Published Year: 2026

Computed Tomography Market - A Global and Regional Analysis: Type, Technology, End User, and Regiona

The global computed tomography market is projected to reach $13,197.1 million by 2036 from...

Focus on Application, End User, and Region - Analysis and Forecast, 2026-2036

Delivery Time: 1 Working Day

Get ISO Certified Research, Customization, Data Extraction, and Value-Added Services with All BIS Research Reports

BIS Research provides a comprehensive report library with unlimited access to data, insights, and market intelligence through Subscription.

Get Subscription Know More

Introduction of the Computed Radiography Market

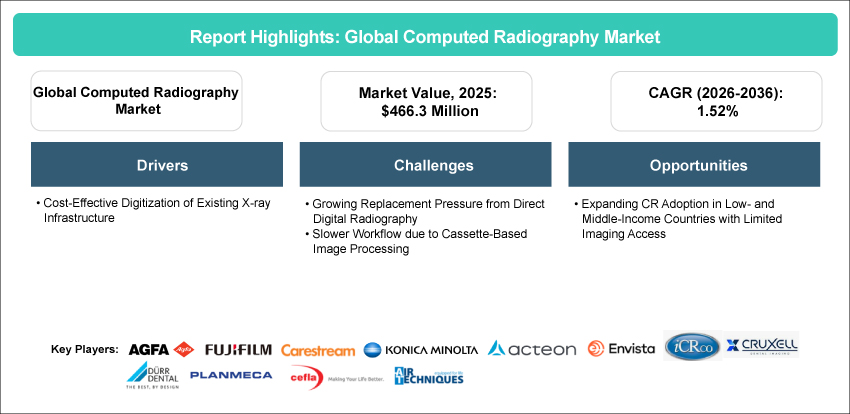

The global computed radiography market, initially valued at $466.3 million in 2025, is projected to grow substantially, reaching $548.9 million by 2036, with a remarkable compound annual growth rate (CAGR) of 1.52% from 2026 to 2036.

The global computed radiography market is experiencing moderate growth, driven by the continued need for affordable digital conversion of conventional X-ray workflows and the broader shift toward digital diagnostics. Computed radiography (CR) uses photostimulable phosphor imaging plates, cassettes, CR readers/scanners, and image processing software to convert X-ray exposures into digital images. The technology remains relevant for hospitals, diagnostic imaging centers, dental clinics, orthopedic practices, rural facilities, and public-sector healthcare providers that require digital image storage, retrieval, sharing, and reporting capabilities without replacing existing X-ray infrastructure. As a bridge between film-based radiography and direct digital radiography, computed radiography enables healthcare facilities to convert conventional X-ray workflows into digital imaging environments while reducing film processing, chemical handling, physical archiving, and manual image management. Its compatibility with PACS/RIS platforms and ability to extend the usability of installed X-ray rooms continue to make it a practical option for cost-sensitive and infrastructure-constrained healthcare settings pursuing phased digital diagnostics adoption.

Technological advancements are reshaping the computed radiography landscape, with improvements in compact CR readers, reusable imaging plates, image processing software, dose optimization, mini-PACS functionality, and workflow connectivity playing an important role in sustaining market relevance. Despite the market’s growth prospects, challenges such as the increasing preference for direct digital radiography, slower image availability, cassette-based workflow limitations, and replacement pressure in high-volume hospitals remain significant. However, ongoing demand from smaller healthcare facilities, mobile diagnostic units, dental and orthopedic clinics, and emerging markets is expected to support continued adoption of computed radiography as an affordable and phased pathway toward digital imaging modernization.

Market Introduction

The global computed radiography market has undergone a gradual transition, shaped by the need for affordable digital conversion of conventional X-ray imaging workflows. Computed radiography continues to serve as a bridge technology for healthcare facilities that require digital image capture, storage, sharing, and reporting capabilities without replacing their existing X-ray infrastructure. Companies are increasingly focusing on compact CR readers, reusable photostimulable phosphor imaging plates, cassette-based systems, image processing software, and PACS-compatible workflow solutions to support cost-effective digitization. Noteworthy developments, such as compact tabletop readers, mini-PACS functionality, improved image processing, dose optimization, and mobile-compatible CR configurations, underscore the industry’s focus on extending the practical value of CR in lower-volume, space-constrained, and cost-sensitive healthcare settings. As direct digital radiography adoption continues to increase in high-throughput hospitals, computed radiography is expected to remain relevant in selected markets, particularly among smaller hospitals, diagnostic centers, dental clinics, orthopedic practices, rural facilities, and public-sector providers seeking phased digital modernization.

