Published Year: 2026

Hematologic Malignancies Testing Market - A Global and Regional Analysis: Focus on Product, Platform

The global hematologic malignancies testing market is projected to reach $18,404.5 million by...

Focus on Ecosystem, Application, and Region - Analysis and Forecast, 2024-2034

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Precision medicine utilizes an individual's distinct clinical, molecular, and lifestyle data to inform the diagnosis, treatment, and prevention of cancer, inherited diseases, and other complex conditions. Precision medicine represents a transformative shift in healthcare, moving away from the traditional one-size-fits-all approach to a more tailored and targeted therapeutic strategy. By leveraging advancements in genomics, molecular diagnostics, and data analytics, precision medicine enables healthcare providers to craft personalized treatment plans based on an individual's genetic, environmental, and lifestyle factors. This approach not only promises to enhance the effectiveness of treatments but also reduces unnecessary trial-and-error, leading to better patient outcomes and reduced healthcare costs. As the field continues to evolve, large-scale population studies and cutting-edge technologies are paving the way for more accurate disease predictions, early diagnoses, and optimized therapeutic interventions.

Market Introduction

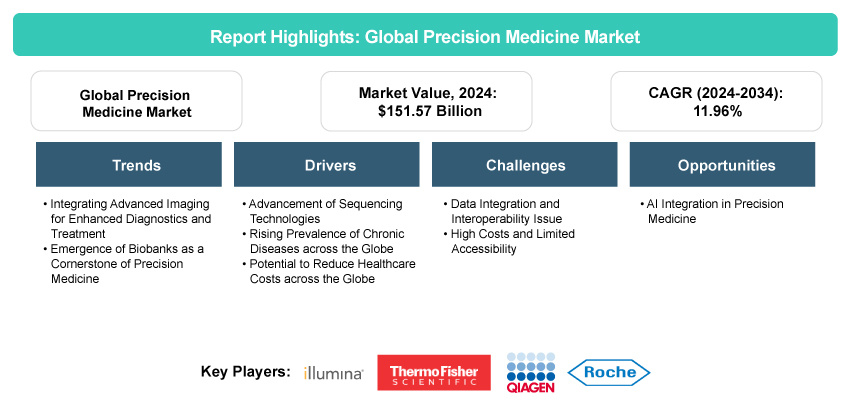

The global precision medicine market is expected to witness substantial growth, projected to reach $469.16 billion by 2034. The growing adoption of precision medicine has been fueled by the expansion of multi-omics research, which combines genomics, proteomics, metabolomics, and other molecular data to create a more comprehensive understanding of health and disease. This innovative approach holds significant potential in various therapeutic areas, including oncology, pharmacogenomics, and inherited diseases.

The precision medicine market has been experiencing rapid growth driven by advancements in sequencing technologies, decreasing sequencing costs, shifting trends toward personalized health, etc. Moreover, advancements in gene sequencing and editing, particularly with CRISPR and next-generation sequencing (NGS), are driving precision medicine forward by enabling more targeted and personalized treatments. These technologies allow for more effective cancer therapies, such as CAR-T cell therapy, which harnesses the patient’s immune system to fight cancer. As these technologies evolve, they are expected to further enhance the accuracy of diagnoses, facilitate early interventions, and optimize therapeutic outcomes, contributing to the growing demand for precision medicine solutions in oncology and genetic disorders.

In addition, spatiotemporal omics technologies and proteomics have emerged as critical tools for understanding complex diseases at a molecular level. By analyzing variations in genomic, proteomic, and metabolomic profiles, these technologies provide deeper insights into the heterogeneity of diseases such as cancer, paving the way for treatments tailored to an individual’s unique disease characteristics. The integration of artificial intelligence (AI), big data analytics, and IoT technologies has also been transforming the precision medicine landscape by enabling real-time monitoring and analysis of patient data. These advancements improve the ability to predict disease progression, personalize treatments, and enhance patient outcomes. However, they also introduce challenges, such as data privacy concerns and the need for advanced computational tools, which could impact the overall adoption and scalability of precision medicine solutions in the market. As these technologies mature, they will drive further innovation in the precision medicine space, leading to more efficient and effective healthcare models.

