Published Year: 2023

Next Generation Sequencing (NGS) Market - A Global and Regional Analysis: Focus on Offering, Company

The global NGS market was valued at $6.76 billion in 2022 and is expected to reach $28.47...

Focus on Offering, Technology, Application, and End User - Analysis and Forecast, 2024-2034

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Next-generation sequencing (NGS) has revolutionized cancer diagnostics by enabling the simultaneous analysis of multiple genes. This allows for precise tumor profiling, identification of actionable mutations, and customization of treatment plans through targeted therapies. NGS is widely used in liquid biopsies, which are non-invasive and help track cancer progression by analyzing circulating tumor DNA (ctDNA) in the bloodstream. Additionally, translational research in oncology relies heavily on NGS for studying tumor genetics. Researchers can identify genetic alterations that contribute to cancer progression and resistance to therapies. This has driven the development of new drugs and targeted therapies. Furthermore, NGS technology is applied in non-invasive prenatal testing (NIPT) to screen fetal DNA for chromosomal abnormalities such as Down syndrome. Moreover, NGS allows for rapid and accurate pathogen detection. Its ability to sequence entire genomes aids in genomic surveillance of infectious diseases, particularly in cases of drug-resistant pathogens.

The increasing prevalence of cancer, chronic diseases, and rare genetic disorders in Latin America has been driving the adoption of NGS technologies for personalized treatments, thereby fueling the growth of the Latin America NGS market. Precision medicine has been gaining traction as healthcare systems in countries such as Brazil and Mexico invest more in oncology and genomic testing. Programs that encourage collaboration between public research institutions and private companies are accelerating the adoption of NGS. More clinical labs are incorporating NGS-based diagnostics for cancer treatment, leveraging liquid biopsies and tumor profiling. This trend is set to expand as genomic data becomes more accessible and affordable. Academic partnerships and international collaborations are contributing to the growth of translational research in genomics, particularly in fields such as infectious disease research and population genomics.

Market Size and Growth

In 2024, the Latin America NGS market was valued at $268.04 million. It is projected to grow at a compound annual growth rate (CAGR) of 8.34%, reaching $597.20 million by 2034.

Key Figures in the Latin America NGS Market:

• Installed Base: The number of NGS instruments in use is expected to increase from 2,244 units in 2023 to 4,179 units by 2034, with the highest installed base in Brazil, followed by Mexico.

• NGS-Based Testing Volume Analysis: The NGS-based testing volume in Latin America is expected to increase from 111.2 thousand in 2023 to 405.3 thousand in 2034.

o By Indication: Based on the indication, oncology is expected to dominate the testing volume in the Latin America NGS market.

o By Country: Based on country, Brazil is expected to dominate the testing volume in the Latin America NGS market.

o By Sourcing Type: Based on sourcing type, the outsourced segment is expected to dominate the testing volume in the Latin America NGS market.

Market Dynamics

Drivers:

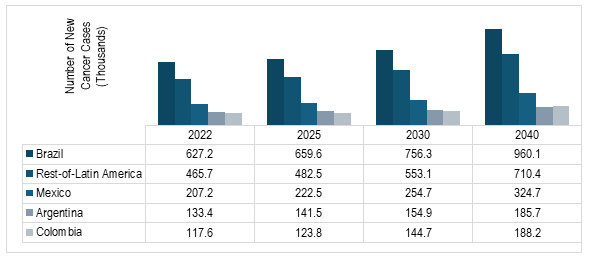

1. Rising Demand for NGS Driven by Growing Disease Burden: Rising demand of next-generation sequencing (NGS) is becoming a key driver of Latin America NGS market, leveraging its ability to provide precise genetic insights for cancer diagnosis and treatment, as well as its applications in infectious disease research. The increasing cancer burden and demand for personalized medicine are fueling the adoption of NGS in the region.

Figure: Incidence of Cancer in Key Countries of Latin America in 2022, 2025, 2030, and 2040

2. Expanding Localized Genomics Infrastructure and Partnerships: The Latin America NGS market is expanding due to initiatives such as the CABANA project, which has built regional genomic infrastructure and facilitated global collaborations. Partnerships with organizations such as MGI Tech, BGI Genomics, and Lifebit are enhancing the region's sequencing capabilities, advancing precision medicine, and promoting large-scale genomic research.