Industrial Impact

The global computed radiography market has witnessed steady adoption, driven by the continued demand for affordable digital imaging solutions and the need to modernize conventional X-ray workflows without full system replacement. Key players such as Carestream Health, Agfa-Gevaert Group, FUJIFILM Corporation, Konica Minolta, Inc., and other regional providers play a central role in supporting cost-effective radiography digitization through CR readers, reusable imaging plates, cassettes, image processing software, and PACS-compatible workflow solutions. These offerings are crucial across routine applications such as chest imaging, orthopedic imaging, dental radiography, trauma assessment, and general radiography, enabling healthcare facilities to reduce film dependence, improve image storage and retrieval, and support more efficient reporting workflows. By extending the usability of existing X-ray infrastructure, reducing the burden of chemical processing and physical archiving, and enabling digital image sharing, computed radiography continues to contribute to more accessible diagnostic imaging. The market’s impact is most visible in smaller hospitals, diagnostic imaging centers, rural facilities, public-sector providers, and cost-sensitive markets, where CR remains an important bridge between analog radiography and full direct digital radiography adoption.

Market Segmentation:

Segmentation 1: By Application

• Orthopedic Imaging

• Chest Imaging

• Dental Imaging

• Others

Chest Imaging Segment to Dominate the Computed Radiography Market (by Application)

In terms of application, the chest imaging segment is expected to lead the computed radiography market, accounting for a significant share due to the high volume of chest X-ray examinations performed across routine diagnostic, emergency, inpatient, and outpatient settings. Chest imaging remains widely used for the assessment and monitoring of respiratory infections, pneumonia, tuberculosis, chronic obstructive pulmonary disease, trauma, lung abnormalities, and cardiac-related conditions. Moreover, as chest X-rays are frequently repeated for diagnosis, follow-up, and pre-operative evaluation, healthcare facilities continue to rely on CR systems where affordability, existing X-ray infrastructure utilization, and workflow digitization are key priorities.

Segmentation 2: By End User

• Hospitals

• Orthopedic and Specialty Clinics

• Diagnostic Imaging Centers

• Other End Users

Hospitals to Dominate the Computed Radiography Market (by End User)

In terms of end user, the hospitals segment is anticipated to lead the computed radiography market, accounting for a significant share due to the high volume of routine and urgent diagnostic imaging procedures performed across hospital departments. Hospitals use computed radiography across emergency care, inpatient wards, outpatient departments, orthopedics, chest imaging, trauma assessment, and surgical evaluation, where cost-effective digital image acquisition and reliable workflow support remain important. Computed radiography enables hospitals to digitize existing X-ray rooms, improve PACS-compatible image storage and retrieval, reduce dependence on film processing, and support more efficient reporting workflows without requiring immediate full-system replacement. The segment is further supported by the presence of trained radiology staff, established imaging infrastructure, and recurring demand for X-ray examinations across multiple clinical departments.

Segmentation 3: By Region

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Rest-of-Europe

• Asia-Pacific

o China

o Japan

o India

o Australia

o South Korea

o Rest-of-Asia-Pacific

• Latin America

o Brazil

o Mexico

o Rest-of-Latin America

• Middle East and Africa

o K.S.A.

o U.A.E.

o South Africa

o Rest-of-Middle East and Africa

Asia-Pacific to Dominate the Computed Radiography Market (by Region)

In terms of region, Asia-Pacific is expected to lead the computed radiography market, accounting for a significant share due to the continued demand for affordable radiography digitization across cost-sensitive and infrastructure-developing healthcare systems. The region includes a large base of hospitals, diagnostic imaging centers, dental clinics, orthopedic practices, rural healthcare facilities, and public-sector providers that continue to rely on existing X-ray infrastructure. Computed radiography offers these facilities a practical route to transition from film-based workflows to digital image capture, storage, sharing, and reporting without the higher upfront investment required for direct digital radiography systems. The segment is further supported by hospital infrastructure expansion, rural diagnostic access initiatives, growing imaging procedure volumes, and the need to improve PACS-compatible workflow efficiency. As healthcare providers across emerging Asia-Pacific markets continue to prioritize phased modernization, affordability, compact deployment, and reduced dependence on film processing, computed radiography is expected to maintain a strong position in the regional market.

Recent Developments in the Computed Radiography Market

• In September 2025, Carestream introduced Image Suite V4 Software MR 11 for CR and DR imaging systems, adding AI-enabled companion images such as bone suppression, pneumothorax visualization, and enhanced tube/line visualization to improve diagnostic confidence. The update also includes SmartGrid Technology, cross-system detector sharing, and customizable image looks to enhance workflow and patient experience.

• In May 2024, Carestream Health launched Image Suite MR 10 Software for CR and DR imaging systems in May 2024, designed to improve radiographer productivity, imaging efficiency, and user experience. The update adds features such as Focus HD detector support, DR Total Quality Testing, CR mammography enhancements, and optional DR long-length imaging auto-stitching.

Demand – Drivers, Challenges, and Opportunities

Market Drivers:

Cost-Effective Digitization of Existing X-ray Infrastructure: The need for affordable digitization of existing X-ray infrastructure remains a key factor driving demand for computed radiography systems. Many healthcare facilities, particularly in cost-sensitive markets across Asia-Pacific, Latin America, the Middle East and Africa, and selected European regions, continue to operate functional analog or film-based X-ray systems. For these facilities, the priority is not immediate replacement with direct digital radiography, but the gradual reduction of film dependency, chemical processing, darkroom operations, and physical image storage. Computed radiography addresses this need by enabling digital image capture through reusable photostimulable phosphor plates, cassettes, CR readers, and image processing software while allowing providers to continue using existing X-ray rooms. This makes CR a practical solution for phased modernization, particularly among smaller hospitals, diagnostic centers, rural facilities, and public-sector providers with limited capital budgets. By supporting PACS-compatible image storage, easier sharing, improved reporting workflows, and lower recurring consumable costs compared with conventional film radiography, computed radiography provides a manageable route toward digital imaging adoption.