Industrial Impact

Precision medicine is reshaping the healthcare industry by enabling personalized treatments that significantly improve patient outcomes. For instance, the use of genetic profiling in oncology has led to the development of targeted therapies. In addition to improving individual patient care, precision medicine is driving innovation across the healthcare ecosystem, particularly in drug discovery and clinical trials. The pharmaceutical industry is leveraging genomics to discover new drug targets, as seen in the development of the breakthrough drug Kymriah, a CAR-T therapy for leukemia, which was developed through the identification of genetic markers specific to the disease. Clinical trials are also becoming more targeted, with companies such as Novartis and Pfizer using genomic data to stratify patient populations and improve trial efficiency. Moreover, the integration of precision medicine into population health management is evident in initiatives such as Geisinger Health System’s MyCode Community Health Initiative, which offers genomic sequencing to patients to improve preventive care and early disease detection. This growing application of precision medicine has not only improved individual treatment outcomes but has also helped to optimize healthcare delivery systems, reduce costs, and accelerate the development of new therapies.

Market Segmentation

Segmentation 1: by Ecosystem

• Applied Science

o Genomics

o Pharmacogenomics

o Other Applied Science

• Precision Diagnostics

o Molecular Diagnostics

o Medical Imaging

• Digital Health and Information Technology

o Clinical Decision Support Systems (CDSS)

o Big Data Analytics

o IT Infrastructure

o Genomics Informatics

o In-Silico Informatics

o Mobile Health

• Precision Therapeutics

o Clinical Trials

o Cell Therapy

o Drug Discovery and Research

o Gene Therapy

In the global precision medicine market, as of 2023, the precision therapeutics segment holds the largest share at 33.6%. Precision therapeutics has gained significant traction in oncology, rare diseases, and chronic conditions, where traditional treatments often fall short due to its ability to offer highly personalized treatment options that are tailored to an individual’s genetic, molecular, and environmental profiles. Moreover, the growing use of biomarker-driven patient selection in clinical trials further enhances treatment efficacy, as it helps identify the right patients for the right therapies, reducing trial failure rates and accelerating the path to successful treatments. On the other hand, the digital health and IT infrastructure segment is projected to grow at the highest (CAGR) of 14.4% from 2024 to 2034 Digital health is becoming an increasingly important part of precision medicine due to its ability to enhance patient care through the collection, transmission, and integration of vast amounts of personalized health data. Moreover, it allows for the real-time tracking of a patient’s health, enabling quick modifications to treatment plans as needed. This continuous feedback loop ensures that therapies remain optimal throughout the course of treatment, helping to improve patient outcomes.

Segmentation 2: by Application

• Oncology

• Infectious Diseases

• Neurology/Psychiatry

• Life Style and Endocrinology

• Cardiology

• Gastroenterology

• Others

Based on application, the global precision medicine market was led by the oncology segment, which held a 52.8% share in 2023. The global increase in cancer burden has been one of the major factors driving the demand for precision medicine. For instance, according to the World Health Organization, more than 35 million new cancer cases are expected by 2050, marking a 77% increase from the estimated 20 million cases in 2022. Moreover, technological advancements, especially in genomic sequencing and molecular diagnostics, have transformed cancer treatment. Next-generation sequencing (NGS) identifies genetic alterations and biomarkers, enabling personalized therapies tailored to a patient’s tumor characteristics. In addition, the growing integration of genomic data into immunotherapy, where treatments are increasingly guided by specific genetic or molecular markers that predict how patients will respond to immune-based treatments, is driving the segment growth.

Segmentation 3: by Region

• North America

o U.S.

o Canada

• Europe

o Germany

o U.K.

o France

o Italy

o Spain

o Rest-of-Europe

• Asia-Pacific

o Japan

o India

o China

o Australia

o South Korea

o Rest-of-Asia-Pacific

• Latin America

o Brazil

o Mexico

o Rest-of-Latin America

• Middle East and Africa

o K.S.A.

o South Africa

o Rest-of-Middle East and Africa

The precision medicine market in the North America region is expected to witness a significant growth rate of 10.25% during the forecast period, marked by the increasing prevalence of genetic disorders and the growing demand for personalized medicine and robust government initiatives. Also, the strong infrastructure for medical research and clinical trials and increasing investment by biopharmaceutical companies in precision medicine are driving the market. However, the Asia-Pacific region is expected to witness the fastest growth rate of 14.67% during the forecast period 2024-2034 Various factors are expected to contribute to this growth, including increasing disposable income, rising prevalence of chronic disease, increasing demand for personalized health, and increasing focus on the development of cost-effective, advanced diagnostic tools.

