliness, and authenticity are the four foundations of good laboratory services. In order to improve the analytical difficulties of sample processing, clinical biochemists typically overlook the need for timeliness. Clinicians, on the other hand, usually use timeliness as a benchmark for laboratory performance, which is expressed as the turnaround time (TAT). Short TATs help clinicians diagnose and treat patients as quickly as feasible, as well as discharge patients from emergency departments or hospital in-patient services.

One of the most common concerns with diagnosis is false and incomplete diagnoses. False-negative readings are the most typical issue with ECG. Other symptoms of any underlying heart didorder, such as chest pain, must be considered, and extra testing may be required. Delayed TAT and incomplete/false diagnosis results can have a negative impact on the market.

Modern cardiac imaging, which may include many modalities, is essential to correctly characterize the anatomy and physiology of pediatric and congenital heart disease. Newer imaging modalities, such as cardiac magnetic resonance imaging (CMR) and cardiac computed tomography angiography (CCTA), are increasingly being employed. When it comes to deciding on intervention or surgery for congenital or acquired heart disease, echocardiography and electrocardiography (ECG) are still the gold standards for non-invasive diagnosis. Due to the fast proliferation of medical imaging workstations, companies are working on improving technology and enabling public access to the software.

Company growth at workstations for medical imaging will be driven by rising demand for digital platforms, as well as new medical facilities and advancements in the healthcare business. The global electrocardiographs market is predicted to increase as a result of these improvements in multimodal diagnostic imaging for cardiovascular disorders.

Impact of COVID-19 on Global Electrocardiographs Market

Due to the increased cardiac complications caused by the COVID-19 virus, the overall market for diagnostic electrocardiographs, particularly conventional electrocardiographs, has a positive impact during this phase; however, implantable loop recorders have a minor impact when compared to conventional cardiac monitors due to the high cost of the equipment. Due to the requisite infrastructure not being in place to deal with the overwhelming number of cases in most nations, the impact was greater, particularly in the first months of February and March.

The electrocardiographs (ECG) machine is one of the key instruments for measuring the extent of cardiac involvement in COVID-19 patients and the effect of medications in this scenario due to its wide accessibility, low cost, and ability to be studied remotely.

Market Segmentation

Electrocardiographs Market (by Product Type)

Different technologies that are studied and analyzed under the global electrocardiographs market report include conventional devices and emerging devices.

Conventional devices generate the highest revenue in the electrocardiographs market, and emerging devices are expected to rise at a faster pace during the forecast period 2021-2031. This is mostly due to a rise in technologically advanced options and features like portability, constant monitoring, and cloud data sharing.

Global Electrocardiographs Market (Conventional Devices)

Different product types that are studied and analyzed under conventional devices segment include resting ECG machines and stress ECG machines.

In the global electrocardiographs market, resting ECG machines generate the most revenue, while stress ECG machines are projected to expand at the fastest rate during the forecast period 2021-2031. Stress lelectrocardiography offers the advantages of being widely available, having a minimal initial investment, and adding value by allowing assessment of heart structure as well as myocardial response to a potentially ischemic stimulus. All of these elements are projected to propel the market for stress ECG devices ahead.

Global Electrocardiographs Market (Emerging Devices)

Different product types that are studied and analyzed under emerging devices segment include implantable loop recorders, mobile cardiac telemetry, Holter monitors, and cardiac event monitors.

In the electrocardiographs market, implantable loop recorders generate the most revenue, while mobile cardiac telemetry is projected to expand at the fastest rate during the forecast period 2021-2031. Mobile cardiac telemetry provides the convenience of a compact and portable device as well as the ability to detect arrhythmia circumstances that other devices ignore due to its increased capacity to examine the morphology of the electrocardiographs. The key companies are benefited from these advantages over competing ECG devices.

Global Electrocardiographs Market (by Region)

The different regions covered under the electrocardiographs market report include North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

North America dominated the global electrocardiographs market in 2020 and is anticipated to uphold its dominance throughout the forecast period. The growth in the market is majorly driven by the increasing adoption of electrocardiographs after several cases of retained “foreign bodies” were reported across the globe. It is mandatory in several countries to implement electrocardiographs for patient’s safety during an operative procedure. Also, the ongoing trend for digital transformation is putting a significant impact on the market growth.

Key Market Players and Competition Synopsis

Some of the key players operating in the market include Abbott Laboratories, Biotricity, Inc., BIOTRONIK SE & Co. KG, Boston Scientific Corporation, CardioComm Solutions, Inc., Cardioline SpA, Fukuda Denshi Co., Ltd., General Electric Company, Hill-Rom Holdings, Inc., iRhythm Technologies, Inc., Koninklijke Philips N.V., Medtronic plc, Nihon Kohden Corporation, OSI Systems, Inc., and Zoll Medical Corporation (Asahi Kasei Corporation).

The electrocardiographs market has witnessed several strategic and technological developments in the past few years, (January 2016- June 2021) undertaken by the different market players to attain their respective market shares in this emerging domain. Some of the strategies covered in this segment are product offerings and upgradation, collaborative activities (partnerships, alliances, and business expansions), mergers and acquisitions, and regulatory and legal activities. The preferred strategy for companies has been collaborative activities.

Key Highlights

• According to global electrocardiographs market report, conventional devices segmentis dominating the market in 2020 when compared to emerging devices segment under the segmentation – by product type. Emerging devices are forecasted to uphold this position in the market and dominate by the end of the forecast period 2021-2031.

• In conventional devices segmentation, resting ECG machines are the market leader. During the forecast period 2021-2031, resting ECG is projected to lead the market. Stress ECG is projected to rise at a faster pace than resting ECG machines, with a CAGR of 6.1%.

• In emerging devices segmentation, resting implantable loop recorders is the market leader. By the end of the forecast period 2021-2031, mobile cardiac telemetry is projected to lead the market. Mobile cardiac telemetry is projected to rise at a faster pace than implantable loop recorders, with a CAGR of 11.7%.

• When the overall market contribution is considered, conventional devices segment accounts for 57.6% of the total market.

• The market holds the highest numbers in the North America region, followed by Asia-Pacific. The U.S. leads the table by contributing 33.2% of the total market in 2020. It is expected that by the end of the forecast period 2021-2031, the Asia-Pacific region will lead the market in the region-based segmentation.

Focus on Product Type, End User, Region, COVID-19 Impact, Competitive Landscape, and 22 Countries Data - Analysis and Forecast, 2021-2031

The electrocardiographs is expected to grow witnessing a CAGR of 7.8% during the forecast period from 2021 to 2031.

Trends that can influence the growth of the market include rise in demand for Holter monitors and development of insertable cardiac monitors.

The factors driving the growth of the market include growing demands for point-of-care diagnostic systems and rising end-user preference for non-invasive diagnostic technologies over invasive technologies

Hospitals and clinics, home care settings and ambulatory surgical systems and others are end-users of the electrocardiographs.

Abbott Laboratories, Biotricity, Inc., BIOTRONIK SE & Co. KG, Boston Scientific Corporation, CardioComm Solutions, Inc., Cardioline SpA, and Fukuda Denshi Co., Ltd., among others.

The radiation therapy in oncology report highlights that the market was valued at $5,481.8...

The global next-generation ultrasound systems market was valued at $8,246.8 million in 2020...

The Global Point-of-Care Imaging Devices Market was valued to be $8.66 billion in 2019 and is...

The global tissue imaging market was valued to be $14.42 billion in 2019 and is anticipated to...