Market Challenges:

Growing Replacement Pressure from Direct Digital Radiography: The increasing replacement of computed radiography by direct digital radiography remains a key restraint for the computed radiography market. While CR continues to support affordable digitization of existing X-ray infrastructure, its cassette-based workflow requires additional steps such as plate handling, reader-based scanning, image processing, and periodic plate maintenance. In contrast, direct digital radiography uses flat-panel detectors to capture images directly and enables faster image availability, improved workflow efficiency, lower radiation dose, and better image consistency. This makes DR more attractive for high-volume hospitals, trauma centers, orthopedic departments, and advanced diagnostic imaging facilities where throughput, dose optimization, and diagnostic confidence are important procurement priorities. As healthcare providers increasingly move beyond basic digitization toward fully digital and automated radiography workflows, CR becomes less competitive for new installations and higher-end upgrades. Although CR remains relevant in cost-sensitive and transitional facilities, the stronger clinical and operational value proposition of DR is gradually narrowing CR’s addressable market. This shift is expected to limit long-term growth, particularly in digitally mature healthcare systems where hospitals are prioritizing faster imaging workflows, improved dose performance, and more integrated radiography platforms.

Market Opportunities:

Expanding CR Adoption in Low- and Middle-Income Countries with Limited Imaging Access: The expansion of computed radiography in low- and middle-income countries represents a significant growth opportunity, as access to basic diagnostic imaging remains uneven across many healthcare systems. X-ray imaging continues to be one of the most essential first-line diagnostic tools for chest infections, trauma, orthopedic conditions, tuberculosis screening, and emergency care. However, many smaller hospitals, rural diagnostic centers, public-sector facilities, and community-level healthcare providers continue to face limitations related to advanced imaging infrastructure, capital budgets, trained workforce, and digital connectivity. Computed radiography addresses this gap by enabling facilities to digitize existing analog X-ray workflows without immediately replacing the full X-ray room. While direct digital radiography offers stronger long-term workflow efficiency, its higher upfront investment may restrict deployment in resource-constrained settings. As governments and healthcare organizations continue to expand affordable diagnostic access and rural imaging services, computed radiography is expected to remain a practical bridge technology for facilities seeking basic digital imaging capability with controlled capital expenditure.

Analyst’s Thoughts

According to Priyanshi Upadhyay, Research Analyst - BIS Research, “The computed radiography market is expected to witness steady but selective growth, driven by the continued need for affordable digital conversion of existing X-ray infrastructure, particularly across cost-sensitive and underserved healthcare settings. While direct digital radiography is increasingly preferred in high-volume hospitals due to faster image availability, improved workflow efficiency, and stronger dose performance, computed radiography continues to hold relevance as a practical bridge technology for facilities that cannot immediately replace functional analog X-ray systems. Its ability to reduce dependence on film processing, support PACS-compatible image management, and enable phased radiology modernization makes it important for smaller hospitals, diagnostic centers, dental clinics, rural facilities, and public-sector providers. With demand increasingly concentrated in emerging markets and lower-volume healthcare environments, the market’s long-term opportunity will depend on affordability, service support, compact system design, and workflow connectivity rather than major hardware innovation.”

Focus on Application, End User, and Region - Analysis and Forecast, 2026-2036

Computed radiography is a cassette-based digital X-ray imaging technology that uses reusable photostimulable phosphor imaging plates to capture X-ray exposures and convert them into digital images through a CR reader or scanner. It enables healthcare facilities to digitize existing analog X-ray systems without replacing the entire X-ray room, supporting digital image storage, retrieval, sharing, reporting, and PACS-compatible workflows.

To strengthen their market position, companies are focusing on affordable digital conversion solutions, compact CR reader design, durable reusable imaging plates, improved image processing software, and PACS or mini-PACS integration. Many players are also targeting smaller hospitals, diagnostic centers, dental clinics, orthopedic practices, rural facilities, and cost-sensitive healthcare markets where existing X-ray systems remain functional and full direct digital radiography adoption may be financially difficult. Service support, distribution reach, workflow connectivity, and lifecycle management are also becoming important competitive strategies.

The following are the USPs of this report:

• Market regulations and key trends in the computed radiography market

• Market dynamic analysis of the opportunities, trends, and challenges in the market

This report is valuable for computed radiography system manufacturers, imaging plate and cassette providers, diagnostic imaging companies, distributors, hospitals, diagnostic imaging centers, dental clinics, orthopedic facilities, public-sector healthcare providers, and investors involved in radiography infrastructure and digital imaging solutions.

The global computed tomography market is projected to reach $13,197.1 million by 2036 from...

The global dental radiography market was valued at $2,328.5 million in 2021 and is projected...