Recent Developments in the Precision Medicine Market

• In January 2025, OMNY Health and Scipher Medicine entered into a partnership to advance precision medicine in autoimmune diseases. Under this partnership, Scipher Medicine will combine its clinico-transcriptomic data with OMNY Health’s vast electronic medical record (EMR) network to enhance treatment options and outcomes for millions of patients worldwide.

• In November 2024, 23andMe Holding Co. and Mirador Therapeutics entered into a strategic research collaboration. Through this partnership, Mirador will utilize a curated set of de-identified genetic and phenotypic data from the 23andMe research database, combined with its proprietary Mirador360 development engine, to advance target validation and precision medicine initiatives.

• In May 2024, the Precision Health Alliance, a new initiative co-founded by the Duke Clinical Research Institute (DCRI), Beam Therapeutics, CRISPR Therapeutics, Intellia Therapeutics, and Verve Therapeutics, was launched to drive innovation in precision health and medicine. The alliance aims to address challenges in personalized healthcare by focusing on genetic factors and will serve as a collaborative platform for research in gene editing. It seeks to explore patient preferences, ethical issues, and regulatory challenges while influencing future policies and payment models to expand patient access and accelerate advancements in the field.

• In May 2024, Rymedi and Precision Genetics announced a strategic partnership to enhance health outcomes and efficiencies through precision medicine. This collaboration will integrate Precision Genetics’ PrecisionOp, a personalized solution to minimize adverse drug reactions and reduce opioid use after surgery, with Rymedi’s blockchain-enabled clinical trial and registry platform.

Demand –Drivers, Challenges, and Opportunities

Market Demand Drivers:

Advancement of Sequencing Technologies: The advancement of DNA sequencing technologies has been a key driver in the rapid growth of the precision medicine market, bringing transformative changes to healthcare. From the early days of Sanger sequencing to the innovations in next-generation sequencing (NGS) and long-read technologies, sequencing methods have become more accurate, personalized, and efficient. The dramatic reduction in sequencing costs, from over $100 million in 2001 to just $100-$200 in 2023, has made genomic testing more accessible and integrated into routine clinical care. This affordability is crucial in expanding precision medicine's reach to a broader patient base. Advances in sequencing accuracy, especially with long-read technologies, have enhanced the identification of rare genetic variants and allowed for more precise diagnoses and treatments, particularly in complex conditions such as cancer, cardiovascular diseases, and genetic disorders. Additionally, improvements in sequencing speed and throughput enable faster, large-scale genetic studies, while multi-omics integration provides a more holistic approach to personalized treatment. These developments are accelerating the demand for precision medicine, making genomic testing a core component of modern healthcare.

Some of the other driving factors include:

• Rising Prevalence of Chronic Diseases

• Potential to Reduce Healthcare Costs

• Potential to Reduce Adverse Drug Reaction

Market Challenges:

Data Integration and Interoperability Issues: A key challenge in precision medicine is integrating diverse data sources to create a comprehensive view of a patient’s health. Healthcare providers must combine electronic health records (EHRs), genomic databases, imaging data, patient-reported outcomes (PROs), and other relevant datasets, but these are often stored in siloed systems that lack seamless communication. Data silos remain a significant barrier, with platforms used for clinical, genomic, and imaging data often unable to interact effectively. A 2023 HealthIT.gov survey revealed that 40% of healthcare organizations struggle to fully integrate EHRs with external data sources, such as genomic and imaging information. This fragmentation hinders personalized decision-making, as healthcare providers cannot easily access or correlate the necessary data. The complexity of data integration is further compounded by the need for specialized tools to analyze genomic data, natural language processing (NLP) to structure clinical notes and advanced imaging software for aligning data. Additionally, many healthcare systems overlook the integration of PROs, which are critical for understanding a patient's lifestyle and preferences, with over 35% of providers not yet incorporating them into clinical workflows, limiting the ability to offer truly personalized care.

Some of the other factors challenging the market growth include:

• High Costs and Limited Accessibility

• Limited Reimbursement and Insurance Coverage

Market Opportunities:

AI Integration in Precision Medicine: The integration of AI into precision medicine (PM) offers a significant opportunity for market growth by enhancing various aspects of healthcare, including risk assessment, treatment optimization, and patient outcomes. AI's ability to process complex biological data, including genetic profiles and patient histories, overcomes traditional barriers to robust risk assessment protocols, enabling more accurate predictions and personalized care. For instance, AI has revolutionized disease diagnosis by identifying patterns that may be missed by human clinicians, particularly in fields like dermatology and Alzheimer’s disease. It also improves patient monitoring by leveraging data from wearables and IoT sensors to provide real-time insights, reducing diagnostic errors and enabling timely interventions. Furthermore, AI accelerates drug discovery by analyzing large datasets to identify new therapeutic targets, particularly in cancer, ultimately enhancing the precision and effectiveness of treatments. Integrating AI into clinical decision-making improves diagnostic accuracy and supports clinicians with evidence-based insights, ensuring more informed decisions.