Restraints:

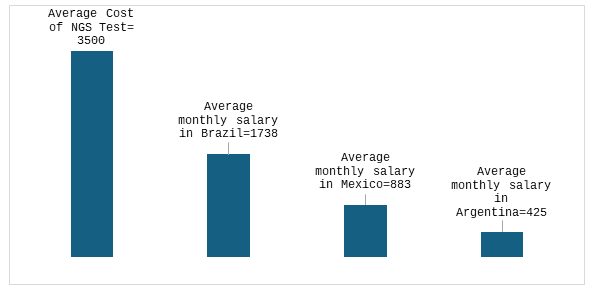

1. Cost-Effectiveness: The high cost of next-generation sequencing (NGS) testing remains a barrier to its widespread adoption in the region, subsequently hindering the growth of the Latin America NGS market, particularly in Brazil, Mexico, and Argentina, where average incomes are significantly lower. Despite global reductions in NGS costs, affordability challenges continue to hinder its integration into healthcare systems across the region.

Figure: Comparison between the Average Cost of NGS Test In Latin America and the Average Monthly Salary of People in Brazil, Mexico, and Argentina ($)

2. Lack of Funding and Reimbursement: Limited funding in public healthcare systems in the region hampers the development of essential infrastructure for genetic testing, forcing reliance on costly private labs, which consequently hinders the growth of the Latin American NGS market. The high cost of clinical exome sequencing and inadequate reimbursement rates, particularly in the public sector, further restrict access to NGS, limiting its adoption and sustainability across the region.

3. Lack of Education, Awareness, and Specialists: The lack of understanding of genomic technologies such as exome sequencing and whole genome sequencing among healthcare providers and patients, along with insufficient medical education and specialized professionals, is a major barrier to their broader adoption in Brazil. This knowledge gap, combined with the absence of clear guidelines and limited access to experts, restricts the effective implementation of these technologies.

Opportunities:

1. Establishing Diagnostic Centers: The Latin American NGS market has significant growth potential, driven by healthcare access disparities in Brazil, with specialized resources concentrated in certain regions. Expanding NGS capabilities and integrating technologies into initiatives such as 'Telessaude' and 'Hello Genetics' can enhance diagnostic support, improving rare disease care in underserved areas across LATAM.

2. Expanding Genomic Data for Advanced NGS Solutions: The limited availability of large-scale genetic data in Latin America hampers the interpretation of exome and whole genome sequencing results, creating an opportunity to build comprehensive regional genomic databases. Expanding these efforts will improve variant classification, enhance genetic research, and address gaps in understanding pathogenic variants specific to the diverse regional population, and create a growth opportunity for the Latin America NGS market.

Key Trends:

1. Growing Adoption of Personalized Medicine: The Latin America NGS market is growing rapidly due to its expanding role in oncology and infectious disease research, driven by the rising demand for precision medicine and its critical applications in cancer mutation detection and virological studies such as COVID-19 and HBV.

2. Increasing Local Production and Infrastructure: Countries in Latin America are investing in local NGS infrastructure by establishing genomics centers and bioinformatics training programs, such as the CABANA model in Mexico, to reduce reliance on international services and enhance regional genomic research capabilities.

3. Expansion of Genomic Data Accessibility: Efforts to increase the accessibility of genomic data are growing, with partnerships such as Lifebit, Omica.bio, and gen-t in Brazil and Mexico enhancing local data representation in global datasets to support more inclusive and accurate population health research.

Segmentation

Segmentation 1: By Offering

• Instruments: This segment includes integrated workflow instruments, sequencing instruments, and library preparation instruments.

• Kits and Consumables: This segment includes library preparation kits, target enrichment kits, sequencing kits, and multi-use kits.

• Software

• Services

Based on offering, the services segment is expected to dominate the Latin America NGS market.

Segmentation 2: By Technology

• Ion Torrent Semiconductor Sequencing

• Reversible Terminator Sequencing (SBS)

• Single Molecule Real Time Sequencing

• Nanopore Sequencing Technologies

• Other Technologies: It includes SOLiD sequencing, 10x Genomics' Chromium Technology, etc.

Based on technology, the reversible terminator sequencing (SBS) segment is expected to dominate the Latin America NGS market.

Segmentation 3: By Application

• Clinical: It includes oncology, neurological diseases testing, reproductive health testing, rare disease diagnostics, infectious disease testing, and others.

• Translational Research: It includes hematologic malignancies and solid tumors.

Based on application, the clinical segment is expected to dominate the Latin America NGS market.