Some of the other factors creating an opportunity for market growth include:

• Increasing Collaborations and Partnerships

Market Trends:

Integrating Advanced Imaging for Enhanced Diagnostics and Treatment

The trend in precision medicine is shifting toward delivering high-quality, personalized care through the integration of advanced imaging technologies, genomics, and AI-driven solutions. This approach enhances the accuracy and effectiveness of diagnoses and treatment plans by offering a multi-dimensional understanding of diseases such as cancer. Radiomics and AI are transforming clinical decision-making by providing actionable insights from medical images, enabling a deeper understanding of tumor heterogeneity and patient-specific factors. Additionally, cloud-based platforms and biophysical modeling are allowing for real-time analysis and personalized treatment simulations, further improving clinical outcomes. As these technologies evolve, the demand for high-quality, tailored therapies is expected to rise, offering better results than traditional methods.

Some of the other emerging trends in the market include:

• Emergence of Biobanks as a Cornerstone of Precision Medicine

Analyst’s Thoughts

According to Akash Mhaskar, Principal Analyst – BIS Research, “The precision medicine market is growing rapidly, fueled by advancements in DNA sequencing technologies that make genomic testing more accessible. Despite challenges in data integration, AI offers significant opportunities by enhancing disease diagnosis, risk assessment, and treatment optimization. As AI and sequencing technologies evolve, precision medicine is set to transform patient care, especially in oncology and genetic disorders.”

Focus on Ecosystem, Application, and Region - Analysis and Forecast, 2024-2034

Precision medicine is an innovative healthcare approach that integrates applied sciences such as genomics, molecular biology, and bioinformatics to tailor treatments based on an individual’s genetic makeup, environment, and lifestyle. It relies on precision diagnostics, including advanced genetic sequencing, biomarker analysis, and AI-driven imaging, to enable early disease detection and targeted interventions. Digital health and information technology, such as electronic health records (EHRs), wearable devices, and AI-powered analytics, play a crucial role in collecting, analyzing, and personalizing patient data for more effective decision-making. The field also encompasses precision therapeutics, including gene therapies, biologics, and targeted drugs designed to address specific molecular mechanisms of diseases, ensuring higher efficacy with minimal side effects. By integrating these components, precision medicine is transforming disease prevention, diagnosis, and treatment, making healthcare more predictive, personalized, and proactive.

To strengthen their position in the rapidly evolving precision medicine industry, market players are adopting strategic collaborations, AI-driven innovations, and personalized drug development. Companies are increasingly forming partnerships with biotech firms, research institutions, and digital health startups to accelerate the discovery and commercialization of targeted therapies. Artificial intelligence (AI) and machine learning are being leveraged for advanced genomic data analysis, drug discovery, and predictive analytics to enhance patient outcomes. Additionally, pharmaceutical and biotech firms are expanding their portfolios with precision therapeutics, including gene therapies, mRNA-based treatments, and monoclonal antibodies. Investments in companion diagnostics and digital health platforms, such as remote patient monitoring and real-world evidence (RWE) analytics, are enabling more accurate and scalable treatment approaches. Furthermore, regulatory engagement and adaptive clinical trials are streamlining the approval process for new personalized medicines, ensuring a competitive edge in this dynamic market.

The following are the USPs of this report:

• Market regulations and key trends in the precision medicine market

• Dynamic analysis of the opportunities, trends, and challenges in the market

This report is essential for healthcare providers, pharmaceutical and biotech companies, diagnostic firms, researchers, and investors. It offers insights into precision diagnostics, targeted therapies, and digital health solutions, helping clinicians and scientists stay updated on advancements. Pharma and biotech firms can leverage it for R&D and drug development, while investors and analysts can use it to assess market trends and growth opportunities for strategic decision-making.

The global hematologic malignancies testing market is projected to reach $18,404.5 million by...

The global liquid biopsy market was valued at $4,072.6 million in 2023 and is expected to...

The global precision medicine software market was valued at $1,824.9 million in 2023 and is...

The global NIPT market was valued at $3,350.4 million in 2023 and is expected to reach...