Segmentation 4: By End User

• Hospitals and Clinics

• Academic and Research Institutes

• Pharmaceutical and Biotechnology Companies

• Government Labs

• Other End Users

Based on end user, the academic and research institutes segment is expected to dominate the Latin America NGS market.

Competitive Landscape

• Illumina dominated the Latin America NGS market, driven by its extensive portfolio of sequencing platforms such as the NovaSeq and MiSeq systems. Its strong presence in both clinical applications and research fields makes it the top player, benefiting from its leadership in high-throughput sequencing and a broad range of consumables and sequencing services.

• Thermo Fisher is also a key player in the Latin America NGS market, primarily through its Ion Torrent sequencing platforms and robust offerings in NGS reagents, kits, and library preparation solutions. Its focus on both clinical diagnostics and biotechnology research allows it to cater to diverse sectors, including healthcare and agriculture, making it a strong competitor to Illumina.

• Known for its long-read sequencing technology, Pacific Biosciences holds a niche position in the Latin American market. Its HiFi sequencing is particularly useful for de novo genome assembly, making it valuable for genomic research and complex genetic studies where long-read accuracy is critical, though its market share remains small in the Latin America NGS Market.

• Oxford Nanopore offers unique portable sequencing platforms, such as MinION, enabling real-time DNA/RNA sequencing. Its competitive edge lies in its scalability and ability to sequence in real-world settings, making it attractive for research. Despite its smaller market share, its portability and low-cost sequencing options position it for future growth in the Latin America NGS market.

Recent Developments

• In July 2024, Danaher launched two CLIA and CAP-certified labs to accelerate the development of CDx and CoDx, integrating diagnostic technologies, including NGS, to streamline precision medicine for faster drug development.

• In June 2024, MGI Tech Co., Ltd. has partnered with SeqOne to create end-to-end genomic analysis solutions using next-generation sequencing technologies. This collaboration aims to advance NGS research and diagnostics, improving global healthcare outcomes.

• In May 2024, QIAGEN and Myriad Genetics developed a global HRD test using QIAGEN’s QIAseq xHYB technology and Myriad’s MyChoice CDx biomarkers. The test, designed for research and companion diagnostics in oncology, expanded testing capabilities and clinical applications worldwide, building on their recent master agreement.

• In April 2024, Beckman Coulter Life Sciences partners with Watchmaker Genomics to deliver automated NGS library preparation solutions, enhancing lab efficiency and ensuring consistent, high-quality results for clinical and translational applications.

• In April 2024, Oxford Nanopore Technologies launched the Compatible Products Programme to enhance its genomic sequencing ecosystem by approving third-party products for seamless integration. The initiative aimed to improve user experience and foster collaboration within the genomics community by ensuring high compatibility and performance across sequencing workflows.

Conclusion

The Latin America NGS market is poised for significant growth, driven by increasing demand for personalized medicine, advancements in genomic infrastructure, and expanding research collaborations. Despite challenges such as high costs, limited funding, and a lack of specialized professionals, opportunities in areas such as expanding genomic data, establishing diagnostic centers, and integrating NGS into healthcare systems offer a promising future. As local genomic capabilities grow and accessibility improves, the Latin America NGS market is expected to become a key player in global healthcare innovation.

Focus on Offering, Technology, Application, and End User - Analysis and Forecast, 2024-2034

The Latin America next-generation sequencing (NGS) market refers to the comprehensive application of NGS technologies for clinical diagnostics, translational research across Latin American countries. This market includes instruments, such as sequencers, and consumables, such as reagents, kits, software, and services.

The key trends in the Latin America NGS market include the growing adoption of personalized medicine, particularly in oncology and infectious disease research, driven by rising demand for precision treatments. Additionally, there is an increasing focus on expanding local NGS infrastructure, with countries investing in genomic centers and bioinformatics training programs, alongside efforts to enhance the accessibility of genomic data for more inclusive population health research.

The key drivers of the Latin America NGS market include the rising demand for precision medicine due to the increasing prevalence of cancer, chronic diseases, and rare genetic disorders. Additionally, expanding localized genomics infrastructure, global partnerships, and collaborative initiatives are enhancing NGS capabilities, fostering growth in the region's market.

The Latin America NGS market was valued at $250.3 million in 2023 and is anticipated to reach $597.20 million by the end of 2034, at a CAGR of 8.34% during the forecast period 2024-2034.

The global NGS market was valued at $6.76 billion in 2022 and is expected to reach $28.47...